As mentioned elsewhere, I try to keep about 5% of my retirement savings in what I loosely refer to as “cash”. Of course, it’s not cash, cash doesn’t earn any interest, and that would drive me bonkers. Instead, I’ve been using ZMMK and ICSH (two of my ETF all-stars) to serve this purpose. I made a more detailed assessment of available products at the time over here.

But Global X (a company who I do a lot of business with, thanks to XEQT, XGRO and HXT) has launched 4 products that invest solely in US Treasury Bills.

TSTX/TSTX.U/TSTX.F: all based on 1-3 year treasury bills, which, in common bond lingo, is “short” duration. TSTX is the one that’s probably of greatest interest to most of you since it trades in CAD. TSTX.U is the same thing but it trades in USD, and TSTX.F trades in CAD but uses currency hedging to smooth out the CAD/USD exchange rate1.

TLTX/TLSX.U/TLTX.F: same idea as above, but these products are based on 20 year T-Bills, which would be considered “long” duration and are much more sensitive to changes in the prime interest rate.

They are brand spanking new (launched Oct 7, 2025), but have already paid out their first distributions at the end of October:

CAD ETF Distribution

USD (.U) ETF Distribution

Hedged (.F) ETF Distribution

TSTX family (1-3y)

0.14090

0.13991

0.13990

TLTX family (20y)

0.16056

0.15943

0.15941

The TSTX family is paying 3.4% yield, which is way better than any CAD product I’ve evaluated previously2. It’s not as good as USD HISAs, but being able to get US-like interest rates in a Canadian denominated product is a cool thing. T-Bills of this duration are not super sensitive to changes in interest rates, but the 20y ones would be. TSTX is a product I’ll be keeping an eye on as an alternative to ZMMK, potentially, as long as the prime rate in the US remains significantly higher than Canada’s.

Reduced Fees for CNDX (S&P/TSX 60 index)

Global X was running a promo this year that I talked about previously, but they’ve set a new low price for their flagship Canadian index fund at 0.09% MER starting in 2026. (The MER is 0% at the moment). I don’t hold CNDX myself (I use XIC and VCN, which both include all of the TSX and costs 0.06%), but if you like to focus on the larger part of the Canadian market, you may want to take a look here.

I don’t like hedging as a rule, as it just adds cost and I figure that over time, the USD/CAD exchange rate is reasonably stable. ↩︎

And if these ETFs existed at the time, I probably wouldn’t have looked at them because they have a duration that’s a little too long for me to consider them “cash-like”. But I like my “cash” to be cashflow positive, with no downsides. ZMMK and ICSH aren’t guaranteed to do that, but their super-short average duration (90 days or so) makes it far more likely. ↩︎

In a previous post, I took a look at the major fund companies’ all-in-one-funds with a focus on what passive indices each of them folllowed with regards to Canadian equity, US equity, International equity, and bonds. That assessment found that iShares and BMO were very similar, but TD and Vanguard looked very different.

But do different indices really make a difference in terms of what each of these companies hold when it comes to equities? That’s what we’re trying to find out. Let’s take a look at each of the categories in turn.

Canadian Equity

Let’s take a look at the top Canadian equity holdings of TEQT, XEQT, ZEQT and VEQT1:

Stock

TEQT %

XEQT %

ZEQT%

VEQT%

RBC

1.65

1.73

1.62

1.80

Shopify

1.55

1.69

1.62

1.49

TD

1.12

1.16

1.10

1.16

Enbridge

0.84

0.88

0.85

0.92

Brookfield

0.82

0.82

0.78

0.81

BMO

0.74

0.77

0.72

0.77

Agnico

0.66

0.69

0.68

0.63

Scotiabank

0.64

0.67

0.63

0.68

CIBC

0.60

0.63

0.60

0.63

CP KC

0.57

0.58

0.57

0.62

# held

292

215

215

156

Top 10 %

9.19

9.62

9.17

9.51

Top Canadian Equity Holdings for TEQT, XEQT, ZEQT, VEQT per ETF factsheets, October 2025

