I’m in the middle of my transition from QTrade to Questrade. With 11 different accounts to migrate, most of my time has been spent with their new account setup screens, but I have already taken note of a few differences that I’ve noticed between the two in my first week of using Questrade.

Trading fees on stocks and ETFs

Questrade recently announced that they were eliminating commissions on the buying and selling of all stocks and ETFs. QTrade has a decent list of free to trade ETFs, but obviously Questrade is the winner here.

Personally, I don’t think this will make a huge difference for me since my retirement portfolio is mostly based on QTrade’s “free” list (most notably XGRO and AOA), but it’s not fully in that camp. I’ll save a few bucks over the course of the year thanks to this.

Support

Those of you who read my mini-review of QTrade will know that I don’t consider their support a strong suit1.

I encountered quite a few snags2 along the way with Questrade’s account opening process, and as a result I have spent some time dealing with their support team.

One big difference you see right away is that they seem to rely exclusively on chat, with very clear (if sometimes disheartening3) queue position metrics. I myself am a fan of chat, especially one that makes it very clear where you are in the queue. Compared with QTrade, no contest — I’ll take keeping a window open on a computer I’m using over having to listen to highly compressed and repetitive hold music any day of the week!

A technical quibble I have with Questrade’s chat is that it is inconsistently persistent as you navigate the Questrade screens4. On more than one occasion I had my chat closed accidentally because I navigated to the “wrong” screen. Compared to other support chat platforms I’ve used (Rogers, for one), it’s decidedly feature-light.

The support I eventually got was uneven. I suppose last week may not have been the best week to attempt calling Questrade5, but all the same, sometimes the answers I got made no sense or were just flat out wrong.

US Dollar Account Support

Both companies are strong in this regard, allowing USD holdings in various accounts. Personally, I hold USD-denominated assets in my RRIF and my non-registered accounts. (I also used to hold USD assets in my TFSA, but because of the non-preferred tax treatment of dividends held in TFSAs, I got rid of those a few years ago).

The big difference that’s obvious immediately is while QTrade keeps the USD and CAD accounts separate — different account numbers, different screens to navigate — Questrade combines CAD and USD assets in one account. This has the pleasant side-effect of reducing the total number of accounts I have.

I haven’t investigated (yet) how values of accounts and portfolios are reported in Questrade6. I’m expecting that they will allow you to see your account and portfolio values in either USD or CAD7.

One of the irritants I had with QTrade is that they never, ever showed the USD/CAD exchange rate they were using to display the overall CAD value of the portfolio. It appeared they were using a rate that was consistently 1.5% below the spot rate.

And another irritant I had with QTrade is that I could not get RRIF payments natively in USD, something I was told was possible before I opened the RRIF in the first place8. Questrade claims they allow this on their public website, so I’m hopeful. More to come at the end of this month, hopefully.

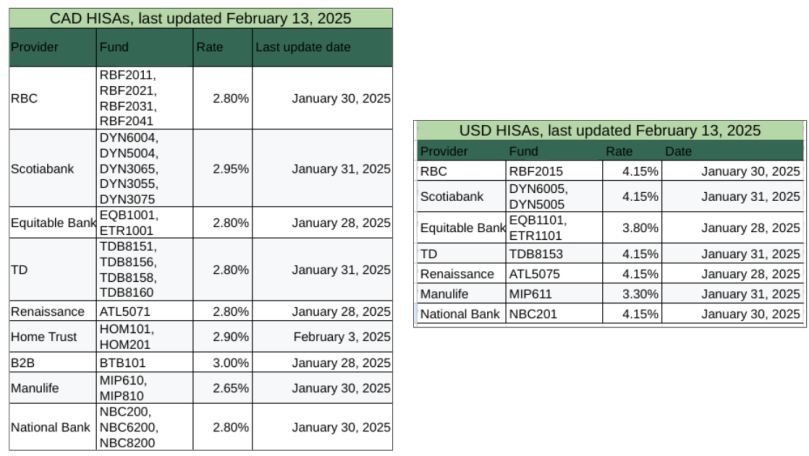

HISA support

High Interest Savings accounts are an important part of my portfolio holdings since my decumulation strategy depends on them. QTrade has an extensive list of free to trade HISAs (I covered them here) but Questrade doesn’t provide access to this class of product. Instead I have to use ETFs. But since all ETFs are free to trade on Questrade, this shouldn’t really make a big deal of difference. In some ways, it’s better because QTrade restricted HISA purchases to a minimum of $1000, whereas most of the cash-oriented ETFs have an entry price of either $50 or $100 per unit.

I find it difficult to get answers to super-specific questions about various platforms, so if you have questions about any of the platforms I use/ have used (namely, BMO Investorline, Interactive Brokers, Wealthsimple, QTrade and Questrade), then feel free to ask away at comments@moneyengineer.ca.

- For an example of coherent and attentive customer support, you’d have to look at Wealthsimple ↩︎

- Their website appeared to be getting crushed at times…weird sporadic and non-repeatable error messages ↩︎

- Last week on one of my calls, I started at position 370 or so. That was a 90 minute wait. But at least I could write blogs while I waited, something that is really irritating to do when you have to listen to hold music. ↩︎

- Possibly browser-related, but c’mon, it’s 2025 and I was using OSX Safari! ↩︎

- RRSP season, and their generous promo ending… ↩︎

- I have accounts, but until the in-kind asset transfer completes, I have no assets. ↩︎

- Taking a peek at the mobile app while I write this, I see options for account balances to be reported as “Combined in CAD”, “Combined in USD”, “CAD” and “USD” so it appears my expectations will be met. ↩︎

- After two months (!) of back and forth with QTrade, I was told — last week — that this is possible using the exact same method I unsuccessfully attempted in January. ↩︎