As of this morning, this is what the overall portfolio looks like:

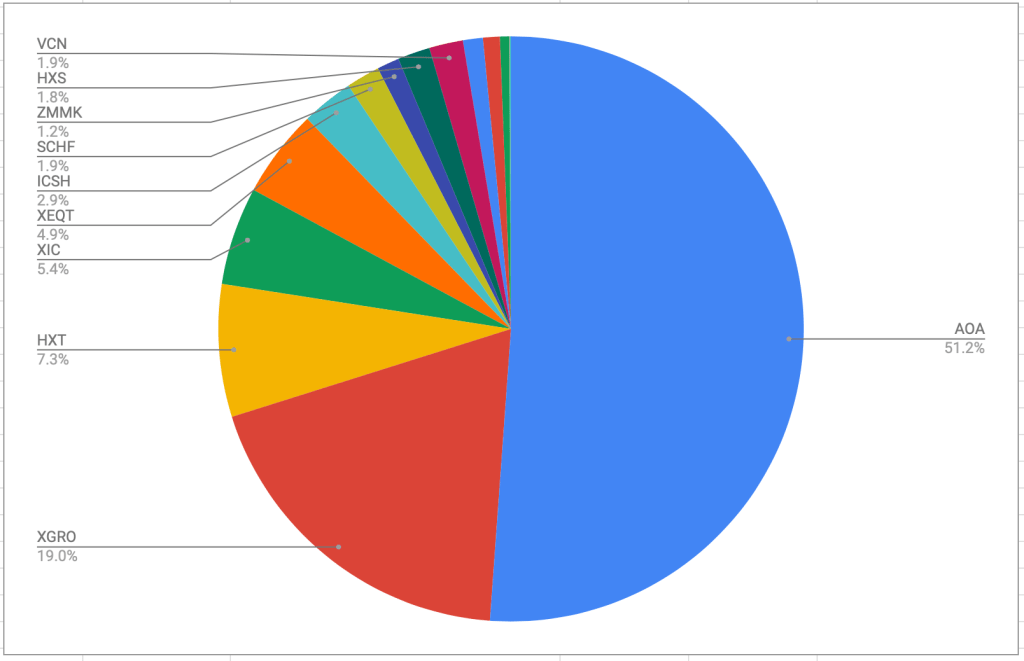

Overall retirement portfolio by holding, April 2025

The portfolio, as always, is dominated by AOA and XGRO which are 80/20 asset allocation funds in USD and CAD, respectively. The rest are primarily either cash-like holdings in two ETFs: ZMMK in CAD and ICSH in USD) or residual ETFs held in non-registered accounts for which I don’t want to create unnecessary capital gains just for the sake of holding AOA or XGRO.

The biggest month over month change was a small decline in AOA and a small uptick in XEQT, about a 1% shift overall. This was because I shifted some of my USD assets to CAD assets in the RRIF using Norbert’s Gambit2. I chose XEQT over XGRO because the contribution of bonds in the portfolio was slightly over my asset allocation target3. XEQT is essentially XGRO, minus the bond holdings (it’s a 100% equity fund).

There was also a noticeable reduction in the contribution of ICSH to the portfolio; this was largely due to the unfavourable change in the USD/CAD exchange rate over the course of the month, and not due to any change in the holdings there.

