Summary: High Interest Savings Accounts (HISAs) are a way for cash to earn half-decent, risk-free interest. These “Series F” HISAs are likely available through your online broker, but you may have to ask how to get at them, exactly.

The high interest savings account (HISA1) is a different animal than the bank accounts offered by the likes of Simplii, Tangerine, EQ, or Wealthsimple2. The bank accounts are more intended for very short term savings for day to day use. They frequently offer attractive promotional rates for new clients. And while these are all good ways to earn a few extra bucks on cash in your account, it’s not the focus here.

The HISAs I’m talking about are usually only offered via a broker, and many of the DIY brokers3 allow you to purchase the so-called “Series F” version of these, which do not have any hidden trailer fees. They are “special” bank accounts insured by CDIC4 that pay rates that are tied to the overnight rates. When those change, expect the HISA rates to follow suit.

There was a mini-explosion in ETFs that invested in HISAs: CASH and HISA are two examples5. I never bothered with these since they weren’t free to trade on QTrade and trading costs would be a significant drag on the ROI.

Part of my investment philosophy is to have 5% of my overall holdings in cash (as for the rest, it’s 15% in bonds, 80% in Equity). And so I’m quite motivated to have some sort of real return6 from my cash position since it is a measurable part of my net worth.

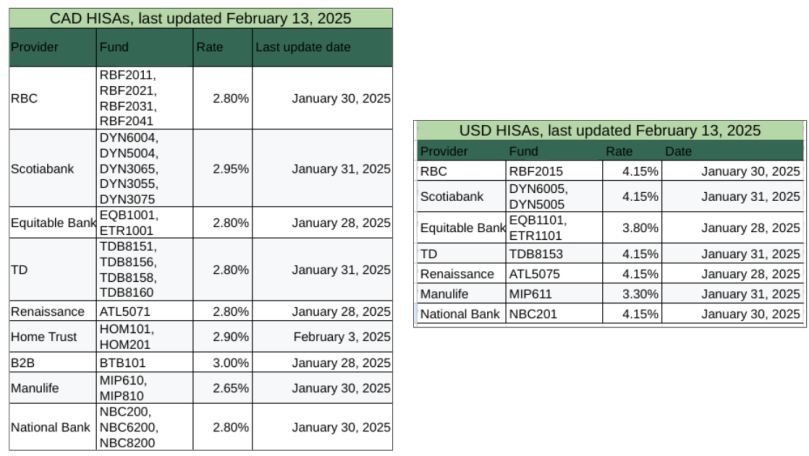

So I do pay attention to the ups and downs of the HISA rates. And I figured I’d share them with you:

There’s also a Google Sheets version with a bit more detail (source links) if you prefer.

Hopefully most of the fields are self-explanatory. The “fund” column shows the identifier you would need to use to actually trade the HISA on your trading platform. How to access it will vary by provider. QTrade hides their HISAs in the “Mutual Fund” tab which is incorrect; these are not mutual funds, but are often modeled that way in the DIY platforms.

For Canadian Dollar HISAs, Scotiabank7 has been usurped! They have long been the highest-paying provider but the title now falls to B2B bank: https://b2bbank.com/advisor-broker-rates/banking-rates.

For those of you who hold US cash in your brokerage accounts, you can benefit from the much higher US interest rates8, and you have multiple choices since multiple providers are paying the same rate.

Before taking the leap and trading in HISAs, I was surprised by how they were handled on QTrade. There were a few differences possibly specific to QTrade, but pay attention to how your provider handles HISA trades:

- QTrade considers holdings in HISAs part of your cash position for the purposes of buying stocks and ETFs9. If you successfully complete a trade that exceeds your ACTUAL cash position (i.e. cash NOT in the HISA) you will also have to sell the correct amount of your HISA to get rid of the negative cash balance in your account and avoid interest fees

- HISA trades are not tracked in the “orders” tab of QTrade10 so be careful that you don’t inadvertently trade the same thing twice

- QTrade limits all HISA purchases to $1000 minimum; there are no restrictions on sales, and there are no fees for either buying or selling HISAs.

Does your DIY broker give you access to other funds? Let me know about them at comments@moneyengineer.ca!

- An aside about the image chosen for this post…I pronounce the acronym HISA….and it’s on a TABLE, get it? ↩︎

- Looking at these websites, I may have to consider breaking up with CIBC for my day to day banking… ↩︎

- QTrade and iTrade definitely allow you to purchase these. Wealthsimple and BMO Investorline do not. Wealthsimple as a matter of course offers pretty competitive rates for any cash floating around in your account, especially if you have over $500k with them. BMO Investorline has high interest savings too, but you access to their product only (BMT104). ↩︎

- My personal bias is that I don’t much pay attention to CDIC-insured or not. I figure if major Canadian banks start failing, I had better make like Survivorman, because no insurance is going to save me. Perhaps that’s naive. ↩︎

- Great names for both, by the way ↩︎

- That’s return above the current inflation rate. Hiding money under a pillow would typically earn a negative real return, equal in magnitude to the current inflation rate. ↩︎

- All my cash holdings are in DYN6004 or DYN6005. ↩︎

- US Fed has not been as aggressive in cutting interest rates as compared to Bank of Canada. ↩︎

- Since I don’t have a margin account, if I try to buy something I don’t have the money for, I’m normally strongly discouraged from doing so with a clear warning. ↩︎

- BMO Investorline is the king of confusing handling of cash positions in your account. ↩︎