VEQT has fewer holdings than the others, and this indicates slightly more concentration/slightly less diversification than the other funds. TEQT is at the top of the heap when it comes to the number of companies held, with XEQT and ZEQT looking pretty similar. My take here is that the differences between TEQT/XEQT/ZEQT/VEQT are pretty slight when it comes to Canadian equity. The Canadian equity indices these funds track may be different, but the differences are pretty minor, and might simply be attributable to tracking errors; how often and when these funds rebalance their holdings may explain the differences shown here.

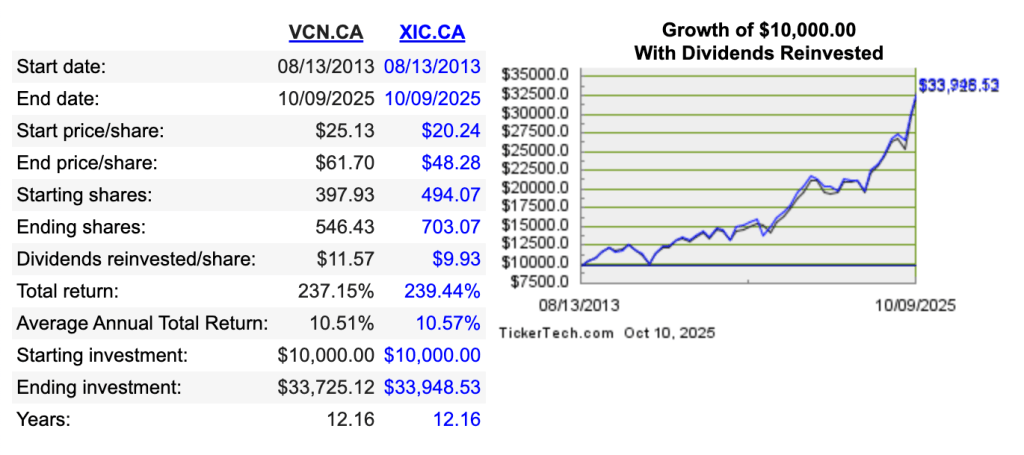

But just for fun, I looked at comparing VCN (which is underneath VEQT, and tracks the FTSE Canada all cap) to XIC (which is underneath XEQT, and tracks the S&P/TSX Capped Composite) and found this using https://www.dividendchannel.com/drip-returns-calculator/ (which is also listed in Tools I Use).

This indicates a tiny advantage to XIC aka the capped composite index, but there’s not a lot of daylight between these two returns!

On the Canadian Equity front, I declare the 4 funds EQUIVALENT!

US Equity

The US weighting is NOT the same for each of these funds, so making a one-to-one comparison is a bit tricky.

TEQT: 55% US

ZEQT: 50% US

XEQT, VEQT: 45% US

What I show in the table below is the percentage of the US portion held by the fund. So in other words if stock XYZ makes up 5% of the US holdings of TEQT and XEQT, it means that TEQT actually holds more of XYZ because 55 cents of every dollar of TEQT is invested in XYZ as compared to 45 cents for XEQT et al.

Stock

TEQT: TPU %

XEQT: XTOT %

ZEQT: ZSP/ZMID/ZSML%

VEQT: VUS%

NVIDIA

7.81

6.91

7.35

6.45

Microsoft

6.62

5.71

6.26

6.02

Apple

6.38

5.53

5.99

5.54

Amazon

3.73

3.24

3.45

3.49

Broadcom

2.75

2.38

2.51

2.23

Meta

2.74

2.33

2.51

2.56

Alphabet Cl A

2.43

2.07

2.26

1.97

Alphabet Cl C

2.13

1.67

1.82

1.59

Tesla

2.12

1.80

1.91

1.46

JP Morgan

1.46

1.24

1.36

1.29

Eli Lilly

1.25

1.00

1.09

1.00

Berkshire

1.15

1.33

1.47

1.43

# held

504

2494

1511

3524

Top 10 %

38.17

32.97

35.54

32.74

Top US Equity Holdings for TEQT, XEQT, ZEQT, VEQT per ETF factsheets, October 2025