Plan for the next month

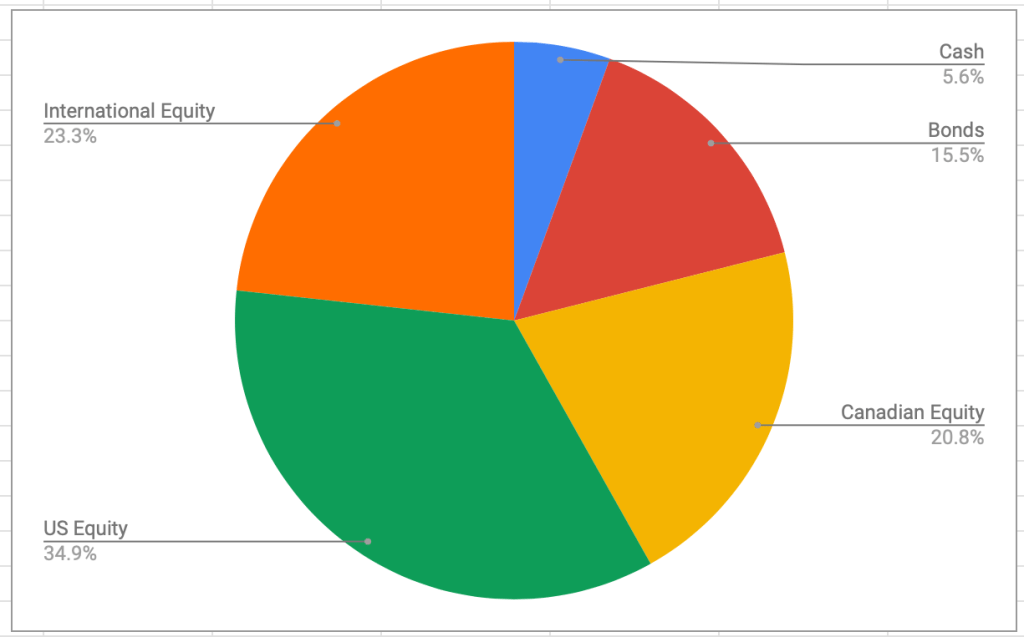

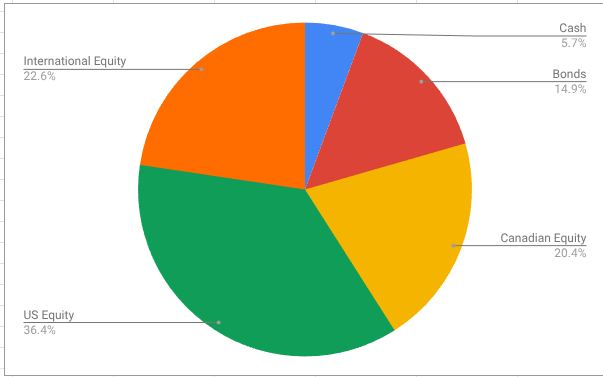

The asset-class split looks like this

Overall retirement portfolio by market, April 2025

This looks to be pretty close to my target percentages which haven’t changed:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds (almost all are buried in XGRO and AOA)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX 60)

36% US equity (dominated by ETFs that mirror the S&P 500, with a small sprinkling of Russell 2000)

24% International equity (mostly, but not exclusively, developed markets)

So, the plan for next month is, do nothing out of the ordinary. Reinvest cash (dividends, TFSA contributions) in one of AOA, XEQT/XGRO, ICSH or ZMMK depending on the asset category most in need on the day of the reinvestment. All these ETFs are covered on my ETF All-Stars page.

