You can see last month’s table overhere, with a newly updated “last update” date 🙂

Since my provider (Questrade) doesn’t provide a way to buy HISAs on the cheap, I use ZMMK for my Canadian cash holdings and ICSH for my USDs. These ETFs are part of my ETF all-stars. ZMMK’s last distribution was $0.12 per share, which works out to a yield of 2.89%2 and ICSH’s last distribution was $0.198284 per share, which works out to a yield of 4.71%.

As expected, I’m getting a slight premium on my interest rate for taking on a slightly more risky investment. I’ll keep on eye on that in future posts!

Summary: BMO has reduced fees on its family of asset-allocation ETFs (ZCON, ZBAL, ZGRO, ZEQT) to put its Management Expense Ratio (MER) in the same realm as competing families from GlobalX, iShares and TD.

Low-cost all-in-one ETF providers, and the symbols you can use to buy them

In my view, any of these families are worthy of your investment dollars. Which particular fund you pick within a family depends on your tolerance for volatility and/or your timeline for needing the money you’re investing. Each list of fund symbols in the table above is listed in order of amount of equity — so for TD, you can see that TEQT has the most equity (100%) whereas TCON has the least (40%). You might want to give https://moneyengineer.ca/2025/05/06/investment-basics-asset-allocation/ a read to get more familiar with the concepts.

There are other all-in-one families (Vanguard, Fidelity, Mackenzie), the ones shown here are the least expensive of the lot at 0.20% MER or less. TD is the current winner of the lot with a rock-bottom 0.17% MER. ↩︎

There’s also an ESG asset allocation fund, ZESG. ↩︎

There’s also a bunch of covered call variations that are of no interest to me. ↩︎

iShares is the family I work within. I started with them over the others because they could be traded for free on my former provider (QTrade). My current provider (Questrade) allows free trading for any ETF. ↩︎

As of this morning, this is what the overall portfolio looks like:

Retirement holdings by ETF, May 2025

The portfolio is dominated by my ETF all-stars; anything not on that page is held in a non-registered account and won’t be fiddled with unless it’s part of my monthly decumulation. Otherwise I’ll rack up capital gains for no real benefit.

The biggest changes were caused by two events that happened over the past 30 days:

I did a small rebalancing exercise to reduce my exposure to the Canadian equity market, selling VCN in favor of XEQT. (XEQT is only 23% Canadian equity per dollar invested; VCN was 100%). This sort of rebalancing happens whenever I drift more than 1% off of my target allocations.

I took some cash from a HISA and invested it in ZMMK; for reasons too boring to report here, that money was effectively not being tracked in these pages until this month — that anomaly won’t be repeated in subsequent months since ZMMK and ICSH are where I park the “cash” position of my portfolio.

