I’ve been making monthly posts about the current interest rates available via “Series F” High Interest Savings Accounts (HISAs) and HISA-like ETFs for a while now. These are an excellent place to park your money. My current broker, Questrade, gives me access to HISAs, but they are not free to trade, hence of zero interest1 to me — I use HISA-like ETFs instead, some options I uncovered earlier this year are discussed over here.

Anyway, I’ve decided to make things a bit easier and make the HISA table a permanent fixture at the Money Engineer. You can always find the most recent version of the table over here: https://moneyengineer.ca/hisa-and-short-term-bond-table-canada-us/, so feel free to bookmark it. (It’s a submenu of the DIY Investors menu found under All Readers.) I’ll generally make updates to it any time the interest rates change in Canada or the US, which they did last week.

If ever I’ve missed an update, or you see a problem, always happy to hear from you — just shoot me a note.

Insert joke about falling interest rates / typical big bank interest here. ↩︎

You can read about my asset-allocation approach to investing over here.

The view post-payday

I pay myself monthly in retirement, so that’s a good trigger to update this post. On October 27th, this is what it looks like:

The portfolio is dominated by my ETF all-stars; anything not on that page is held in a non-registered account and won’t be fiddled with unless it’s part of my monthly decumulation. Otherwise I’ll rack up capital gains for no real benefit.

No massive changes this month; the one you might notice is a slight shift from AOA to XGRO. I move some of my USD holdings into CAD every quarter, and last month was when I did it. The majority of my spending is in CAD, so I use Norbert’s Gambit to move funds around.

Plan for the next month

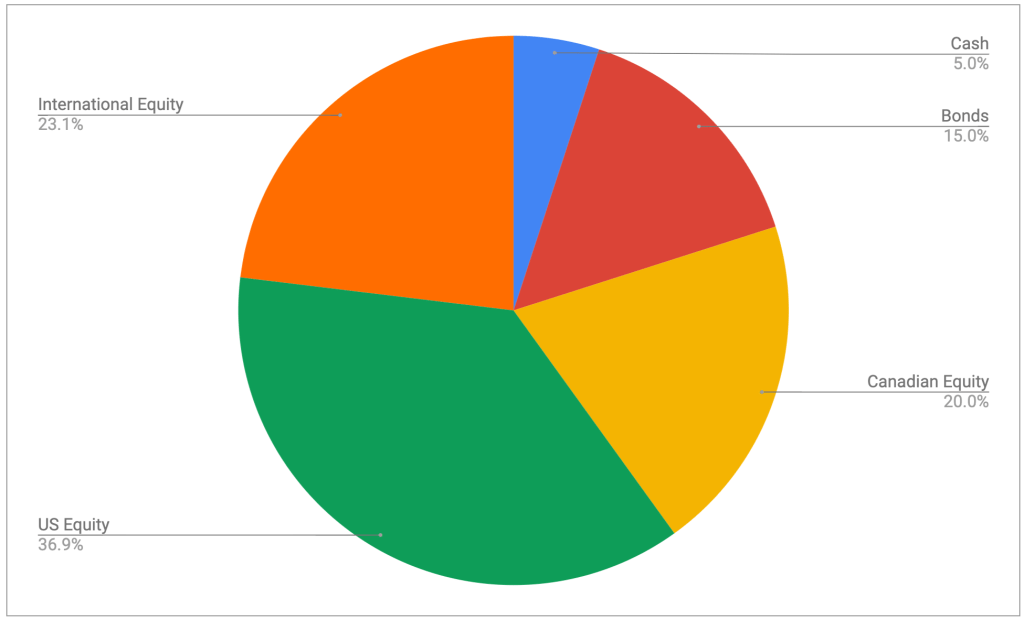

The asset-class split looks like this

It’s looking pretty close to the targets I have, which are unchanged:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds (almost all are buried in XGRO and AOA)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX 60)

36% US equity (dominated by ETFs that mirror the S&P 500, with a small sprinkling of Russell 2000)

24% International equity (mostly, but not exclusively, developed markets)

All looks to be in order from an asset allocation perspective, no need to do anything here.