What’s clear here is that TEQT is an outlier insofar as it only focuses on the largest US companies, with the other three funds including smaller companies. This also impacts how much money is found in the top 10 US holdings of TEQT, with 38% of holdings invested in names like NVIDIA, Microsoft, Apple et al.

This has proven beneficial of late since smaller US companies have not kept pace with the larger ones. Per spglobal.com, the 10 year performance as of Oct 13, 2025 of the three US market segments has been:

S&P SmallCap 600 = 7.65%

S&P MidCap 400 = 8.49%

S&P 500 = 12.75%

Meaning that any fund that holds smallcap and midcap US stocks has had their returns dragged down in the past 10 years.

So my conclusion for US Equities is that TEQT is the performance champion, but this comes with a less diversification than the alternatives: not only does TEQT focus on the highest-performing portion of the US equity market, it also puts more money overall into the US equity market. This has worked well for the last ten years, but it’s anybody’s guess as to whether this is a good idea for the future.

International Equity

The International2 weighting is NOT the same for each of these funds, so making a one-to-one comparison is a bit tricky.

TEQT: 20% International

VEQT: 25% International

ZEQT: 25% International

XEQT: 30% International

BMO gets the “lack of transparency” award from me for their complex structure. ZEQT holds ZEA which holds European stocks as well as IEFA, which is their USD fund holding the same things. It also holds ZEM which holds emerging markets stocks as well as EEM, which holds similar things in USD. Nowhere can you find a BMO/ZEQT consolidated view like what I’m showing below.

Like in the previous examples, what I show in the table below is the percentage of the International portion held by the fund.

Stock

TEQT: TPE %

XEQT: XEF/XEC %

ZEQT: ZEA/IEFA/ZEM/EEM%

VEQT: VIU/VEE%

Taiwan Semi

0

1.73

5.88

4.19

ASML

1.98

1.43

2.11

1.59

SAP

1.43

1.03

1.37

1.14

Nestle

1.30

0.93

1.24

0.96

Roche

1.24

0.87

1.12

0.95

Novartis

1.24

0.90

1.17

0.98

AstraZeneca

1.24

0.93

1.26

0.94

HSBC

1.15

0.83

1.22

1.02

Shell

1.11

0.80

1.09

0.87

Toyota

1.06

0.70

0.97

0.85

Siemens

1.02

0.77

1.08

0.82

Tencent

0

0.80

2.75

2.10

Samsung

0

0.37

2.03

1.16

Alibaba

0

0.40

1.87

1.59

# held

893

5626

3864

3524

Top 10 %

12.77

10.25

20.89

15.68

Top International Equity Holdings for TEQT, XEQT, ZEQT3, VEQT per ETF factsheets, October 2025

Here you see some pretty significant differences. BMO and Vanguard (especially BMO’s ZEQT) have a much heavier emphasis on “emerging” markets than XEQT does; TD’s TEQT has NO exposure to emerging markets at all.

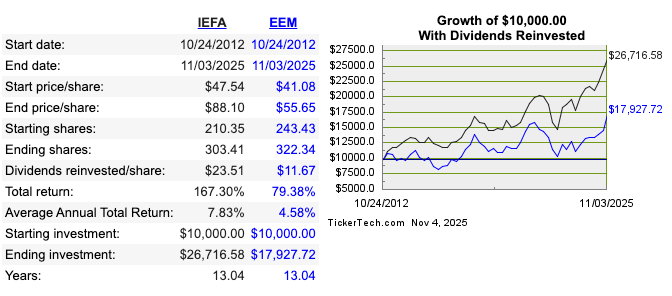

That’s an interesting strategic choice being made here. Let’s compare emerging market performance to mature international markets. We cand do that by looking at IEFA (mature markets) versus EEM (emerging markets)4:

Emerging markets have been a serious lag to global performance, so perhaps TD is on to something here. I played with this chart quite a bit and it’s only very lately (last 2 years or so) that emerging markets have outperformed the established ones. Long term trend? ZEQT certainly hopes so.

