This is a monthly look at what’s in my retirement portfolio. The original post is here.

Portfolio Construction

The retirement portfolio is spread across a bunch of accounts:

5 RRIF accounts

3 for me (Questrade, Wealthsimple)

2 for my spouse (Questrade)

2 TFSA accounts (Questrade)

4 non-registered accounts, (1 for me, 1 for my spouse, 2 joint, all at Questrade)

The view post-payday

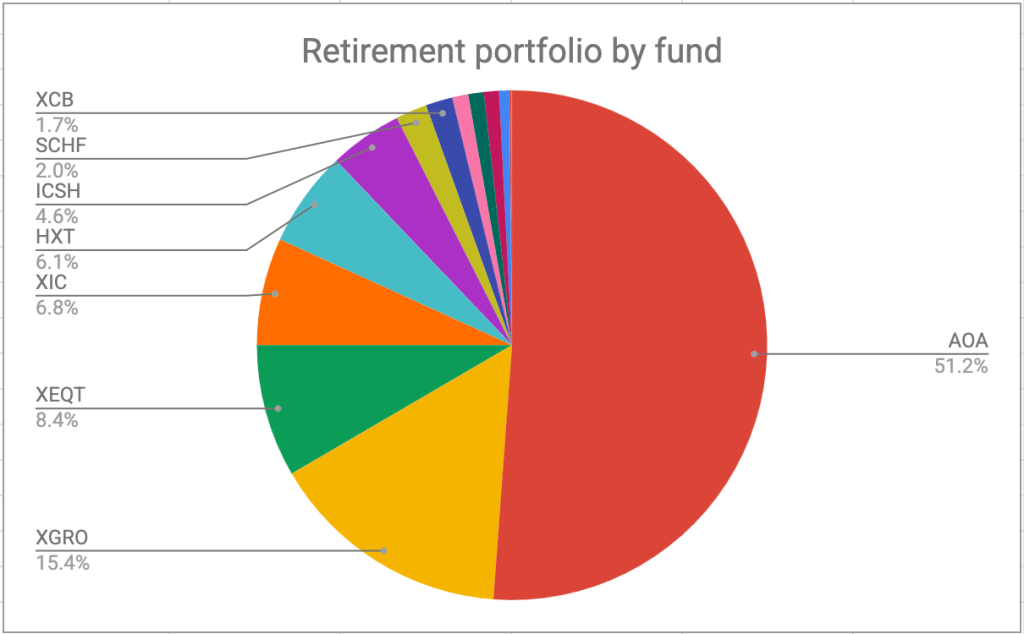

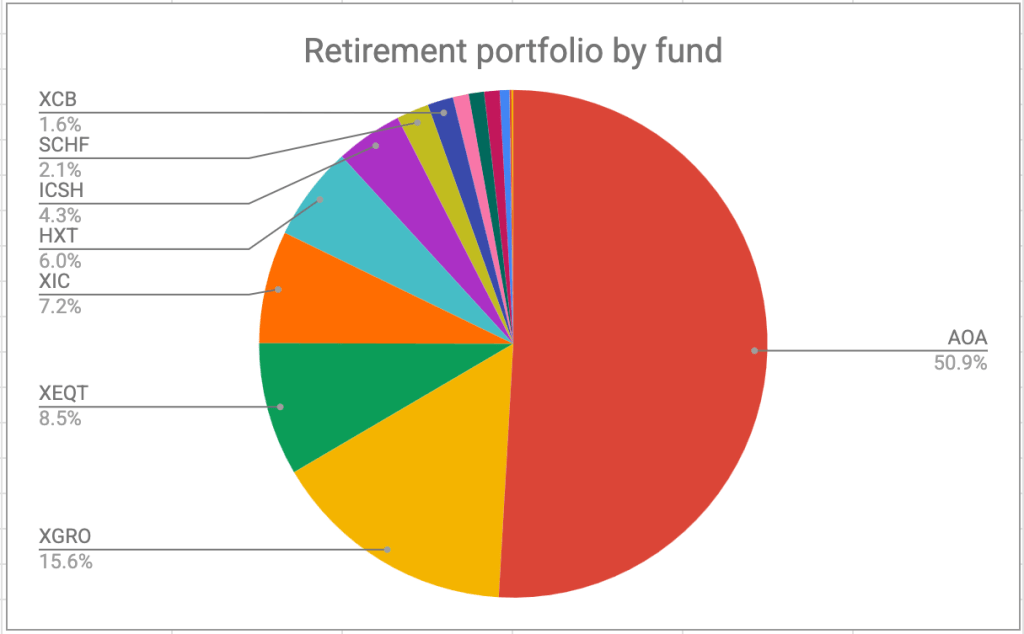

I pay myself monthly in retirement, so that’s a good trigger to update this post. On March 30, this is what it looks like:

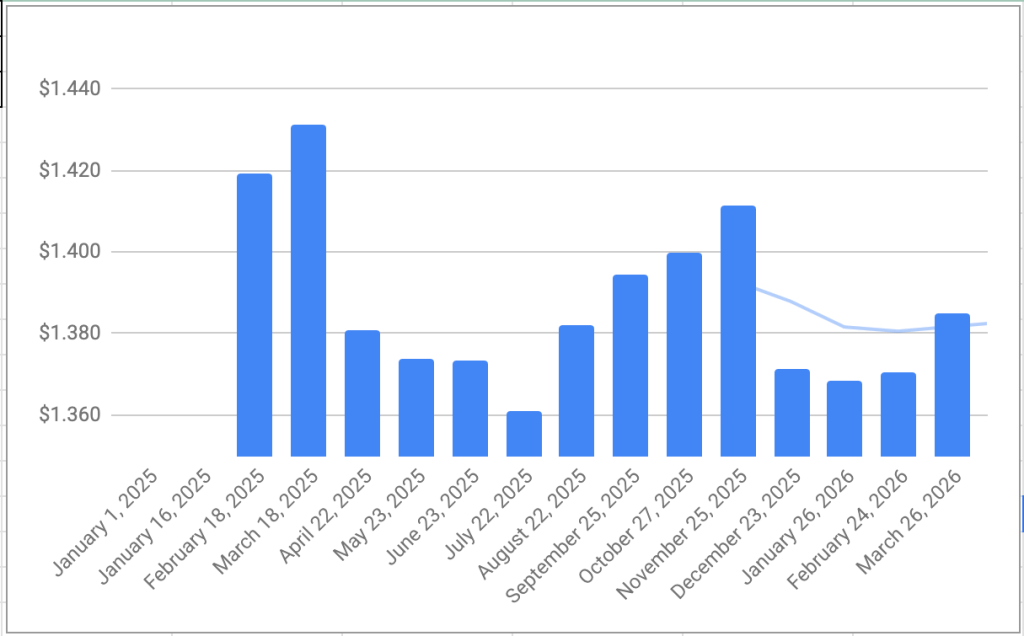

The portfolio is dominated by my ETF all-stars, (and if not an all-star, they are probably on the Magnificent Seven ETFs list). This split is before all the quarterly dividends have paid out. AOA, XGRO, XEQT, XIC all have a quarterly payment that collectively might skew the numbers a bit — I have all these investments on DRIP so I just buy more of the same. All that to say that there weren’t big changes month to month; my USD holdings got a bit of a boost this month thanks to a favourable exchange rate. (A lot of my retirement holdings are in USD, so the FX rates matter somewhat). Here’s what the USD has looked like in CAD since my retirement:

