This was the title of a recent webinar I attended via PWL. You can watch it yourself over here: https://www.youtube.com/watch?v=pQl6n4zepys. I don’t think I learned a ton from it — the short answer? “It depends”. “On what?”, you may ask. Here’s some things that influence the answer to the question:

It depends on HOW you live.

Put another way, “what’s your budget in retirement1“? This is a question that many people don’t have an answer to. There’s a few buckets to think about, it’s not intended to be exhaustive:

- Necessities: shelter (and associated maintenance) and utilities(heat, light, water, internet, streaming services, phone), food, clothing, exercise, transportation and associated insurance/maintenance2, taxes (municipal3, federal)

- Medical expenses (drugs, dentists, optometrists, physiotherapy)

- Entertainment (eating out, shows, memberships/user fees)

- Travel (transport, housing, activities)

- Charities

One thing you don’t have to worry about is setting aside money for an RRSP, since once you’re retired, that’s no longer a thing. But don’t neglect the need for a savings fund for unexpected larger expenses. We always keep a “house fund” that gets a monthly payment that we don’t touch for anything other than home renovations or repairs.

Your bank/credit card4 statements5 might be a good place to see what your typical spending looks like.

It depends on where you live

Live in Toronto? Vancouver? Yeah, that’s not cheap. But if you were willing to move to, say, Thailand or a low cost Canadian city, you might be able to spend a lot less on housing. But since most people aren’t willing to uproot, these costs are known, or can at least be reasonably estimated. And if you’re staying put, then will you downsize? When?

It depends on whether you have a pension outside of CPP/OAS

And I’d add, “and it depends if that pension is indexed to inflation”. (The CPP and OAS are, which is why they are great).

It depends on how long you’re going to live

Not predictable, obviously. The oft-cited “4% rule” of retirement assumes a 30 year retirement. That’s living until age 95 if you retire at the “usual” age of 65. When I engaged a financial advisor in the lead-up to retirement, the charts stopped at age 95 as well.

It depends on whether you want to leave an estate to your beneficiaries

Want to die with nothing6? Then you need less money than if you want to leave assets behind. It’s a pretty fundamental question. And if you want to leave assets behind, then how much? And to who? (You do have an up to date will, right?)

It depends on what your CPP and OAS payments are likely to look like

CPP is dependent on how long you’ve been contributing to the plan, up to a maximum that is published annually7. You can take CPP as early as age 60, and as late as age 70, with penalities/bonuses accumulating every month. CPP needs to be applied for before the cheques start rolling in.

OAS is dependent on how long you’ve lived in the country. If you’ve lived here for 40 years or more, then you qualify for the maximum payment of $742.31 at age 65 and automatically starts at age 658 (for most people) unless you specifically ask for it to be deferred.

It depends on how much income you’re intending to make in retirement

The CPP isn’t designed to pay a living wage9. For this reason, many people “ease” into retirement by working part-time or on short-term contracts. This income impacts the answer to the original question — obviously, if you are earning money, then the retirement nest egg can be smaller.

It depends on what your retirement assets are invested in

This, in my view, is frequently overlooked. The fact is that retirement can be quite long, and assets invested in a retirement portfolio still have growth potential. My retirement assets are 80% equities, 15% bonds, 5% cash. This provides me with more growth potential at the risk of having to weather periods of market volatility. I’m comfortable with that degree of risk, but others may not be. Having a lower exposure to equities means your nest egg needs to be bigger.

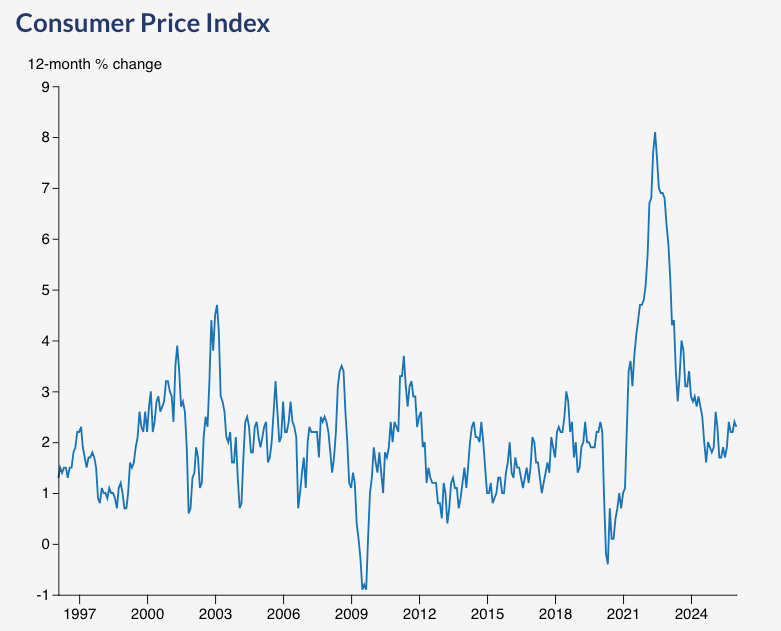

It depends on future inflation

Inflation can fluctuate a lot over the course of retirement. Take the last 30 years as an example:

Inflation is really the biggest concern in my retirement since most of my current income is not inflation-protected10.