So on the international front, you have choices

TEQT only focuses on mature markets

XEQT allows some (not much) exposure to emerging markets

ZEQT and VEQT make much bigger bets on emerging markets

Which is the correct call? TEQT historically has made the right choice, but as the old adage goes “past performance does not guarantee future results” (or something like that).

I’m using the all-equity versions of these to make the comparison more apples-to-apples. VEQT has a larger Canadian percentage (30%) than the other 3 (25%), so I muliplied VEQT’s holdings by 25/30 to make the comparison meaningful. ↩︎

In this analysis, I’m not making a distinction between “mature” and “emerging” markets. Some of the funds do. In all cases, “International” means “no US, no Canada”. ↩︎

I’ve been making monthly posts about the current interest rates available via “Series F” High Interest Savings Accounts (HISAs) and HISA-like ETFs for a while now. These are an excellent place to park your money. My current broker, Questrade, gives me access to HISAs, but they are not free to trade, hence of zero interest1 to me — I use HISA-like ETFs instead, some options I uncovered earlier this year are discussed over here.

Anyway, I’ve decided to make things a bit easier and make the HISA table a permanent fixture at the Money Engineer. You can always find the most recent version of the table over here: https://moneyengineer.ca/hisa-and-short-term-bond-table-canada-us/, so feel free to bookmark it. (It’s a submenu of the DIY Investors menu found under All Readers.) I’ll generally make updates to it any time the interest rates change in Canada or the US, which they did last week.

If ever I’ve missed an update, or you see a problem, always happy to hear from you — just shoot me a note.

Insert joke about falling interest rates / typical big bank interest here. ↩︎

You can read about my asset-allocation approach to investing over here.

The view post-payday

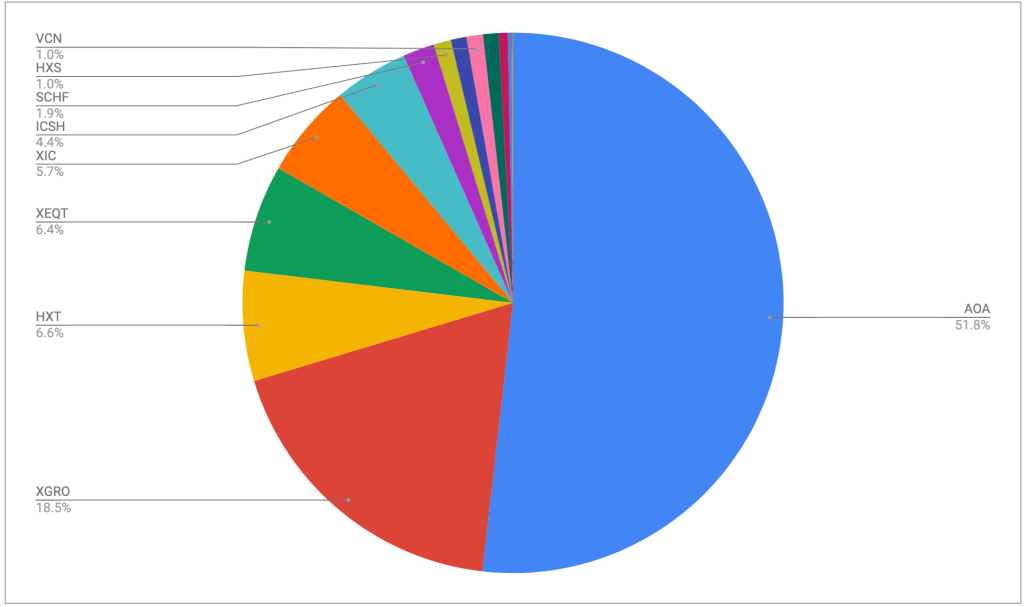

I pay myself monthly in retirement, so that’s a good trigger to update this post. On October 27th, this is what it looks like:

The portfolio is dominated by my ETF all-stars; anything not on that page is held in a non-registered account and won’t be fiddled with unless it’s part of my monthly decumulation. Otherwise I’ll rack up capital gains for no real benefit.

No massive changes this month; the one you might notice is a slight shift from AOA to XGRO. I move some of my USD holdings into CAD every quarter, and last month was when I did it. The majority of my spending is in CAD, so I use Norbert’s Gambit to move funds around.

Plan for the next month

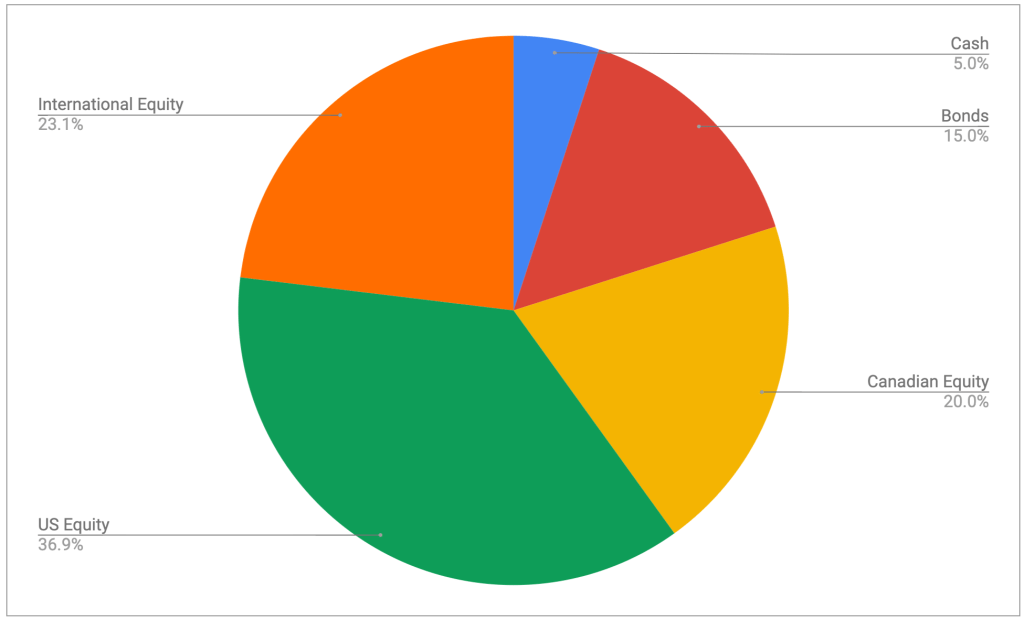

The asset-class split looks like this

It’s looking pretty close to the targets I have, which are unchanged:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds (almost all are buried in XGRO and AOA)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX 60)

36% US equity (dominated by ETFs that mirror the S&P 500, with a small sprinkling of Russell 2000)

24% International equity (mostly, but not exclusively, developed markets)

All looks to be in order from an asset allocation perspective, no need to do anything here.