Plan for the next month

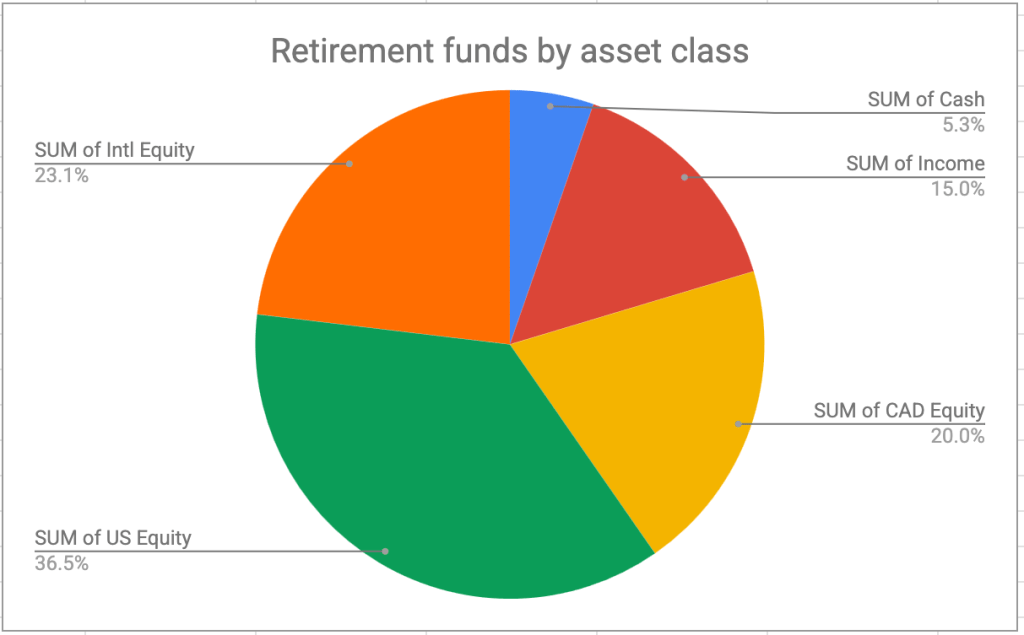

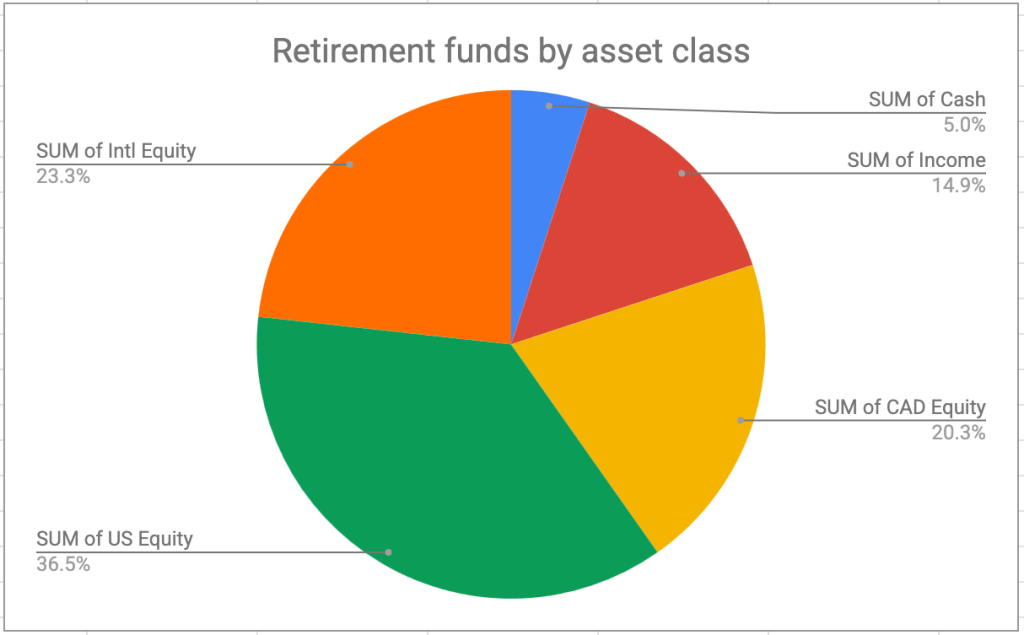

The asset-class split looks like this; you can read about my asset-allocation approach to investing over here.

It’s looking pretty close to the targets I have, which are unchanged:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds/income (most are buried in XGRO and AOA, rest are in XCB)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX — HXT and XIC)

36% US equity (dominated by ETFs that mirror the S&P 500)

24% International equity (mostly, but not exclusively, developed markets)

The alignment with target is what drives my investment decisions; seeing the chart above tells me there’s no movements needed, which makes things simpler.

Since we’re just about in to the 2nd quarter of the year, it’s time for me to move some AOA into XGRO using Norbert’s Gambit1. The Gambit has worked out pretty well for me so far; I track my effective FX rate every time I do it, and it’s always less than relying on the instant (and relatively expensive) FX conversions offered by my broker2.