My approach? Knowledge and a willingness to be flexible

What kind of knowledge?

- I had a sense of what my budget desires were

- I knew my retirement portfolio was going to stay 80% equities

- I knew I had no pensions outside of CPP/OAS. With advice from my advisor, this lead to the current plan to defer these pensions to age 70 so I can maximize my inflation-protected income.

- My advisor advised me that I had enough saved up that I could retire

But I gained additional, non-data-driven knowledge:

- no realistic plan lasts 30 years11

- that market returns are highly variable12, that inflation is highly variable, that my personal spending budget is highly variable

- that I have always, always, always, adapted to life changes (income, expenses) by either being looser or tighter with money.

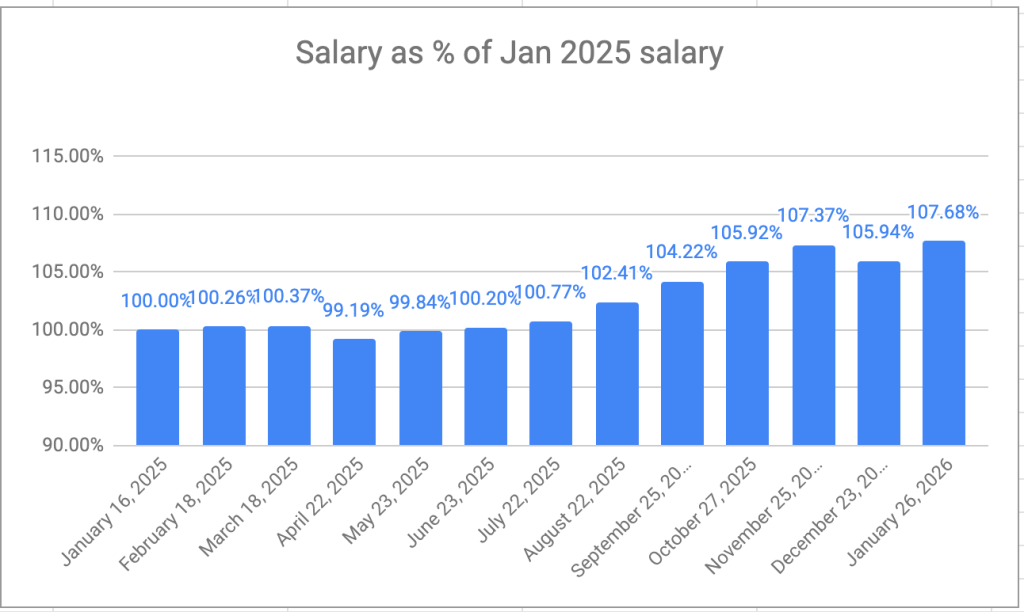

The decumulation strategy I use (VPW, Variable Percentage Withdrawal, talked about here) is deceptively simple, but requires you to be flexible, as your monthly calculated salary is based on your net worth. My salary has generally ticked upwards in the past 12 months, but it could just as easily turn in the other direction in the event of a sustained market downturn. I’ve decided I can live with that. And if you want to see a much longer test in action, check out longinvest’s VPW forward test at https://tinyurl.com/vpwForwardTest.

My final thoughts: be suspicious of a specific answer to “how much do you need to retire”? It depends on so many factors, including your own propensity to adapt to changing conditions, that a simple answer doesn’t seem possible — or reasonable.

- And does it change over time? I expect my budget needs are higher now than they will be in the future, when presumably I’m less able/willing to travel. ↩︎

- If you own a car ↩︎

- If you own a house ↩︎

- A lot of my spending takes place using my credit card so I can collect the free money offered. ↩︎

- A bit crude, but once in a while it flags something for me: https://www.cibc.com/en/personal-banking/ways-to-bank/mobile-services/insights.html ↩︎

- Doing this with 100% accuracy would imply you know the date of your own demise, so probably not a realistic objective ↩︎

- And is currently $1507.65/month if you’re 65 this year. ↩︎

- This one thing I did learn from the PWL webinar: that for most of us, unless you take action, the OAS will start when you turn 65. ↩︎

- Per the CPP website (emphasis mine): “The Canada Pension Plan (CPP) retirement pension is a monthly, taxable benefit that replaces part of your income when you retire” ↩︎

- Owning equities is a sort of imperfect inflation hedge since equity prices, like all prices, are influenced by it. ↩︎

- I’m reminded of the famous quote by Mike Tyson: “Everyone has a plan until they get punched in the mouth” ↩︎

- One year after paying for my retirement plan that informed me I was still three years from retirement, I retired. Why? My retirement savings had blown past “the number” I was advised to hit. And, after a year of retirement, my net worth is 10% higher than when I started retirement. The market sometimes works in your favour. ↩︎