**** Update: Per email communication on October 24 2025, as of January 31, 2026, Passiv will not be offered at all by Questrade, as they are planning to launch their own “integrated portfolio monitoring and rebalancing tools”.

**** Update: As of June 1, 2025, Passiv Elite is no longer offered for free for Questrade Clients. It’s now part of a subscription service called Questrade Plus***

As you may have heard, I’m in the middle of a transition between online brokers1. And so I’ve been spending some more time getting to know what Questrade offers to the DIY investor besides free buying and selling of stocks and ETFs.

One thing I looked into lately was Passiv, a service that is offered for free for all Questrade clients.

In brief, Passiv is a 3rd party web application2 that allows you to track your investments from a single screen, no matter if they are found in multiple investment vehicles (e.g. TFSA, RRSP, RRIF) or if they are found across multiple providers (full list of supported brokers is here)3.

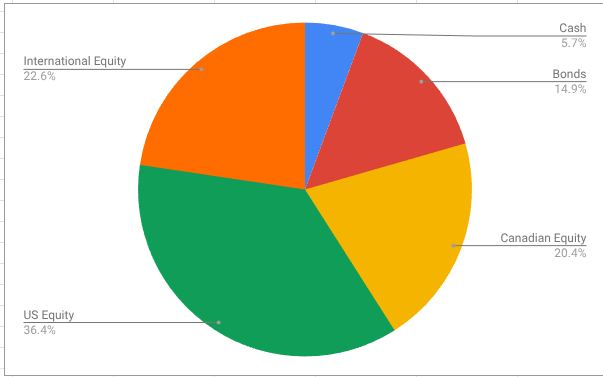

What’s more, it also evaluates your portfolio against a model that you define. For example, if you (like me) have an investment portfolio with a target allocation of 5% cash, 15% bonds, 20% Canadian equity, 36% US equity, and 24% international equity, Passiv can assess your current holdings against these targets, and even do the trades to rebalance the portfolio!

Astute readers will note these are a lot of the same benefits I’m a fan of — and one of the big reasons most of my portfolio is invested in all-in-one asset allocation ETFs. (Are these ETFs unfamiliar? You can read about them here.)

I tried to use Passiv to model my own portfolio, but discovered that all-in-one asset allocation ETFs aren’t really supported by the tool4. Once I thought about it some more, it’s clear why — Passiv really markets itself as an ALTERNATIVE to using all-in-ones. Here’s a clear marketing pitch from Passiv that demonstrates its approach: https://passiv.com/feature-posts/model-portfolios-that-cost-less-than-all-in-one-funds-or-robo-advisors.

So to get the full benefit of Passiv, instead of holding XGRO, you would instead hold the constituent components of XGRO, a fund I’ve broken down previously. This would save you some management fees over time. Passiv helpfully does the math to calculate how much here5.

As a certified cheapskate, I’m always interested in saving a bit of money. But there are some downsides I could see in the Passiv approach:

- You have to actually DO the rebalancing now and then. Not a big deal, but a fund like XGRO does this as part of their offer6.

- You have to do the rebalancing no matter what. By this I mean that you have to buy when others are selling, and sell when others are buying. You can’t get overly attached to any one segment of your portfolio, because then you start making bad decisions based on “gut instinct”. Humans are notoriously bad at this7.

On the plus side, you will definitely save on management fees, and you could certainly tweak the contents to avoid products you wouldn’t normally buy (e.g. XGRO has some hedged funds, which I don’t like, typically).

An unknown for me is how foreign exchange is handled. That’s always something I consider since a lot of my retirement savings are in USD. Some experiments required 🙂

Anyway, it’s given me something to think about. I’ll have to see how easy it is to use in practice once all my accounts are back in place. Any Passiv users out there? I’m interested in your take — just drop a line to comments@moneyengineer.ca.

- And some (not all) of the funds are now showing up in Questrade, about 3 weeks after starting the process. Switching providers is not for the impatient. ↩︎

- WARNING: they don’t have an app. But someone named “Pasiv” does, and it looks very similar. ↩︎

- Other benefits include tracking of dividends, performance charts, etc. All stuff Questrade is apparently not very good at. ↩︎

- One asset class per stock symbol. My home-grown spreadsheet supports dividing symbols by asset class. ↩︎

- The calculation doesn’t include Passiv’s fees for the service, which are waived if you are Questrade client. ↩︎

- Per BlackRock “XGRO’s portfolio will be monitored relative to the asset class target weights and will be rebalanced back to asset class target weights from time to time at the discretion of BlackRock Canada and/or BTC. Generally, XGRO’s portfolio is not expected to deviate from the asset class target weights by more than one-tenth of the target weight for a given asset class.” [source] ↩︎

- If you’re interested in how behavior shapes investing, https://www.looniedoctor.ca/2024/12/13/etf-investor-behavior/ is a very good introduction to the topic. ↩︎