Overall

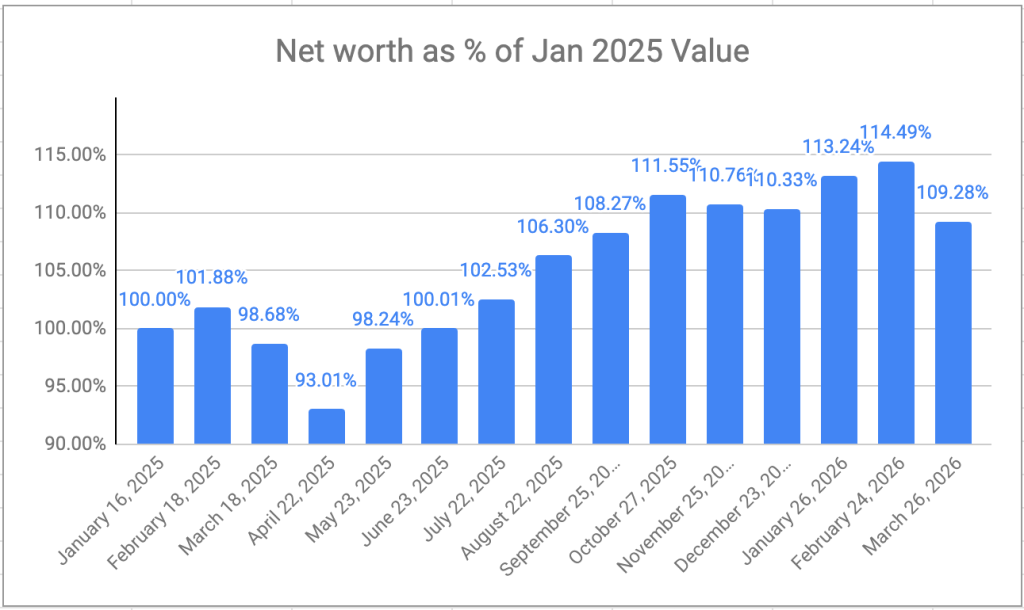

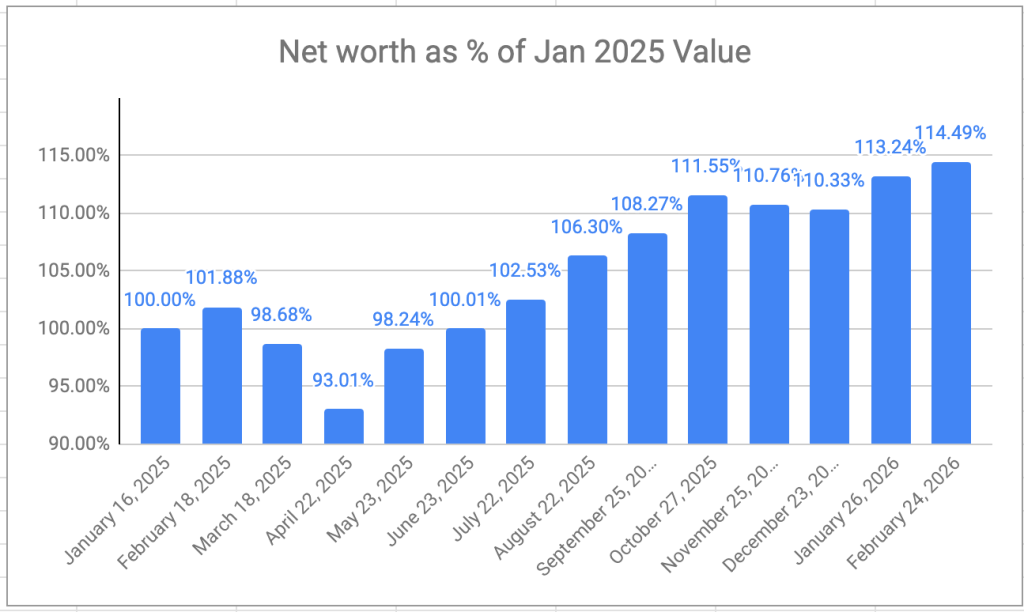

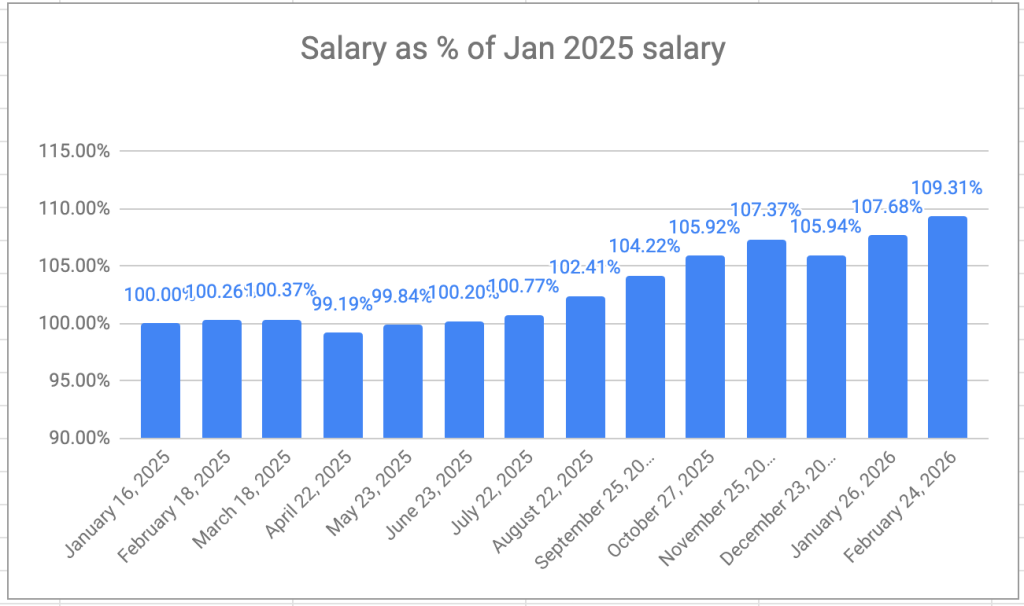

Part of using VPW3 as a strategy is the need to calculate your retirement net worth on a monthly basis. As you can see below, the most recent market gyrations have had a bit of an impact on the bottom line, taking me back to a value I haven’t seen since September last year:

