Eight times a year, the Bank of Canada and the US Federal Reserve have meetings to set and announce their key interest rates. In what I’m sure is a total coincidence, they often happen on the same day. Per the Bank of Canada and the US Fed, here are the dates for 2026:

Wednesday, January 28

Wednesday, March 18

Wednesday, April 29

Wednesday, June 10 / June 17th for the Fed

Wednesday, July 15 / July 28th for the Fed

Wednesday, September 2 / September 15th for the Fed

Wednesday, October 28

Wednesday, December 9

Normally I don’t really pay too much attention to financial headlines. But since interest rates have a direct impact on the monthly income I can expect from the cash holdings in my portfolio (and by “cash” I mean ultra short-term bond funds1), and since I try to keep my HISA and short-term bond table (Canada & US) accurate, I do pay attention to that particular piece of market intel.

ZMMK in CAD, ICSH in USD, both members of the ETF All-Stars club ↩︎

And here you see why most of my “cash” is in ICSH instead of ZMMK. US interest rates are higher in Canada, and although there is of course foreign exchange risk involved, I’m ok with that. ↩︎

Used for monthly salary; held only in non-registered

XEQT: CAD 100% Equity

0%

6.5%

Mostly in TFSA

HXT: CAD Equity

7.4%

6.3%

Used for monthly salary; held only in non-registered

XIC: CAD Equity

5.3%

6.1%

Did not add or subtract from this holding this year

DYN6005: USD HISA

3.7%

0%

Replaced by ICSH

DYN6004: CAD HISA

2.6%

0%

Replaced by ZMMK

HXS: USD Equity

2%

0%

Sold off from non-registered accounts to fund monthly expenses

VCN: CAD Equity

1.8%

1.1%

In TFSA; reduced in favour of XEQT

What didn’t change much

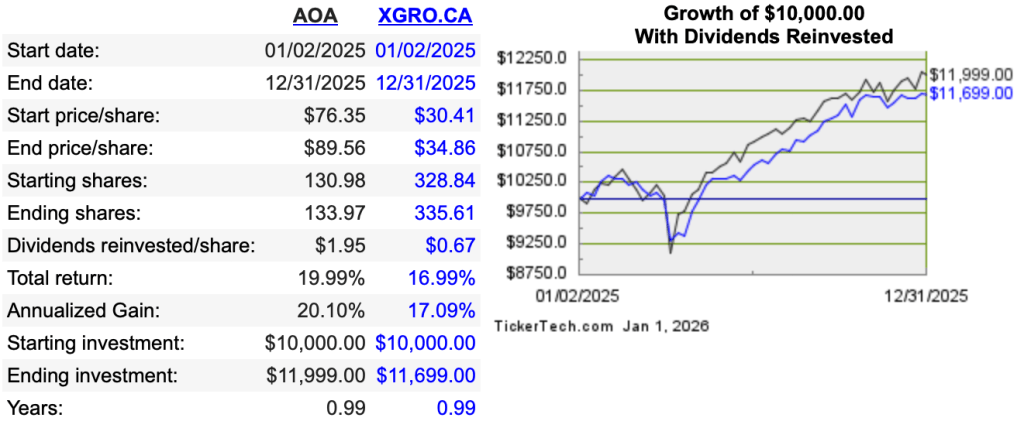

The portfolio is still dominated by XGRO and AOA (not coincidentally, these are two of my ETF All-Stars) and they both had excellent years, as shown by this tool:

What also didn’t change is my overall approach: decisions for shifting funds is totally dependent on maintaining my asset allocations that haven’t changed either:

5% in cash or “cash like” holdings

15% in bonds

20% in Canadian Equity

36% in US Equity

24% in International Equity

This approach meant that what I sold off in my non-registered portfolio to fund my day to day expenses changed throughout the year; as the year progressed I sold HXDM, then HXS (reducing this to zero), and then finally HXT, all in the service of keeping my assets in line with my targets.

What did change

As a result of changing brokers (QTrade to Questrade), I lost the ability to cheaply hold HISAs. And so I had to change tactics and hold “HISA-like” ETFs instead. (which, on Questrade, like all ETFs, can be bought and sold at no charge). At the same time, I realized that I could increase my returns by shifting more to the US market. Significantly higher interest rates in the US means that I can get more for my “safe” funds, with the small annoyance that I have to deal with USD. You can see the latest rates on my frequently updated page.

As I sold off “pure” equity funds from my non-registered accounts, I had to make changes to keep my bond percentages aligned with my targets3. This is the reason XEQT (a global 100% equity fund) now makes an appearance in the overall picture. The nice side-effect of adding XEQT is that my portfolio is now 76% held in all-in-one funds, up about 4% from the beginning of the year. All-in-ones do the rebalancing for you, which is a good way to avoid bad behaviours.