Overall

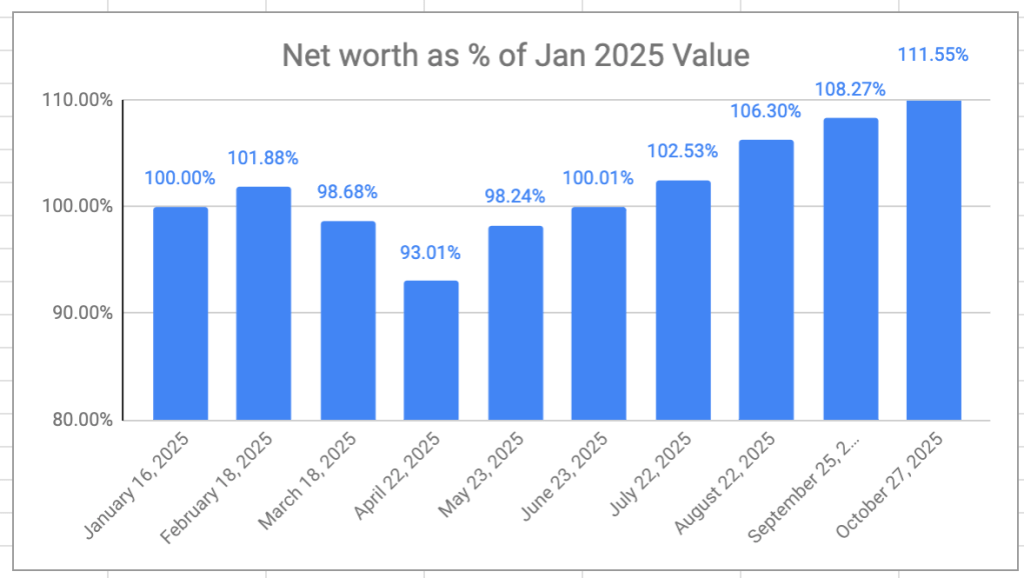

The retirement savings had a great month, again — a 6-month growth streak at this point. Overall, I’m now 11.5% ahead of where I started even though I’ve been drawing a monthly salary since the beginning of the year. I don’t really expect the winning streak to continue, but VPW allows me to take some benefit from the frothy stock markets at moment.

Net Worth as a percentage of starting point

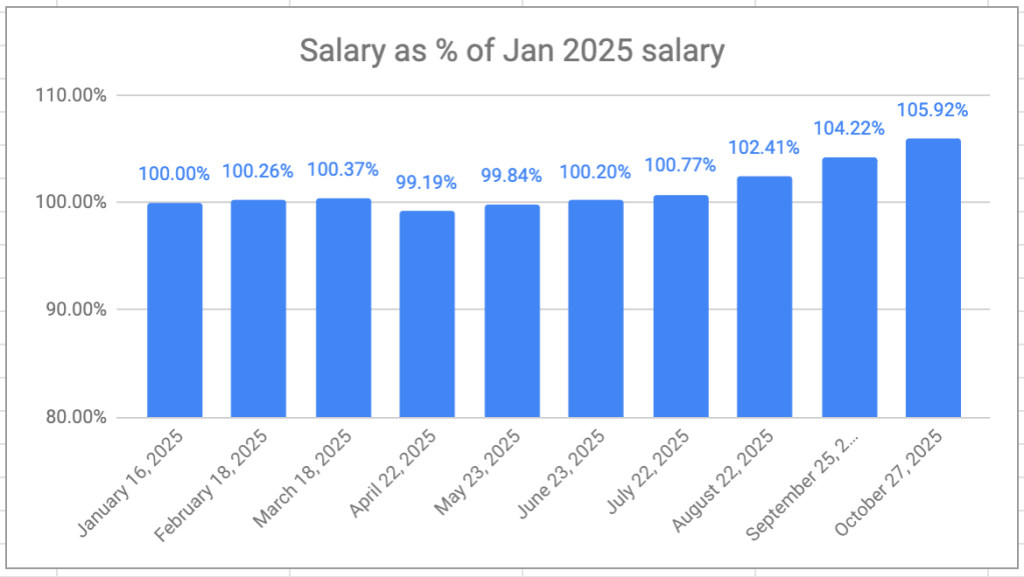

My VPW-calculated salary has hit a new high this year, 5.92% higher than my first draw in January. The monthly salary is also on a 6-month growth streak.