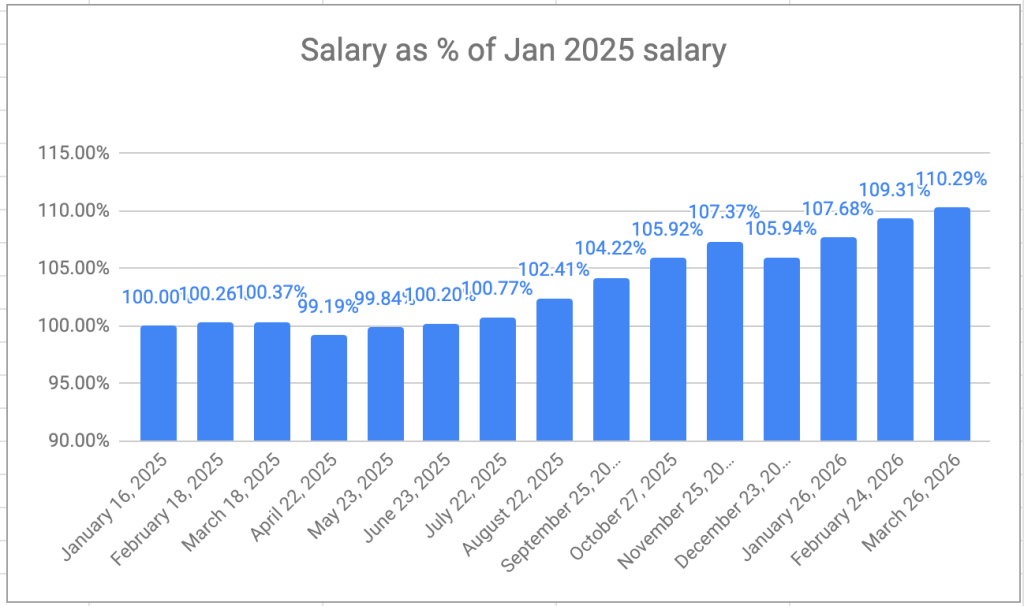

But my VPW-calculated salary, which has a built in shock absorber (aka cash cushion), continued its upward trend nonetheless:

I’m expecting to take a pay cut at some point if the markets fail to recover, but pay cuts are an expected outcome of using VPW as a strategy. The “V” is for “variable”, after all. At this point, I’m still taking over 10% more than I did a year ago, so no matter how you slice it, things are more than on track.

Of late, my need for spending in USD seems not so critical anymore. ↩︎

Both the Bank of Canada and the US Federal Reserve held their main interest rates steady: 2.25% for the Bank of Canada, and between at 3.50% and 3.75% for the US Fed.

This sort of announcement is of interest to investors in such things as HISAs and ultra short term bonds, which tend to track these rates pretty closely. The HISA and short-term bond table (Canada & US) has been updated with this new data.

My current cash strategy (5% of my retirement portfolio, see here for the most recent details) remains heavily weighted to the US side of the ledger since the interest rates are currently better there.

The next chance to see a change in rates will be a month: April 29, 2026 for both entities.

4 non-registered accounts, (1 for me, 1 for my spouse, 2 joint, all at Questrade)

You will notice that QTrade is no longer in the mix. I successfully moved the last RRIF accounts during the month; I learned a lot in the process. QTrade was the victim in the chase for free money offered by Questrade last year; based on current offerings, I’d say that QTrade still has an edge in terms of user experience over Questrade. I’ll go into more detail in a future post.

The view post-payday

I pay myself monthly in retirement, so that’s a good trigger to update this post. On February 28, this is what it looks like:

The portfolio is dominated by my ETF all-stars, (and if not an all-star, they are probably on the Magnificent Seven ETFs list) but if you’ve been following along, you’ll see a few changes.

I dropped XAW since I realized I didn’t need it if I was smarter the ratios of holdings I already owned (XEQT/XIC/XCB). Less is more.

I sold XIC instead of HXT in my non-registered account this month to help pay the bills because I reasoned that eliminating its dividend payouts would be better from a tax perspective2.

Plan for the next month

The asset-class split looks like this; you can read about my asset-allocation approach to investing over here.

It’s looking pretty close to the targets I have, which are unchanged:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds3 (most are buried in XGRO and AOA, rest are in XCB)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX — HXT and XIC)

36% US equity (dominated by ETFs that mirror the S&P 500)

24% International equity (mostly, but not exclusively, developed markets)

I am mulling over making a small tweak to these percentages, increasing US equity exposure at the expense of International equity based on some calculations I’ve done4 but this is neither urgent nor will it be massively impactful to the overall picture.

Overall

There is a bit of an anomaly this month that I should mention. A number of readers have questioned my wisdom of contributing monthly to a TFSA in retirement. From a tax-free growth perspective, it would be far better to make the contribution at the beginning of the year. And many studies have shown that lump sum investing provides better returns than spacing them out. And so, I have taken their advice5 and made all my TFSA contributions for the year this month. And since my TFSA is part of my net worth, there’s a bump being caused by that contribution.