Overall

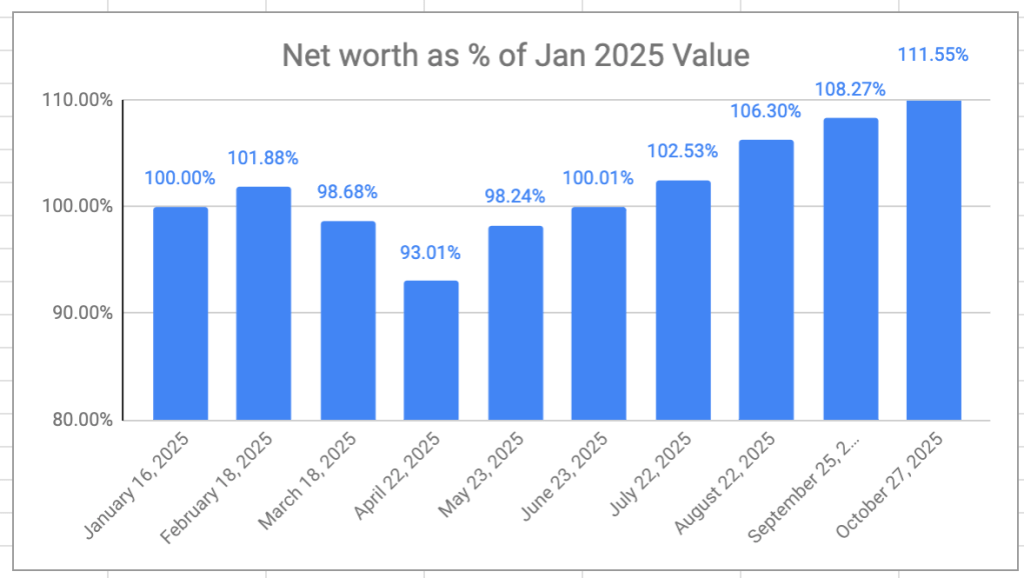

The retirement savings had a great month, again — a 6-month growth streak at this point. Overall, I’m now 11.5% ahead of where I started even though I’ve been drawing a monthly salary since the beginning of the year. I don’t really expect the winning streak to continue, but VPW allows me to take some benefit from the frothy stock markets at moment.

Net Worth as a percentage of starting point

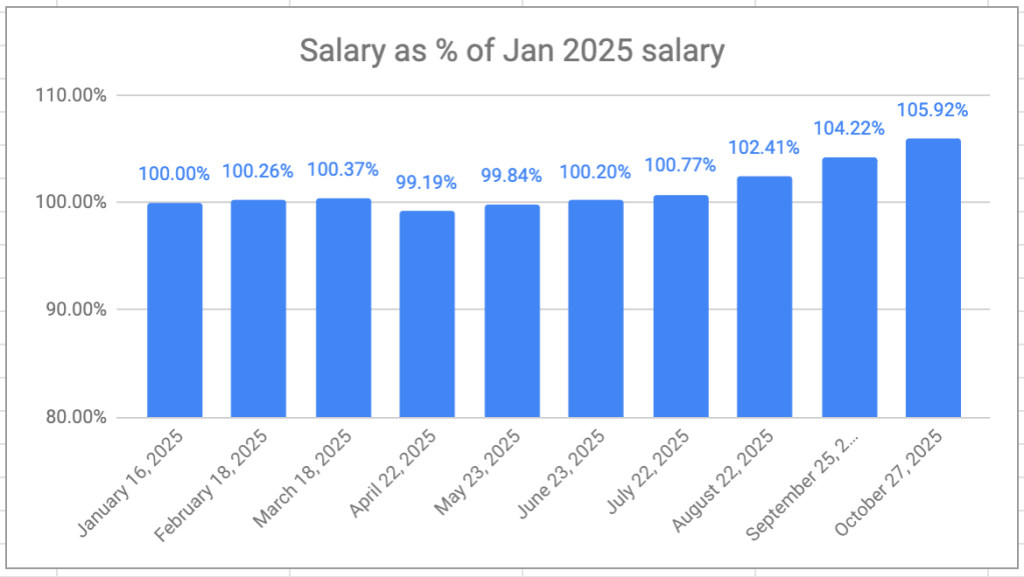

My VPW-calculated salary has hit a new high this year, 5.92% higher than my first draw in January. The monthly salary is also on a 6-month growth streak.

Monthly Salary as a Percentage of Jan 2025 salary

The months ahead will see the final “goodbye” to QTrade1 as the last of my RRIF investments will move to (mostly) Questrade2.