Overall

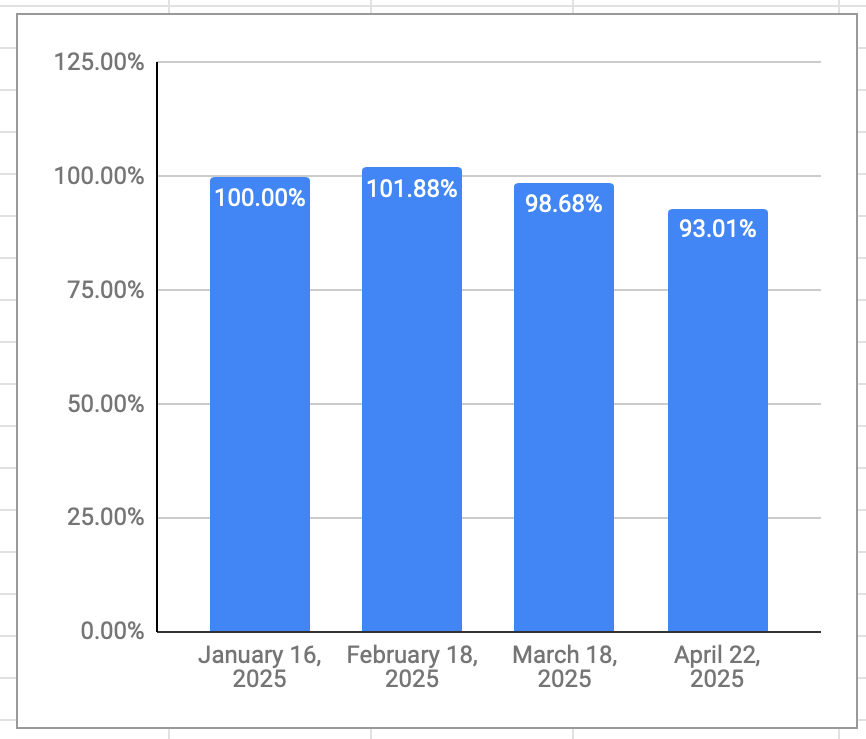

My retirement savings declined 5.75% over the month (down 7% since January) due to the continuing meltdown in the equity markets. It’s not a pretty picture!

Net worth of retirement savings compared to start of retirement

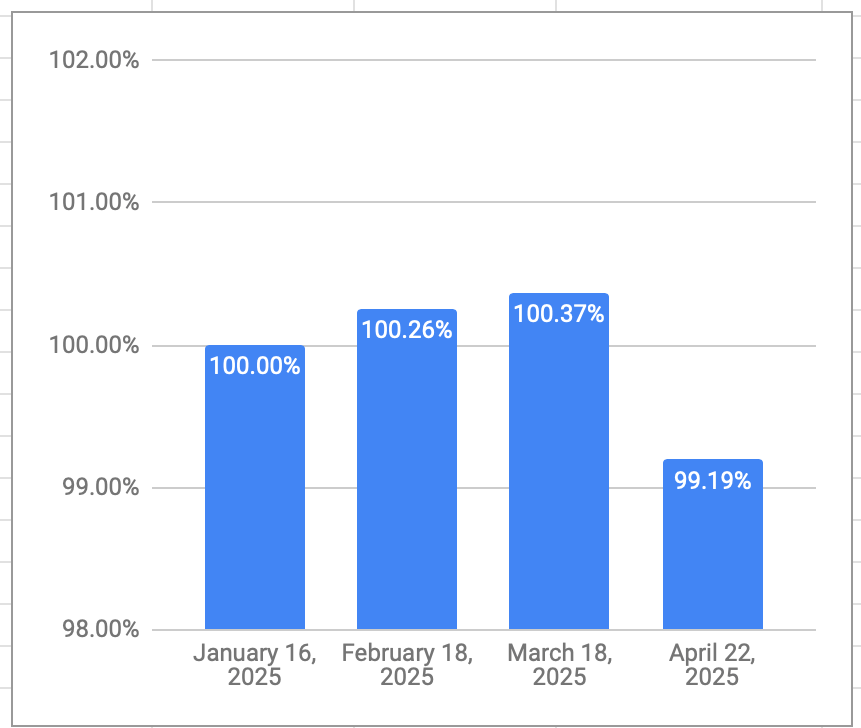

This has not translated to a the same degree of change in my monthly salary. Why? My retirement payouts are calculated by Variable Percentage Withdrawal (VPW), which I cover here. VPW has a built-in cash cushion, which serves to dampen month to month swings in my net worth, either up or down. As you can see in the chart below, my monthly salary has stayed within a 1% band of the first salary I drew in January.

Month over month salary, as compared to start of retirement

Since Questrade combines USD and CAD assets under the same account umbrella, I was able to reduce the number here. ↩︎

I shift funds from the USD to the CAD side of the RRIF more or less quarterly since all RRIF payments are currently coming out of the CAD side of the portfolio. ↩︎

That’s the optimistic point of view; it’s perhaps more accurately stated as “bonds haven’t melted down quite as much as the equity portion of my portfolio”. ↩︎

I’m still wrapping up the estate of my late mother, who died a little over a year ago, a year and a bit after my father died.