And so, net worth overall is up month over month, a two month winning streak.

One spousal, one individual. One at Wealthsimple because (a) I like their user experience and may consider them as my primary broker in the future and (b) they offered me free money and a laptop to move some fees their way. I can be bought. ↩︎

HXT does not pay dividends and instead uses swap contracts to convert them into capital gains, which receive better tax treatment for me ↩︎

I’ve had the dubious privilege of serving as the executor of the estate of my late mother, who was predeceased by my father. I’ve been documenting my journey along the way (previous instalment here).

This instalment is subtitled “Endgame” because late last week I received a Clearance Certificate from CRA. The Clearance Certificate allows me as the executor to distribute the funds in the estate to the beneficiaries without worrying that the CRA will come knocking on my door at some future date looking for taxes1.

So now it is time to move money around from estate to beneficiaries, close accounts and shred the piles of paper in the filing cabinet. Money exists in three places: a CIBC bank account (not an estate account), a CIBC estate account, and in a BMO Investorline estate account.

CIBC Bank Account

Thanks to the advice of a friend who went through this before me, I had a joint chequing account with my mother. It was her account, and I never touched it, but when she died, the account became mine completely, no different than the other chequing account I hold at CIBC. This arrangement proved very handy in the early days of the estate, as I was able to pay funeral expenses out of this account without being out of pocket myself. The balance was low here, and a few e-Transfers to the beneficiaries later, the funds were cleared. A call to CIBC telephone banking (a surprisingly painless experience), and this account was closed from the comfort of my couch.

BMO Investorline

The vast majority of the estate funds are held at BMO Investorline, since I was acting as my parents’ DIY advisor for about 10 years. When my mother died, her RRIF and TFSA passed to her beneficiaries outside of the probate process (you’ve done this, right? Read more here). Her non-registered funds were converted into a brand new estate account and all the assets were transferred in kind. I could not access this account until I had a probated will. With full access, I eventually converted all the holdings into non-interest bearing cash; all that happened over a year ago (December 2024, to be exact). The account has been largely dormant since then, although I did pay the whopping tax bill for my mother’s Final Return2 from it.

Moving the funds out of BMO Investorline couldn’t be easier; thanks to their AccountLink service, you can write cheques against the cash balance held in your non-registered Investorline account. They do charge $1 for each transaction after the first 2 in any calendar month, so I have to make sure I leave enough cash behind to deal with that3.

CIBC Estate Account

Estate accounts are required to deposit cheques made out to the estate. One possible source of such a payment is CRA4, the other is death benefits from CPP/QPP and/or life insurance policies. My experience with the creation and management of a CIBC estate account was a total disaster. Something that should be relatively straightforward is inexplicably very labour intensive. The reasons are probably only knowable to CIBC, but I’ll give my perspective here:

The workflow has not been updated in decades. Opening an estate account required me to make an appointment at the bank. At this appointment, I sat in a chair in an office while I watched the bank employee type my information into some sort of online form. My involvement at this meeting was limited to producing a death certificate and repeating answers to questions that the bank already had in their systems (my name/address etc etc).

The branch employees do not understand how estate accounts work and they rely on a centrally located help desk to guide them through the process. I know this because the branch employee inadvertently gave me the number to this help desk and the very helpful employee I spoke to there was confused that a customer rather than a branch was calling.

There are no electronic records, no electronic access to estate accounts. Deposit a cheque? Visit the bank. Want the balance? Visit the bank. It’s all very circa 1970.

And, lastly, for all this, they have the gall to charge a $5 monthly service fee for “record keeping”.

Anyway, I am guessing that all the major banks are terrible with estates, but it’s hard to imagine a worse experience than with CIBC.

So, to close this account, I need an appointment (of course). The soonest one I could get at my local branch was a week away. I’ve compiled all the materials needed to unlock the funds (probated will, death certificate, blood sample) so I’m hoping this is a “one and done” kind of visit, but I’m not holding my breath on that one.

What’s especially annoying about the estate account is that it has a relatively small amount of money in it, growing smaller monthly thanks to the monthly service fee.

But this chapter is nearly over. Make no mistake, serving as an executor is a lot of work and requires a lot of patience.