I didn’t have a great deal of issue with QTrade as a provider, but their support (lack thereof) was beginning to become irritating. ↩︎

My own QTrade RRIF will join the RRIF holdings I already have with Wealthsimple. They remain a potential backup provider of my retirement savings. I would have moved more to take advantage of their cashback promotion, but they still, inexplicably, do not support self-directed spousal RRIF accounts. ↩︎

(New to asset allocation ETFs aka all-in-ones? Here’s a good place to start.)

Asset allocation ETFs can be purchased from any number of companies. In this article, we look at 4 of the biggest names:

TD, with TEQT, TGRO, TBAL et al

Blackrock/iShares with XEQT, XGRO, XBAL et al

BMO with ZEQT, ZGRO, ZBAL et al

Vanguard with VEQT, VGRO, VBAL et al

The blueprint for each of these ETFs are similar: pick Canadian, US, International and (where applicable1) bond indices, pick a target percentage allocation for each slice of the pie, and carry on…

I previously talked about the variations in percentage allocation (the size of the pie slices) between the major funds over here.

But what about the indices that each of the major fund families track? What’s in the pie? Are there significant differences? Here’s a summary of what I found:

Bloomberg Global Aggregate Canadian Float Adjusted Bond

So there is variation in the pie recipes (the underlying indices), but is it really of any significance? At a glance, I wonder how different the offerings from iShares and BMO actually are — the same index providers show up in each. Without looking at what stocks are actually found in each of these, here’s a quick take, simply based on the names of the indices:

Canadian Equity: All of these funds hold the broad Canadian market, over three different index providers23. iShares and BMO use a capped index, which, in theory, should limit exposure to the very largest Canadian businesses somewhat.

US Equity: Three different index providers seen here (Solactive, S&P and CRSP). TD only holds large US companies, the others hold smaller and midsized US companies. In the last ten years, this has been a winning strategy, but it’s not always been that way.

International Equity: Three different index providers: Solactive, MSCI, FTSE. TD excludes emerging markets (e.g. Brazil, Russia, Taiwan, China, India). The others don’t.

Bonds: Hard to tell just based on the names, but three of them use the same FTSE index. Vanguard uses a Bloomberg index. So I’ll say that it’s likely that Vanguard’s bond portfolio will look different from the other three.

In a future post, I’ll delve into what the main holdings of each of these funds are in each of these categories to see what differences emerge. And whether these differences actually matter!

This excludes 100% equity funds like XEQT, naturally ↩︎

The “composite” in “Capped Composite” means “all the stocks of the TSX”. ↩︎

HISAs are “High Interest Savings Accounts” and offer a nearly zero risk, highly liquid way to earn some interest on your cash holdings. If your broker doesn’t give you access to HISAs (or you have to pay large transaction fees to acquire them), then there’s also ETFs that fit the bill, and some of them are now in this table, too.

Since there’s no central bank meetings until the very end of this month, most of the September 2025 version of this table applies. The exception are the ETFs, which publish new yields monthly, so those figures are updated in the table below:

Canadian HISA and HISA-like ETF rates, last updated October 3 2025

ZMMK is a very short-term bond fund that carries more risk than a HISA, but gives a slightly better return as a result. ZMMK appears in my ETF All-Stars list.

Since I hold a substantial amount of USD-denominated ETFs, I also track US interest rates.

USA HISA and HISA-like ETF rates, last updated October 3, 2025

UCSH and HISU invest in HISAs exclusively; I instead use ICSH which is a rough equivalent of ZMMK in terms of portfolio makeup. Like ZMMK, I enjoy a slight premium in yield as a reward for taking a bit more risk.