Plan for the next month

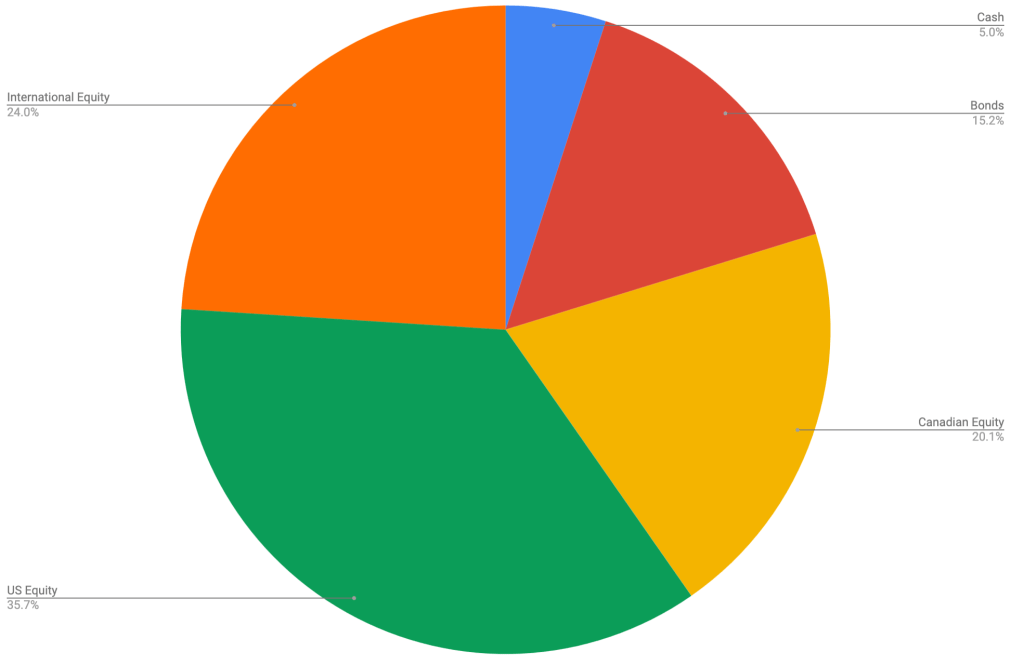

The asset-class split looks like this

This looks to be pretty close to my target percentages which haven’t changed:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds (almost all are buried in XGRO and AOA)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX 60)

36% US equity (dominated by ETFs that mirror the S&P 500, with a small sprinkling of Russell 2000)

24% International equity (mostly, but not exclusively, developed markets)

So, the plan for next month is, do nothing out of the ordinary. Reinvest cash (dividends, TFSA contributions) in one of AOA, XEQT/XGRO, ICSH or ZMMK depending on the asset category most in need on the day of the reinvestment. All these ETFs are covered on my ETF All-Stars page.

One thing I may do is to try to make shifts2 to get a little more return out of my cash position. US interest rates are quite a bit higher than Canadian rates, and so if my cash position is held in USD, I stand to eke a few more points of return there. TBD.

Overall

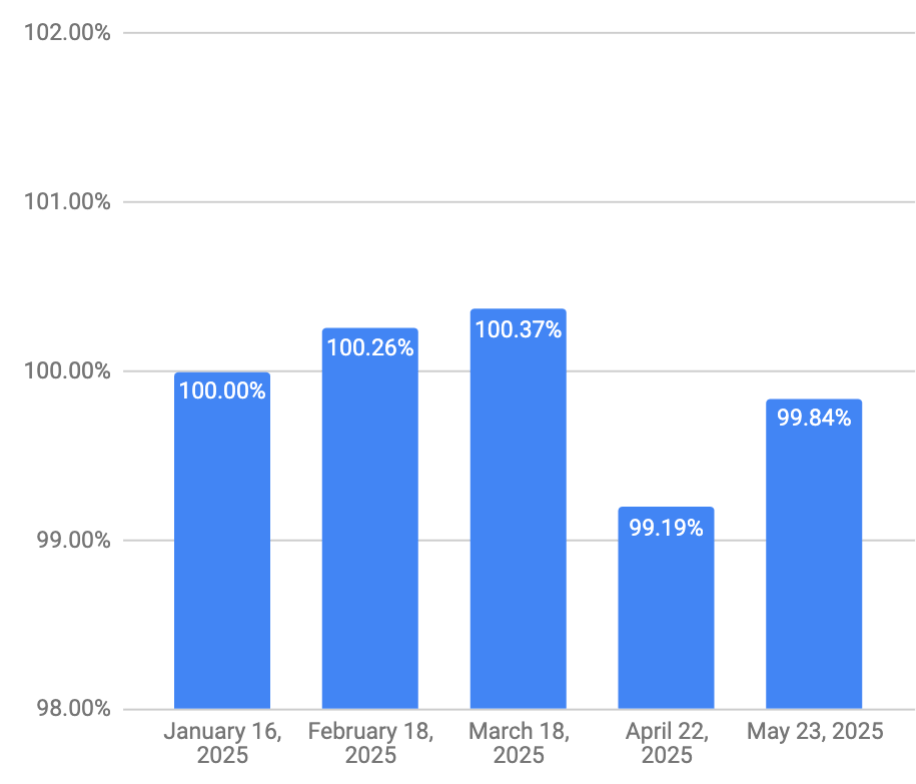

My retirement savings had a nice bounce-back this month, looks like I can cancel the mega-pack of pot noodles I had on order.

Monthly retirement savings, as percentage of Jan 2025 value

The salary I collect month to month recovered a bit, too, although not as quickly. That’s the magic of using VPW’s cash cushion — neither boom nor bust months translate into large changes in the take-home pay.