RRIFs and non-registered accounts generate a lot of tax since they are assumed to be sold and converted to income in the hands of the account holder on the day of death. It’s nearly unavoidable, but I wrote a bit about reducing that tax bomb here. ↩︎

I can only imagine how much work it would be should I end up needing to clear a negative balance in a BMO Investorline Estate account. I wouldn’t know where to begin, ↩︎

In my case, the estate tax return had a refund. Not really sure why, one would have presumed that paying thousands of dollars to an accountant would result in a penny-perfect return, but you’d evidently be wrong about that. ↩︎

This was the title of a recent webinar I attended via PWL. You can watch it yourself over here: https://www.youtube.com/watch?v=pQl6n4zepys. I don’t think I learned a ton from it — the short answer? “It depends”. “On what?”, you may ask. Here’s some things that influence the answer to the question:

It depends on HOW you live.

Put another way, “what’s your budget in retirement1“? This is a question that many people don’t have an answer to. There’s a few buckets to think about, it’s not intended to be exhaustive:

Medical expenses (drugs, dentists, optometrists, physiotherapy)

Entertainment (eating out, shows, memberships/user fees)

Travel (transport, housing, activities)

Charities

One thing you don’t have to worry about is setting aside money for an RRSP, since once you’re retired, that’s no longer a thing. But don’t neglect the need for a savings fund for unexpected larger expenses. We always keep a “house fund” that gets a monthly payment that we don’t touch for anything other than home renovations or repairs.

Your bank/credit card4 statements5 might be a good place to see what your typical spending looks like.

It depends on where you live

Live in Toronto? Vancouver? Yeah, that’s not cheap. But if you were willing to move to, say, Thailand or a low cost Canadian city, you might be able to spend a lot less on housing. But since most people aren’t willing to uproot, these costs are known, or can at least be reasonably estimated. And if you’re staying put, then will you downsize? When?

It depends on whether you have a pension outside of CPP/OAS

And I’d add, “and it depends if that pension is indexed to inflation”. (The CPP and OAS are, which is why they are great).

It depends on how long you’re going to live

Not predictable, obviously. The oft-cited “4% rule” of retirement assumes a 30 year retirement. That’s living until age 95 if you retire at the “usual” age of 65. When I engaged a financial advisor in the lead-up to retirement, the charts stopped at age 95 as well.

It depends on whether you want to leave an estate to your beneficiaries

Want to die with nothing6? Then you need less money than if you want to leave assets behind. It’s a pretty fundamental question. And if you want to leave assets behind, then how much? And to who? (You do have an up to date will, right?)

It depends on what your CPP and OAS payments are likely to look like

CPP is dependent on how long you’ve been contributing to the plan, up to a maximum that is published annually7. You can take CPP as early as age 60, and as late as age 70, with penalities/bonuses accumulating every month. CPP needs to be applied for before the cheques start rolling in.

OAS is dependent on how long you’ve lived in the country. If you’ve lived here for 40 years or more, then you qualify for the maximum payment of $742.31 at age 65 and automatically starts at age 658 (for most people) unless you specifically ask for it to be deferred.

It depends on how much income you’re intending to make in retirement

The CPP isn’t designed to pay a living wage9. For this reason, many people “ease” into retirement by working part-time or on short-term contracts. This income impacts the answer to the original question — obviously, if you are earning money, then the retirement nest egg can be smaller.

It depends on what your retirement assets are invested in

This, in my view, is frequently overlooked. The fact is that retirement can be quite long, and assets invested in a retirement portfolio still have growth potential. My retirement assets are 80% equities, 15% bonds, 5% cash. This provides me with more growth potential at the risk of having to weather periods of market volatility. I’m comfortable with that degree of risk, but others may not be. Having a lower exposure to equities means your nest egg needs to be bigger.

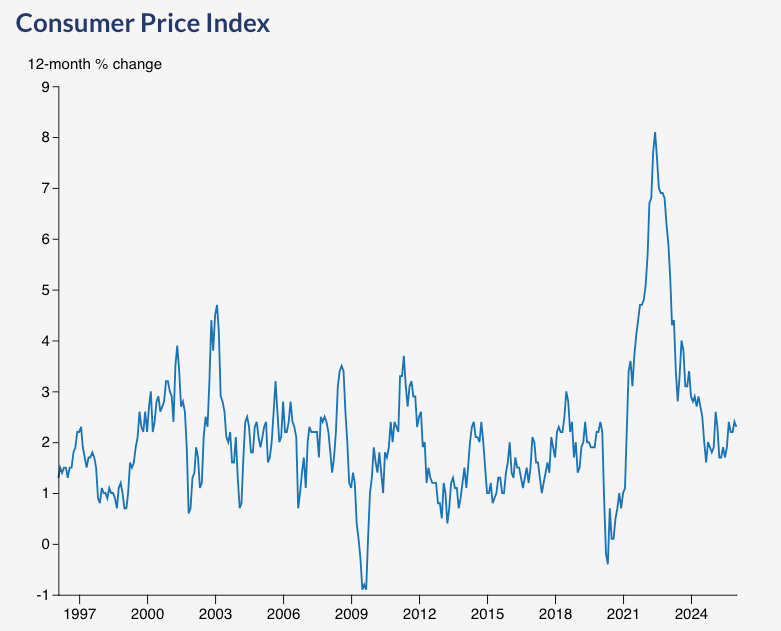

It depends on future inflation

Inflation can fluctuate a lot over the course of retirement. Take the last 30 years as an example:

Inflation is really the biggest concern in my retirement since most of my current income is not inflation-protected10.