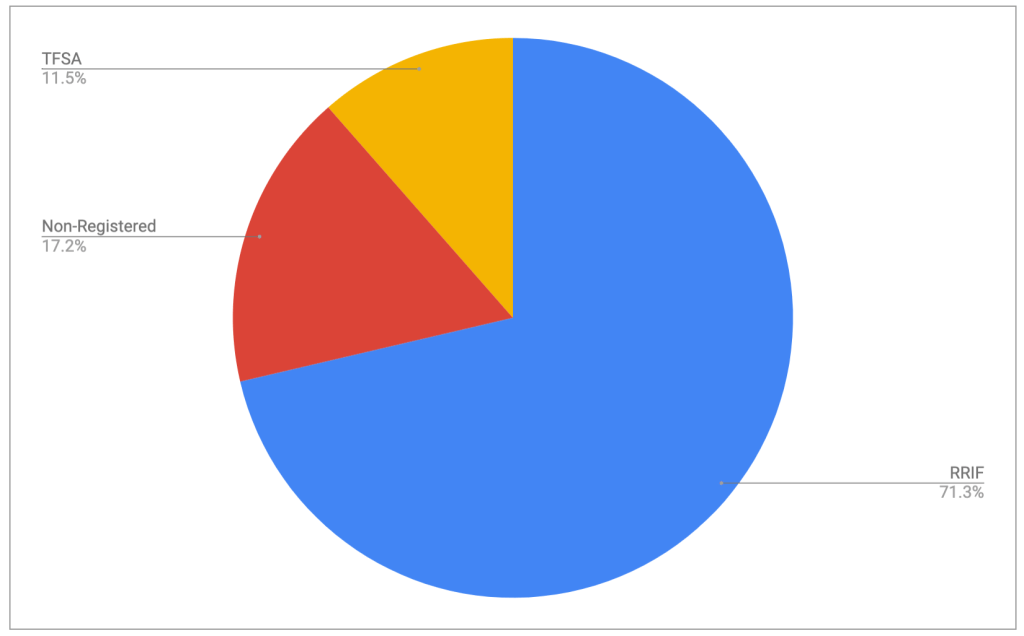

Every month, I try to share with you what’s in my overall retirement portfolio (September 2025 post is here). That retirement portfolio is actually distributed over a bunch of accounts held by me and my spouse and includes RRIFs, TFSAs and non-registered accounts. This is what it looks like at the moment:

Retirement savings as of October 1, 2025 by account type

(My multi-asset tracker is a handy tool to help you quickly create charts that look like the above one).

My current strategy for these three account types looks like this:

RRIF: This is 100% invested in my ETF all-stars. I’m currently withdrawing RRIF minimum payments for two main reasons:

To avoid problems with attribution. I cover that topic over here.

To avoid withholding tax. RRIF minimum payments don’t attract withholding tax, but I am setting aside some of my payments to deal with the unavoidable tax bill come April 2026. I talked about that topic over here.

TFSA: This is mostly invested in the ETF all-stars, but there’s a few stragglers in here1 that I really ought to get rid of. Nothing wrong with the funds in there, but it’s a needless complexity. The TFSA continues to get new funds since it’s hard to beat tax-free growth, and I only buy all-stars with those funds. It will get drawn down last in my retirement planning.

Non-registered accounts: Here it’s a bit of a dog’s breakfast, with very little invested in the all-stars, mostly because most of the equity found here was bought long ago, and changing what I hold would attract capital gains that I would prefer to take on my own terms. It’s where the majority of my early-retirement decumulation takes place.

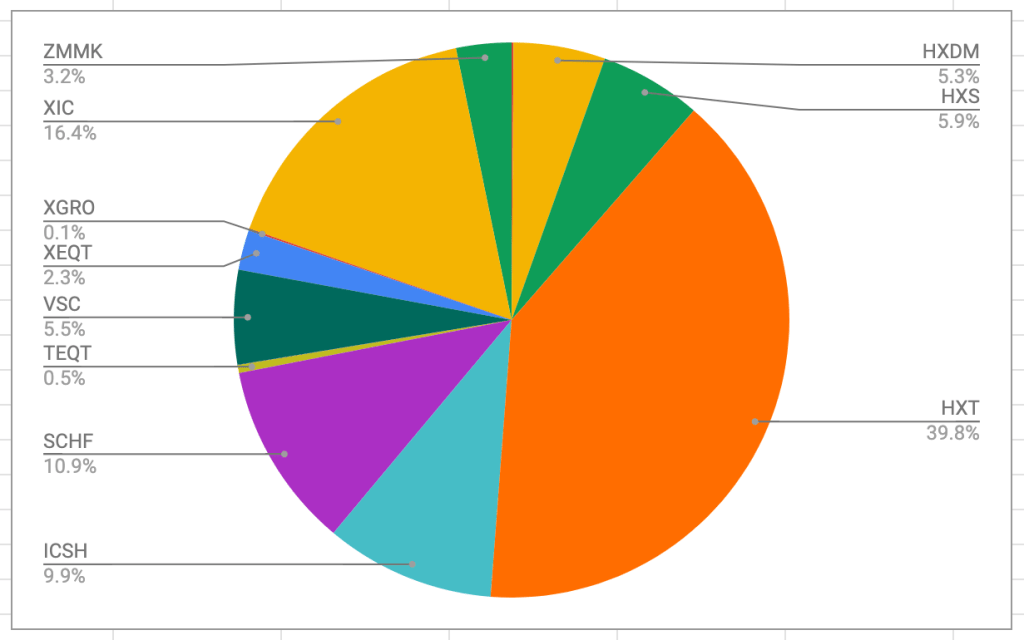

Here’s what that breakfast looks like:

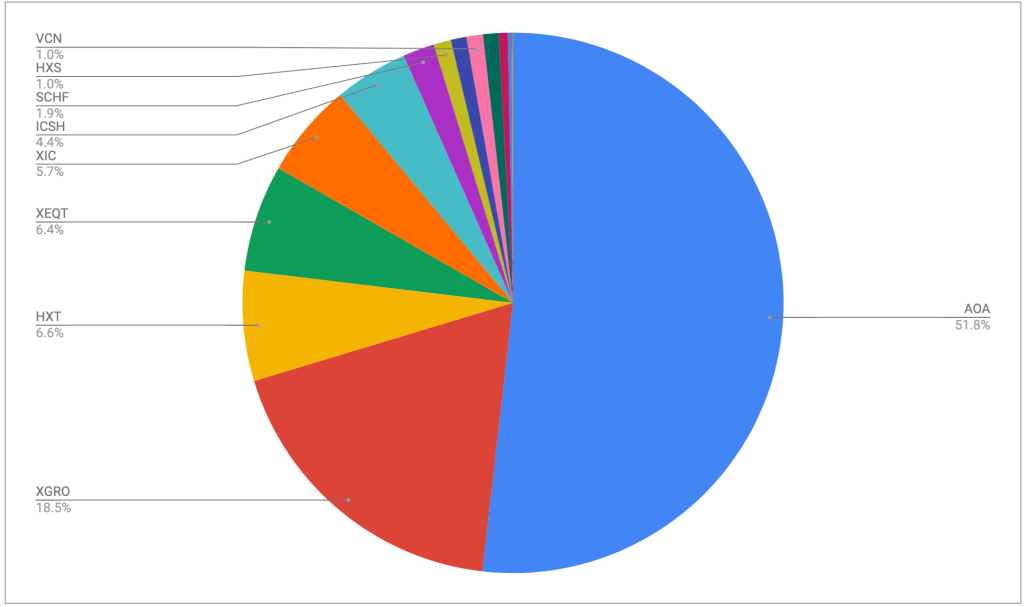

What’s in my non-registered portfolio, October 2025

Here’s a look at each holding, from highest to lowest percentage.

HXT: This is a Canadian equity ETF that does not pay dividends, instead using some wizardry to bury it all in the per-unit price of the ETF. This simplifies taxes, and I have held this fund for a long time. Due to increasing costs of this ETF, it’s among the first to get liquidated as I need funds.

XIC: Canadian equity fund, very popular. I think I bought it to create a bit of dividend income. It will get liquidated after the Horizons funds go (HXS, HXT, HXDM).

SCHF: A very low-cost international equity2 fund in USD that I’ve held for a very long time. It’s funds like SCHF that attracted me to investing in USD, which, at present, adds a lot of complexity.

ICSH: This is one of the all-stars. It is what my VPW cash cushion is invested in3. I use ICSH more than ZMMK in the cash cushion because US interest rates are quite a bit higher than Canadian rates at the moment. I talked about that here.

HXS: Same idea as HXT, except it invests in the S&P 500. This one is held only by my spouse who is still working for a living, so this will just stick around a while, until she stops working and can take on the capital gains.

VSC: A bond fund held by my spouse. I may sell this to harvest some capital gains losses.

HXDM: Same idea as HXT, except international equity. It is on the list to liquidate.

ZMMK: An all-star, held in the same account as ICSH.

The rest (XEQT, TEQT, XGRO) are all new arrivals in the portfolio, purchased using dividends4 from the other funds as well as the bonus payments I keep collecting from Questrade for switching to them.

My non-registered accounts are only a small portion of my retirement holdings, but there’s a fair bit of complexity there. Over time, these accounts will go to zero other than the cash cushion portion (ZMMK, ICSH or whatever replacements I discover) which will remain as long as VPW is my decumulation strategy.

Mostly pure Canadian equity funds. This is to offset AOA that has next-to-no Canadian equity component. ↩︎

VPW = Variable Percentage Withdrawal, an absolutely brilliant strategy for making sure you don’t run out of money in retirement and don’t leave a lot on the table. Read all about it here. ↩︎

With all ETF trades being free, I hold very little actual cash in any of my accounts. ↩︎