Monthly salary, as percentage of Jan 2025 salary

That’s up one from the previous month. In order to collect on Questrade’s transfer bonus, (which they have yet to pay me, they are apparently in a world of hurt on the IT front) you have to have a non-registered account to get paid into. The other 3 are “normal” — one non-registered account for me, one for my spouse, and jointly held one that serves as a cash cushion to smooth out month to month variations in my retirement salary. Read more about that over at https://moneyengineer.ca/2025/01/31/im-retired-now-how-do-i-get-paid/↩︎

With Questrade, all ETF trades are free to make, so I don’t have any real reason not to make such changes. ↩︎

***updated this post to reflect the fact that XEQT has dropped XUS from its portfolio as of July 2, 2025***

This post is inspired by my original on the topic, “What’s the deal with XGRO“? XGRO is great, but since my target asset allocation is only 15% bonds, and XGRO’s bond target is 20%, there’s some tweaking I have to do in order to reduce the bond exposure. That tweak is increasingly being provided by XEQT, part of the same iShares family that produced XGRO.

(As mentioned elsewhere, I rely heavily on all-in-one ETFs in my retirement portolio. New to all-in-ones? Read a bit about them here.)

XEQT, like XGRO, is actually investing in thousands1 of different stocks. Unlike XGRO, it does not hold any bonds at all. I thought it would be interesting to see what, exactly, is underneath every $100 you invest in XEQT. See the results below:

The top stock holding outside North America belongs to Taiwan Semiconductor, at 46 cents for every $100 invested. Additionally, the geographic exposure looks like this:

Geographic exposure of XEQT as of July 25, 2025

One other little tidbit that might be interesting: the distribution yield of XEQT is 2.94% compared with 2.91% for XGRO. This I find a bit surprising, since I would have expected XGRO’s yield to be quite a bit better.

And, if you’re really paying attention, you’ll see that the dollar amounts of this column add up to roughly $80, in keeping with the 80/20 philosophy of XGRO. ↩︎

i lump these together because they hold exactly the same thing. Some loophole that iShares needs to exploit, I gather. ↩︎

On the date I pulled these numbers, cash cracked the top 10 for a holding of $1.34, which is not usual, so I just dropped it. Not sure why that is…perhaps by the end of the month it will resolve itself. ↩︎

Previously, we talked in broad terms about the categories of what you can invest in, namely Equities, Bonds, and Cash. Having % allocation targets for each of these classes is a necessary starting point for making decisions. Here’s a post that talks about how to get there.

Maybe it’s helpful to take a look at some examples of what you can buy to hit each of these categories. I’m going to use iShares as the guinea pig since it offers a lot of products, but you could play the same game with any provider you like.