Monthly Salary as a Percentage of Jan 2025 salary

The months ahead will see the final “goodbye” to QTrade1 as the last of my RRIF investments will move to (mostly) Questrade2.

I didn’t have a great deal of issue with QTrade as a provider, but their support (lack thereof) was beginning to become irritating. ↩︎

My own QTrade RRIF will join the RRIF holdings I already have with Wealthsimple. They remain a potential backup provider of my retirement savings. I would have moved more to take advantage of their cashback promotion, but they still, inexplicably, do not support self-directed spousal RRIF accounts. ↩︎

I have financial relationships with 4 different brokers, soon to be reducing to 2, if things go according to plan:

My long-term relationship with QTrade will come to an end by the end of the year as I move the last of my RRIF accounts out1

Questrade holds the vast majority of my retirement savings; they will inherit most of my remaining QTrade holdings this year2

Wealthsimple holds a small percentage of my retirement holdings, normally because I’ve been chasing a particularly attractive promotion (free money, or last year, a free MacBook Air)

My mother’s estate is held by BMO Investorline and if all goes according to plan (CRA willing), I’ll be done with them early next year as the estate wraps up.

I mention all this because I sometimes get wind of new developments from these providers in near-real-time, if they chose to share those developments with their existing clients. You benefit by hearing about them at the same time I do.

QTrade joins the realm of commission-free brokers

Starting October 28th, QTrade is eliminating trading fees on ALL stocks and ETFs, bringing them in line with Questrade, Wealthsimple, Desjardins, and National Bank. This, combined with their reasonably generous cash back offer3 that runs until the end of the year, makes them a serious contender for your investing dollars. Read more at https://www.qtrade.ca/en/investor/campaign/cashbackoffer.html.

Questrade to ditch Passiv in favour of home-grown tool

One of the things I like about Questrade is their support for Passiv, which I covered here. The main thing I like about Passiv is the integrated dashboard that can span both mine and my spouse’s accounts, especially since Questrade’s native support of Authorized Traders is absolutely abysmal.

This week I received an email from Questrade with subject line “Your Passiv integration will be changing soon”.

Uh-oh.

Anyway, in what I suppose is an effort to make their product “stickier”, Questrade appears to be working on their own Passiv-like “Portfolio Monitoring and Rebalancing Tools”, which are supposed to launch “in 2026”. As a result, the current annual access to Passiv Elite will end at the end of the current renewal date, or on January 30, 2026, whichever is later.

Passiv Elite4 is the tier of Passiv that can do rebalancing trades on your behalf. It’s not a feature I really cared about since Passiv doesn’t model all-in-one ETFs the way I think about them. You might say Passiv is an alternative way of getting the benefits of all-in-one ETFs without actually holding them.

Passiv Elite is $99/year, (which is a bargain compared to the cost of all-in-ones), so I’d expect Questrade’s own tools to be bundled into some tier of their current Questrade Plus offering.

No action required at this juncture, but I’m very curious as to how Questrade’s intended offer will work…and what it will cost.

I would have moved everything back in March, but I hit a snag concerning how RRIFs work. In essence, there’s no support offered for changing RRIF providers mid-year. Once the RRIF calculation has been done for the calendar year, your current broker is obligated to pay out the RRIF minimum. If you decide to move RRIF providers mid-year, the current RRIF provider still has to pay you your RRIF minimum for the entire year before allowing the transfer. Read about it here: https://moneyengineer.ca/2025/03/27/cautionary-tale-changing-brokers-when-you-have-a-rrif/↩︎

I think this is what I have, currently. I became a Questrade client just before the launch of Questrade Plus and probably got access to the “full” Passiv experience for the current year (March 2026 to be exact) by virtue of the assets Questrade has under their management from me aka “Questrade Elite”. ↩︎