Summary: Asset allocation ETFs1 let you buy exactly ONE fund to meet your investing needs. Buy ONE fund, and forget about it. Really? Really.

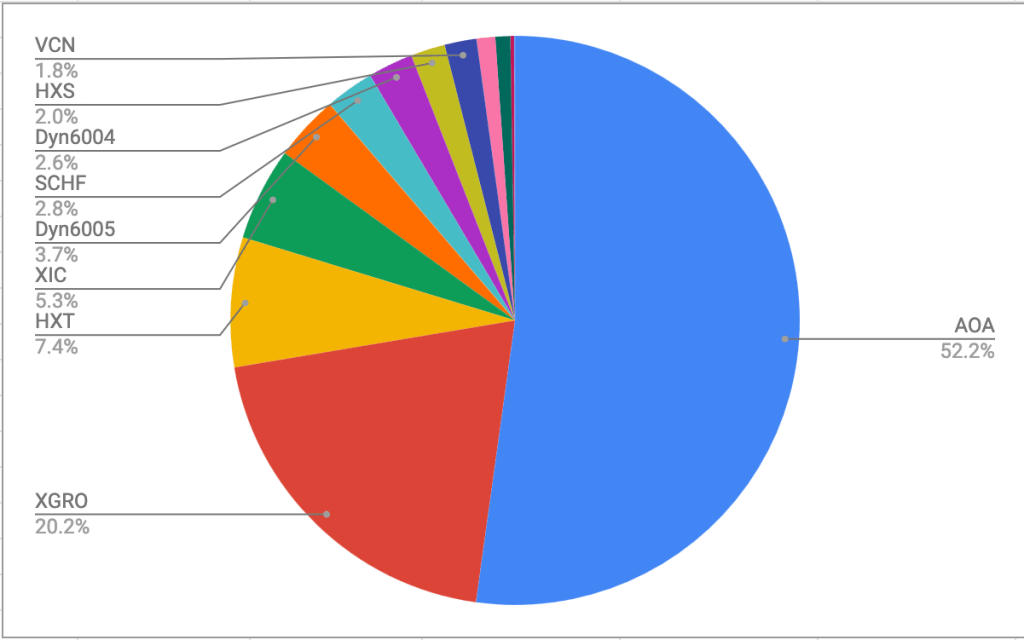

In the run-up to getting ready for retirement, I greatly simplified my portfolio. On the Canadian dollar side, it’s almost all invested in two places: XGRO and DYN6004 (a Canadian high-interest savings account). On the US dollar side, it’s almost all invested in two equivalent places: AOA and DYN6005 (a US high-interest savings account). XGRO is an example of an Asset Allocation ETF that trades in Canadian dollars, whereas AOA is an example of an Asset Allocation ETF that trades in US dollars. The overarching objective of my retirement portfolio is to keep allocations at 5% Cash and the rest in XGRO or AOA. Effectively, this puts me at about 80% stocks.

What’s an Asset Allocation ETF?

Very simply, they are a kind of ETF that allow you to make one investment decision based on your desired risk profile. Risk is a personal decision, based on factors like timeline before needing the money, how much you agonize over stock market fluctuations and so forth.

More risk means better long-term growth prospects means more stocks.

Looking for higher long term growth? Choose an asset-allocation ETF that has a higher percentage of stocks. Looking for lower long term growth with less volatility? Choose an asset-allocation ETF that has a lower percentage of stocks.

There are many Canadian providers out there who provide their own families of asset allocation ETFs.

Which provider you choose may boil down to which is the most convenient / least expensive to buy and sell. For example, BMO Investorline clients can buy and sell the BMO family with no charges, while QTrade clients can trade the iShares family with no charges.

I personally don’t think that there is much to differentiate each of the families. Each provider is just trying to capture your business. So whether you buy ZEQT or XEQT or HEQT or VEQT 2 probably doesn’t matter very much in the big picture.

I summarized them below:

| Provider | ETF Symbols | Read more |

| BMO | 100% Stocks: ZEQT 80% Stocks: ZGRO 60% Stocks: ZBAL 40% Stocks: ZCON | https://bmogam.com/ca-en/products/exchange-traded-funds/asset-allocation-etfs/ |

| iShares | 100 % Stocks: XEQT 80% Stocks: XGRO 60% Stocks: XBAL 40% Stocks: XCNS 20% Stocks: XIC | https://www.blackrock.com/ca/investors/en/learning-centre/etf-education/asset-allocation-etfs |

| Global X3 | 100% Stocks: HEQT 80% Stocks: HGRW 60% Stocks: HBAL 40% Stocks: HCON | https://www.globalx.ca/asset-allocation-etfs |

| TD | 90% Stocks: TGRO 60% Stocks: TBAL 30% Stocks: TCON | https://www.td.com/ca/en/asset-management/insights/summary/all-in-one-td-etf-portfolio-solutions |

| Vanguard | 100% Stocks: VEQT 80% Stocks: VGRO 60% Stocks: VBAL 40% Stocks: VCNS 20% Stocks: VCIP | https://www.vanguard.ca/en/product/investment-capabilities/asset-allocation-etfs |

The magic? Reallocation.

The real magic of asset allocation ETFs is that they do the work of reallocation for you. This is subtle, but crucial. Automatic reallocation takes the emotion out of investing, and means you’re buying low/selling high, every quarter. What?

Take for example XGRO. Per the product brief you can see that its target composition is

- 20% XIC (the TSX 60)

- 36% ITOT (the S&P total US stock market, about 2000 companies)

- 20% XEF (international developed stock market)

- 4% XEC (international emerging stock market)

- 16% Canadian bonds (XBB and XSH)

- 4% Non-Canadian bonds (GOVT and USIG)

The observant reader will note that 80% of this list is made of stocks, divided up over multiple geographies. Anyway, the “target composition” is key here. What this means is that every quarter stocks get bought and sold to re-establish the targets. If the US stock market goes on a tear while the Canadian stock market is tanking, the US gains will be locked in and the Canadian market will get picked up at a discount. It’s a perfect system. No emotion. Just ratios. No work on your part.

What’s the catch?

There is a small cost associated with owning an asset-allocation ETF. Most charge you about 0.20% every year. If you instead decided to own the underlying assets you could probably save on the order of 0.10%. (This is, more or less, what I had in place before I started simplifying my portfolio). But that assumes that you do the rebalancing yourself in a timely way, and the trading fees are negligible.

Wrap up

Asset Allocation ETFs are a great way to get a diversified, risk-appropriate, emotion-free, inexpensive investment portfolio. They are the ultimate tool in the DIY investor’s toolkit.

- Also known as “all in one” ETFs. Also known as “funds of funds”. They all mean the same thing. ↩︎

- Geez, no points for originality on the ETF names… ↩︎

- Global X has additional ETFs on the same page that add leverage to amplify returns. I don’t use them, since the amplification works both ways — in good AND bad markets. ↩︎