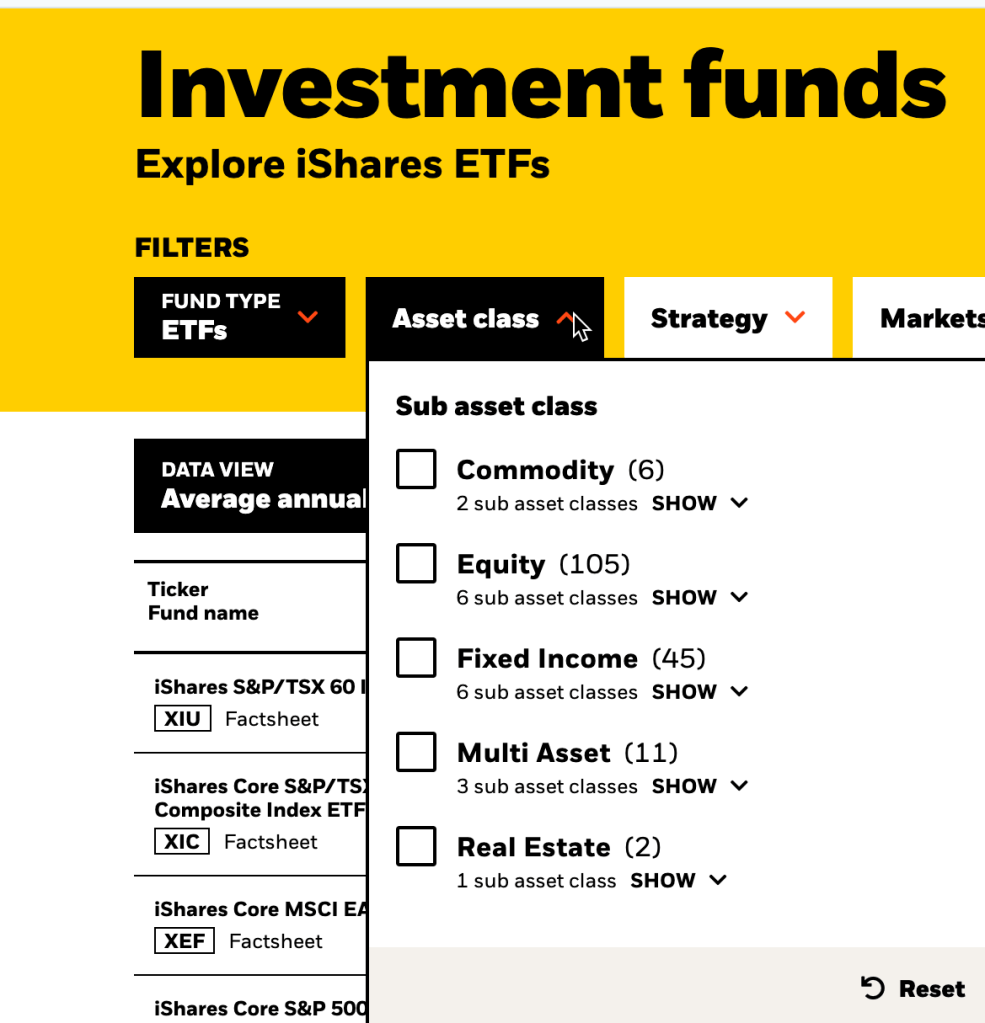

So if you visit iShares ETF page (this is what I’m looking at as I write this), you are presented with a list of (and I’m not joking here), 169 different ETFs. Ouch. How can anyone decide which of these is the best fit?

Helpfully, the page includes an “Asset Class” Filter:

iShares “Asset Class” classifcation for their 169 ETF products (May 2025)

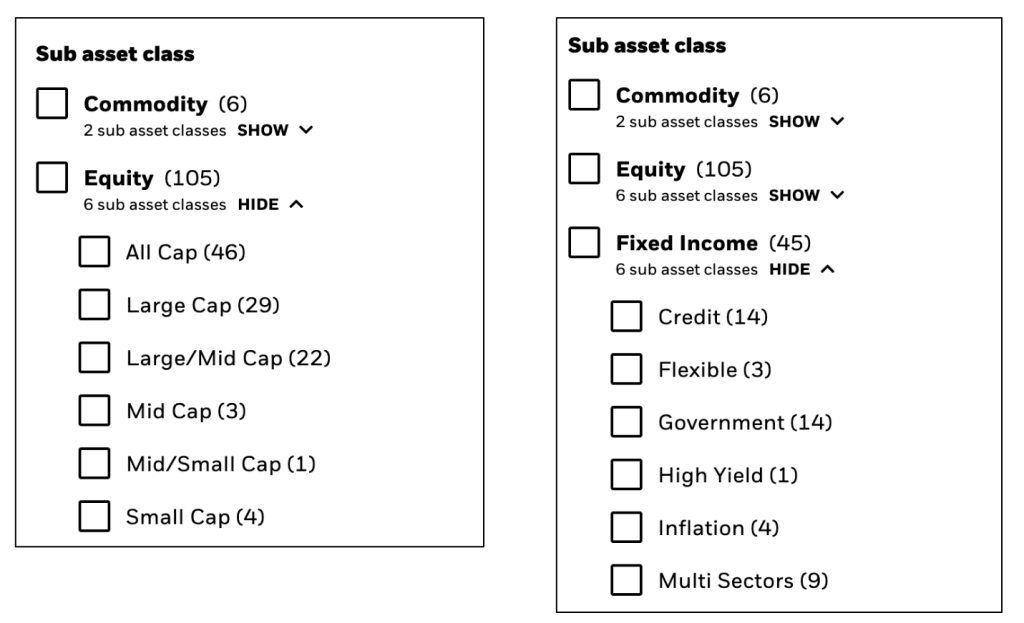

…and now you can quickly recognize “Equity” (with 105 different ETFs to choose from). “Fixed Income” is the other term of interest — this will include bonds and probably something that looks more like cash. So this is now looking a little more sane. Wait, what’s this? They each have “sub classes”?

iShares ETFs Equity and Fixed Income Sub Classes as of May 2025

This narrows things down somewhat. Let’s break these down further.