My approach? Knowledge and a willingness to be flexible

What kind of knowledge?

I had a sense of what my budget desires were

I knew my retirement portfolio was going to stay 80% equities

I knew I had no pensions outside of CPP/OAS. With advice from my advisor, this lead to the current plan to defer these pensions to age 70 so I can maximize my inflation-protected income.

My advisor advised me that I had enough saved up that I could retire

But I gained additional, non-data-driven knowledge:

that market returns are highly variable12, that inflation is highly variable, that my personal spending budget is highly variable

that I have always, always, always, adapted to life changes (income, expenses) by either being looser or tighter with money.

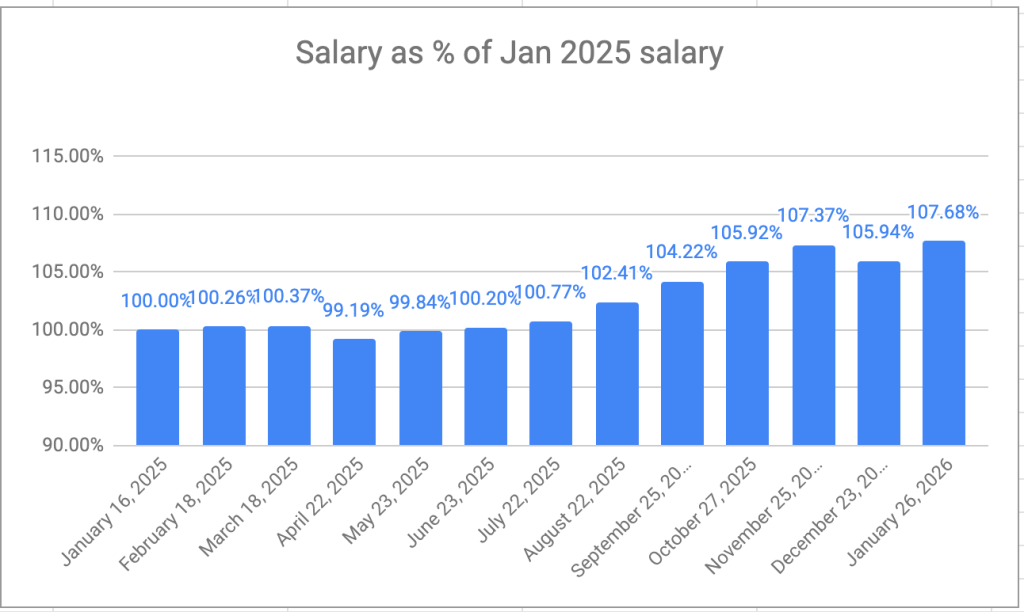

The decumulation strategy I use (VPW, Variable Percentage Withdrawal, talked about here) is deceptively simple, but requires you to be flexible, as your monthly calculated salary is based on your net worth. My salary has generally ticked upwards in the past 12 months, but it could just as easily turn in the other direction in the event of a sustained market downturn. I’ve decided I can live with that. And if you want to see a much longer test in action, check out longinvest’s VPW forward test at https://tinyurl.com/vpwForwardTest.

My final thoughts: be suspicious of a specific answer to “how much do you need to retire”? It depends on so many factors, including your own propensity to adapt to changing conditions, that a simple answer doesn’t seem possible — or reasonable.

And does it change over time? I expect my budget needs are higher now than they will be in the future, when presumably I’m less able/willing to travel. ↩︎

Doing this with 100% accuracy would imply you know the date of your own demise, so probably not a realistic objective ↩︎

And is currently $1507.65/month if you’re 65 this year. ↩︎

This one thing I did learn from the PWL webinar: that for most of us, unless you take action, the OAS will start when you turn 65. ↩︎

Per the CPP website (emphasis mine): “The Canada Pension Plan (CPP) retirement pension is a monthly, taxable benefit that replaces part of your income when you retire” ↩︎

Owning equities is a sort of imperfect inflation hedge since equity prices, like all prices, are influenced by it. ↩︎

I’m reminded of the famous quote by Mike Tyson: “Everyone has a plan until they get punched in the mouth” ↩︎

One year after paying for my retirement plan that informed me I was still three years from retirement, I retired. Why? My retirement savings had blown past “the number” I was advised to hit. And, after a year of retirement, my net worth is 10% higher than when I started retirement. The market sometimes works in your favour. ↩︎