Summary: Vanguard asset allocation funds aka all-in-one funds VEQT, VGRO, VBAL, VCNS. VSIP have reduced their management fees to 0.17%, down from 0.22%, effective November 18, 2025.

It’s a good time to be an all-in-one investor, as I am. New to all-in-ones? Read all about them here.

The summary pretty much says it all. It just got cheaper to own Vanguard’s all-in-one funds. The amount of the reduction amounts to 50 cents for every $10001 invested per year, but compounded over many years, and multiplied by however much you have saved for retirement, it can be a surprisingly large number.

All-in-ones are much cheaper than either roboadvisors or your typical financial advisor, but as we studied before, they’re not without some cost, so fee reductions are always welcomed. Vanguard joins TD and BMO in reducing the cost of their all-in-ones. We looked at the makeup of each of these funds lately; there’s not a huge amount of difference, no matter which one you pick.

Anyway, you may note that Blackrock’s XEQT/XGRO/XINC family is now the most expensive of the lot; there’s no reason for that to be true given the competitive landscape. I would expect Blackrock to follow suit, or if not, I’ll probably be making some moves to get to lower fees, since a lot of my retirement portfolio is currently tied up in XEQT/XGRO. ZEQT/ZGRO I think is the closest in makeup to the XEQT/XGRO family.

Of course, if you only have $1000 saved for retirement, you have other worries. ↩︎

As mentioned elsewhere, I try to keep about 5% of my retirement savings in what I loosely refer to as “cash”. Of course, it’s not cash, cash doesn’t earn any interest, and that would drive me bonkers. Instead, I’ve been using ZMMK and ICSH (two of my ETF all-stars) to serve this purpose. I made a more detailed assessment of available products at the time over here.

But Global X (a company who I do a lot of business with, thanks to XEQT, XGRO and HXT) has launched 4 products that invest solely in US Treasury Bills.

TSTX/TSTX.U/TSTX.F: all based on 1-3 year treasury bills, which, in common bond lingo, is “short” duration. TSTX is the one that’s probably of greatest interest to most of you since it trades in CAD. TSTX.U is the same thing but it trades in USD, and TSTX.F trades in CAD but uses currency hedging to smooth out the CAD/USD exchange rate1.

TLTX/TLSX.U/TLTX.F: same idea as above, but these products are based on 20 year T-Bills, which would be considered “long” duration and are much more sensitive to changes in the prime interest rate.

They are brand spanking new (launched Oct 7, 2025), but have already paid out their first distributions at the end of October:

CAD ETF Distribution

USD (.U) ETF Distribution

Hedged (.F) ETF Distribution

TSTX family (1-3y)

0.14090

0.13991

0.13990

TLTX family (20y)

0.16056

0.15943

0.15941

The TSTX family is paying 3.4% yield, which is way better than any CAD product I’ve evaluated previously2. It’s not as good as USD HISAs, but being able to get US-like interest rates in a Canadian denominated product is a cool thing. T-Bills of this duration are not super sensitive to changes in interest rates, but the 20y ones would be. TSTX is a product I’ll be keeping an eye on as an alternative to ZMMK, potentially, as long as the prime rate in the US remains significantly higher than Canada’s.

Reduced Fees for CNDX (S&P/TSX 60 index)

Global X was running a promo this year that I talked about previously, but they’ve set a new low price for their flagship Canadian index fund at 0.09% MER starting in 2026. (The MER is 0% at the moment). I don’t hold CNDX myself (I use XIC and VCN, which both include all of the TSX and costs 0.06%), but if you like to focus on the larger part of the Canadian market, you may want to take a look here.

I don’t like hedging as a rule, as it just adds cost and I figure that over time, the USD/CAD exchange rate is reasonably stable. ↩︎

And if these ETFs existed at the time, I probably wouldn’t have looked at them because they have a duration that’s a little too long for me to consider them “cash-like”. But I like my “cash” to be cashflow positive, with no downsides. ZMMK and ICSH aren’t guaranteed to do that, but their super-short average duration (90 days or so) makes it far more likely. ↩︎

Readers will know that I’m a fan of the asset-allocation ETF. In fact, the vast majority of my retirement savings are dedicated to them. (New to the concept of asset allocation ETFs? Here’s an intro.)

Owning asset-allocation ETFs means you can quite literally invest and forget. The target asset allocations are maintained automatically for you, eliminating the all-too-common desire to tinker/experiment/play and mess with your returns in the process.

As with all things investing, there’s no such thing as a free lunch. This automatic asset re-allocation is reflected in the MER1 of the asset-allocation ETFs. So what’s this automatic management actually costing the holder of the all-in-one?