Equity Sub-Classes

The term “Cap”1 comes up here. This is short for “capitalization” or, in plain English, “How big is the company we’re investing in?”. I don’t like to place bets on which companies are the most appropriate, so I would gravitate to the “All Cap” sub asset class here. “Large Cap” is probably the next best bet, since large companies tend to dominate the returns in the markets they serve. So let’s select both2.

We’re still left with 75 ETFs with that filter. Still a lot to take in. I suggest sorting by “Net Assets” with the largest on top by clicking in the appropriate column. I figure if other people are investing in these funds, why shouldn’t I?

So here’s my take on the ETFs I see on my screen:

ETF Symbol

Class

Consider?

Comments

XIU, XIC

CAD Equity

Y

Both variations of TSX. I would lean towards XIC because it is cheaper to own.

XSP, XUS, XUU

US Equity

Y

XSP is “hedged” meaning it tries to take away the FX variations, and I normally don’t worry about that. XUU would be my top pick here.

XEF, XFH, XSEM, XEC

Int’l Equity

Y

XSEM/XEC are solely emerging markets, and I would never just hold it absent something like XEF/XFH as well. If I had to pick one, it would be XEF since it’s unhedged. If I could add a second, it would be XEC because it’s cheaper to own.

XQQ

US Equity

N

This is too narrowly focused on 100 Nasdaq stocks; the point of buying a asset category is to buy as many companies as possible

XAW

US Equity + Int’l Equity

Y

An easy way to get non-Canadian Equity exposure with one ETF

XGD, XEI, XDV, XFN, XEG, CPD, CDZ, CIF, XIT, XHC

CAD Equity

N

These are all too narrowly focused and/or trying to make bets on specific parts of the market. Asset allocation is about buying the whole market.

Everything else

No idea

N

There are probably funds that I would consider further down the list but there’s only so many hours in the day, ya know?

Assessing the largest iShares All-Cap/Large Cap ETFs

Fixed Income Sub-Classes

One thing I’ve learned is that Fixed Income is harder to parse than Equity. My quick impression of the names I see on my screen:

Credit: No idea what this might mean

Flexible: ibid

Government: ok, that’s easy, this is only looking at bonds issued by governments. This tends to be the most popular segment of the bond market because (a) there’s a lot of them3 and (b) they are seen as safe investments.

High Yield: This is code for “junk bonds”. More risky, but higher rates of interest.

Inflation: My guess is that this is what is intended to mean “cash”

Multi-Sectors: My guess is that this trying to build a broad universe of bonds.

So, for simplicity, I think I’ll ignore the sub-segments but give you my take on the largest offering here again.

ETF Symbol

Sub Asset Class

Consider?

Comments

XBB

Multi-Sector

Y

“Core Canadian Universe” sounds like it’s got a lot of holdings across the spectrum, and it’s cheap to own. Perfect. This is clearly “Bonds” in my nomenclature.

XSB

Multi-Sector

Y

“Short Term Bond Index” makes me wonder if this is leaning towards a cash-like investment. The fact sheet puts the loan duration at “1 to 5 years” which isn’t cash-like enough for me. This is “Bonds”, albeit rather conservative ones.

XCB, XSH

Credit

Y

This is just the corporate bond market with no government. XSH is less risky because its bonds have a shorter duration on average.

CMR

Multi-Sector

Y

“Premium Money Market” sounds like “Cash” to me, and reading the fact sheet4 makes it sound a lot like ZMMK which was my previous winner in this category.

XGB

Gov’t

N

Nothing wrong with it, but I don’t buy “just” government bond ETFs. Without some corporate exposure, they don’t generate enough returns for my liking. I’ll take the risk.

XLB

Multi-Sector

N

This only buys long-duration bonds. This would be ok if you had holdings elsewhere on the shorter side.

Everything else

No idea

N

There are probably funds that I would consider further down the list but there’s only so many hours in the day, ya know?