Behind the scenes I also tried to better focus each of the account types to make things simpler and clearer:

TFSAs are now 90% equity, with the rest held in bonds. The rationale here is that TFSAs will be the last things I touch to fund retirement, and hence have the longest time horizon. There are still too many individual ETFs here, and my January resolution is to simplify this further.

RRIFs now have only three funds: AOA, XGRO and ICSH.

Investment accounts will remain a bit chaotic as most of my retirement expenses are coming out of these. It also happens to be the place where my “free money” payments end up and so there is a small amount of inbound cash to purchase things with. The 2026 plan is to continue to draw down my non-registered funds since my spouse is still working and would be taxed higher on her capital gains.

What’s ahead in 2026: RRIF

My own calculations4 show that my household RRIF-minimum income will be up 19% YoY, a result of good returns in the RRIF (roughly 11% YoY by my calculation) and being a year older. Selling XGRO every month will cover the required payments, and quarterly I will shift a portion of AOA into XGRO, converting the USD to CAD using Norbert’s Gambit.

What’s ahead in 2026: TFSA

January will see an effort to reduce the number of ETFs here. There are multiple CAD equity ETFs which I should consolidate into one, for instance.

We continue to contribute monthly to the TFSAs. The goal is to maximize equity percentage while minimizing the number of funds held. Once the cleanup is done, I expect to purchase XEQT monthly. Questrade introduced automated investing which I’ll likely set up to accomplish this.

What’s ahead in 2026: Non-Registered Accounts

The same strategy as 2025 will continue. Shortfalls in my monthly salary will be covered by selling assets in the non-registered accounts. I ended last year up 2% YoY in my non-registered accounts; I don’t really expect a repeat there. All things being equal, I should be down in my non-registered accounts at this time next year.

Indirectly. I haven’t tried to do a USD withdrawal for a RRIF payment, but in theory it should be possible. Instead I convert my AOA into XGRO a little at a time using Norbert’s Gambit. ↩︎

My VPW cash cushion is about 50% of my cash position in the retirement portfolio. The other 50% of my cash position is inside the RRIF in order to avoid taxation on those monthly distributions. ↩︎

AOA and XGRO are both 20% bonds, not 15%, and so mathematically this has to be offset with 100% equity somewhere in the portfolio. ↩︎

My providers will give me the real numbers sometime in the coming weeks. How much hassle this will be is TBD. ↩︎

The Bank of Canada and the US Federal Reserve both had their last rate setting meeting of 2025 today. These meetings are of interest to the DIY investor because they set the bar for the interest rate paid on short term loans / high interest savings accounts. I track a universe of HISAs and ETFs of interest over at https://moneyengineer.ca/hisa-and-short-term-bond-table-canada-us/.

The Bank of Canada announcement is here, and the US Fed announcement is here. The Bank of Canada kept things the same, with a rate of 2.25% while the US cut their rates by a quarter point, so they’re now sitting in a range of 3.5-3.75%. Anyway, the gap between the US and Canadian rates is narrowing, but the US overnight rates are still 1.5% higher (aka 150 basis points) and so it pays to use USD money market funds and HISAs if you’re able.

The next opportunity for the banks to mess with interest rates is January 28, 2026.

I’ve been making monthly posts about the current interest rates available via “Series F” High Interest Savings Accounts (HISAs) and HISA-like ETFs for a while now. These are an excellent place to park your money. My current broker, Questrade, gives me access to HISAs, but they are not free to trade, hence of zero interest1 to me — I use HISA-like ETFs instead, some options I uncovered earlier this year are discussed over here.

Anyway, I’ve decided to make things a bit easier and make the HISA table a permanent fixture at the Money Engineer. You can always find the most recent version of the table over here: https://moneyengineer.ca/hisa-and-short-term-bond-table-canada-us/, so feel free to bookmark it. (It’s a submenu of the DIY Investors menu found under All Readers.) I’ll generally make updates to it any time the interest rates change in Canada or the US, which they did last week.

If ever I’ve missed an update, or you see a problem, always happy to hear from you — just shoot me a note.

Insert joke about falling interest rates / typical big bank interest here. ↩︎

As was widely expected, the Bank of Canada and the US Federal Reserve both announced quarter point cuts to their base interest rates. This will be reflected shortly across high-interest products out there, and I’ll update the HISA and HISA-like ETF Table for October 2025 in the coming days.

The next meeting where rates could change happens December 10th.