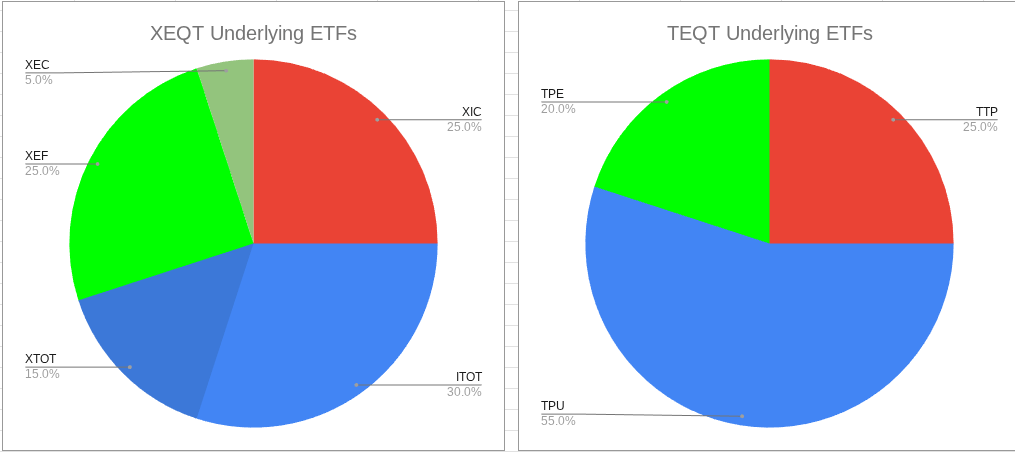

To work out the answer to that question, you have to look at how the asset-allocation ETF in question is built. Some people refer to asset allocation ETFs as “funds of funds” and this is actually quite an apt description, since most asset-allocation ETFs are just constructed by buying up index ETFs issued by the same company.

For example, iShares and TD each have an all-equity asset allocation ETF, named XEQT and TEQT2, respectively. Here’s what’s actually under the hood of each of them:

(I tried to keep the colours consistent between the two: red is Canadian equity, blue is US Equity, and other colours are international equity).

The thing about the MER of an all-in-one is that it already includes the MERs of the funds from which it is built. The tip-off is phrases like this one in iShares’ literature:

…MER includes all management fees and GST/HST paid by the fund for the period, and includes the fund’s proportionate share of the MER, if any, of any underlying fund in which the fund has invested…

What this means is you can work out what the MER would be if you decided to simply manage the underlying funds yourself, and in so doing, figure out the premium that the all-in-one is adding to the mix.

The MER costs I’m talking about here are lower than a factor of 10 (at least) that what’s charged by typical investment advisors and bank-backed mutual funds

The cost premium of the all-in-one is small, but it’s higher than I expected; even small percentage differences are greatly amplified when you work out (say) the 10 year cost of using these products.

The alternative of managing the constituent parts can be a cheapskate alternative and can save real money over time8, but one must beware of

The added complexity inherent in managing a portfolio of multiple ETFs. The XEQT/TEQT example is the simplest one; if you add bonds to the mix (e.g. XBAL/TBAL) you will need to add a few more ETFs to replicate the all-in-one. I used to manage my portfolio without using all-in-ones. I enjoyed it (you may have noticed I have a deep interest in investing). In retirement I have chosen to be practical and have attempted to create an environment that won’t be cognitively overwhelming as I get older.9

The greater likelihood of straying from the plan due to inaction or emotion kicking in. I myself didn’t put a lot of credence to this argument, but people smarter than me have pointed out that this is probably the one biggest factor that derails investment plans.

The MER (Management Expense Ratio) is the cost of operating the ETF, expressed as a percentage. You don’t directly pay MER fees, but they reduce the overall returns of your investments. Lower MERs = more money for you. ↩︎

Just multiply. Watch those decimal points, though. ↩︎

I’m ignoring trading costs which aren’t zero but ought to be very small. Rebalancing assets is necessary of course but is perhaps a monthly, quarterly or annual exercise. ↩︎

And even a portfolio just based on all-in-ones may prove to be too much to handle at some point. I’ve started to pay a bit more attention to the services offered by robo-advisors. ↩︎

Summary: BMO has reduced fees on its family of asset-allocation ETFs (ZCON, ZBAL, ZGRO, ZEQT) to put its Management Expense Ratio (MER) in the same realm as competing families from GlobalX, iShares and TD.

Low-cost all-in-one ETF providers, and the symbols you can use to buy them

In my view, any of these families are worthy of your investment dollars. Which particular fund you pick within a family depends on your tolerance for volatility and/or your timeline for needing the money you’re investing. Each list of fund symbols in the table above is listed in order of amount of equity — so for TD, you can see that TEQT has the most equity (100%) whereas TCON has the least (40%). You might want to give https://moneyengineer.ca/2025/05/06/investment-basics-asset-allocation/ a read to get more familiar with the concepts.

There are other all-in-one families (Vanguard, Fidelity, Mackenzie), the ones shown here are the least expensive of the lot at 0.20% MER or less. TD is the current winner of the lot with a rock-bottom 0.17% MER. ↩︎

There’s also an ESG asset allocation fund, ZESG. ↩︎

There’s also a bunch of covered call variations that are of no interest to me. ↩︎

iShares is the family I work within. I started with them over the others because they could be traded for free on my former provider (QTrade). My current provider (Questrade) allows free trading for any ETF. ↩︎

GlobalX just announced that their Canadian Equity fund CNDX will rebate the management fee for the rest of the year. Up until now, I couldn’t recommend this ETF since prior to this news, its MER was a relatively stratospheric 0.13%1. But 0% is a MER I can live with!

They also have a bunch of their segment ETFs doing the same thing, but I don’t do segment bets. Just asset classes.

I don’t currently own any of this ETF.

Compare Vanguard’s VCE or BlackRock XIC at 1/3 the price. Ok, not letter for letter the same thing, but c’mon… ↩︎