Assessing the largest iShares Fixed Income ETFs

I do have to break away from the largest list to mention some ETFs on the Fixed Income chart that I didn’t know you could buy on the Canadian Market: XSTH and XSTP, which track the TIPS Bond Index. The TIPS index is well known to US investors5 because it’s a very cheap way to buy an inflationary hedge — it’s in the name, as TIPS stands for “Treasury Inflation-Protected Securities”. Now, of course, this refers to US Inflation, and unless you’re buying XSTH (which is the same as XSTP, except hedged to avoid FX changes) you’re also buying into a security that will vary with the CAD/USD exchange rate. So, not sure it’s of interest to the average Canadian investor, but it’s something I didn’t know about before.

Other classes in the iShares List

We only looked deeply at the Equity and Fixed Income categories, but what about the others?

The Commodity category holds ETFs that trade in one of Gold, Silver or Bitcoin. None of these provide predictable returns and are very narrow bets, so for that reason, I have no interest.

The Multi-Asset category contains funds that are a mix of Equity and Fixed Income, with the exact ratios depending on which specific fund you buy. This category contains funds I invest heavily in, namely XGRO and XEQT. I cover “all-in-one” funds like this in this article. Multi-asset funds basically take all the work of trying to balance your Equity and Bond percentages out of your hands for a very low price.

The Real Estate Category is just another segment of the Equity category and like other sub-segments, I don’t pay any attention to this one either.

A Final Word

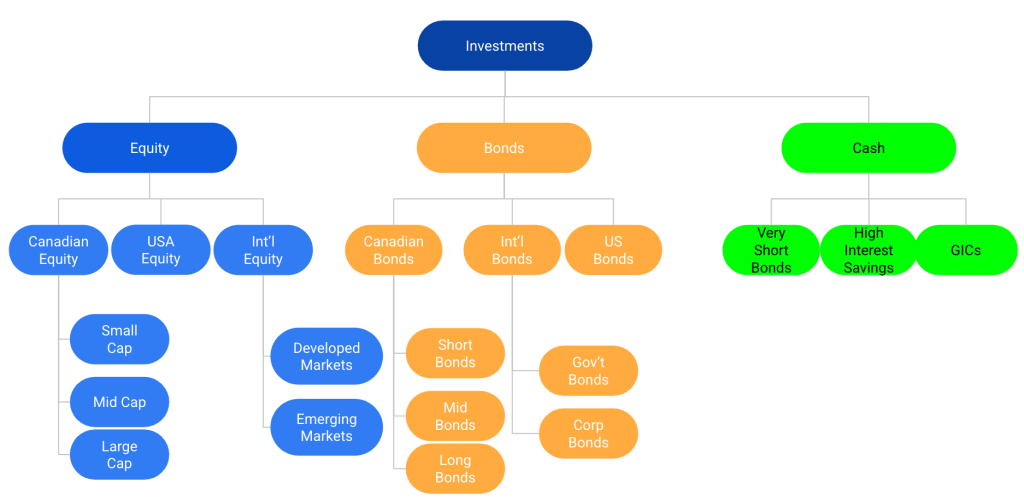

Dividing Investments into asset classes (a short example)

It’s easy to slice and dice the three broad asset categories (Equity, Bonds, Cash) many different ways and you can spend many pleasurable6 hours finding the absolute “best” ETF for any subsegment listed above, or you could invent your own (Ultra Short Term Emerging Market High Yield Bonds Canadian Hedged?). It’s easy to go overboard here, and in the course of simplifying my portfolio, I have restricted myself to 5 broad categories when i think about my investments:

Equity: divided into 3 buckets for Canadian, US and International Equity

Bonds: There are no sub-buckets here, but the products I buy have broad geographic, segment, and duration coverage. Are they allocated optimally? No idea.

Cash: Everything in this category is held in either USD or CAD ultra-short term bonds.

You can see the specific holdings in my portfolio by looking at any of the “What’s in my Portfolio” posts (April 2025 is here or a series of 3 videos is found here) or you can just see the 4 ETFs I hold for the long term here.

And in the course of writing this article, I discovered this fun Asset Mixer you can use to experiment with different asset allocations yourself. It’s like making cocktails, except with money 🙂

Full disclosure: I cheated here. I couldn’t figure out why I wasn’t seeing TSX funds under “all Cap” but that’s because the usual TSX 60 fund is listed as a large cap fund. ↩︎