My situation

All my mom’s worldly assets were held with BMO Investorline: RRIF, TFSA and a non-registered account. This was a self-directed account; the relationship with BMO (as I came to learn) was pretty informal. Me and my siblings were named as beneficiaries of the estate, and my Mom had taken steps to name us as beneficiaries for the RRIF and TFSA. More details about how that works were covered in a previous post.

First weeks

I had ready access to estate cash because I was named as a joint account holder on my Mom’s chequing account1. This is a very useful thing to have in place, since it can cover expenses incurred after death: funeral costs, moving expenses are two that come to mind. I treated this account as part of the estate, but it allowed me to spend the estate’s money instead of my own for these things.

DIY Estate Handling

Informing BMO Investorline2 of my mother’s death was required, and that took a single call to the general help desk. After about a week I had an initial meeting with their estate department.

Once I provided proof of death, all accounts were frozen and I could no longer even see what was in them. BMOI correctly noted that we were the beneficiaries of the TFSA and RRIF and we started the paper-intensive3work of liquidating and distributing the assets held in those accounts. I checked my notes — it took about 2 months for that step to be fully completed.

What was unexpected was that BMOI gave us ALL the money in the RRIF, with no taxes withheld. From a tax perspective, a RRIF is treated as income in the hands of the deceased on the day they die. For most people, that means a substantial tax bill for that tax year. So as an executor4, I had to be VERY sure that my Mom’s non-registered account could cover the tax bill that would eventually come. Using a tax calculator helped a lot.

The non-registered account, where the bulk of the assets lay, would require a probated will, as I expected. This account remained locked and frozen.

Probate and probate fees

In the very simplest terms, probate means getting a court to certify a will as accurate. And when you think about it, it makes sense that financial services companies want to be VERY sure that the executor (aka estate trustee) is in fact the correct person.

After doing a bit of reading (mostly this source) I decided I could tackle it on my own. This was made significantly easier by the fact that I lived in the same city as my mother, and I had access to a courthouse were I could take my completed forms.

When filing your probate papers, you also have to pay probate fees (aka Estate Administration Tax), which means you have to know the total value of the estate on the day of death. BMOI was able to provide me statements up to that day so I had a to-the-penny accurate assessment of the value held there. BMOI was also able to write a cheque to the Ontario Minister of Finance for these fees using funds available5 in the non-registered account. This meant I wouldn’t have to front the money myself.

Probate fees, in my Mom’s case, were not particularly large (not compared to the estimated tax bill), and since RRIF and TFSA were not part of the estate, they were also lower than they could have been.

After filing, the wait for the court-certified document began. I had very low expectations (I had conservatively estimated a 6 month delay here), but I actually had the probated will arrive in the mail a month later, which was about 4 months after my mother’s death.

Using the Probated Will

With a probated will in hand, I could now unlock the non-registered funds in my Mom’s estate. This required me to open an estate account with BMOI and then transfer the non-registered funds to it. After all that paperwork, I once again had full access to the assets that were formerly held in my Mom’s non-registered account — I could log in to the portal, see the holdings, and most importantly, perform transactions myself at the usual self-directed transaction fees.

I sold all the assets (mostly ETFs, naturally) and partially distributed them to the beneficiaries. Distributing the assets was admittedly (again) more challenging than I thought. Since I was quite familiar with how BMOI worked, I requested AccountLink cheques for the estate account, figuring this would be the easiest way to distribute the funds6. This resulted in a bit of a runaround, but eventually I got a box of cheques sent to me. I held some money back7 so I could pay the 2025 tax bill; this money I invested in a HISA.

Preparing for Tax Season

In late 2024, I removed the remainder of the estate from the HISA account. This was done so as to not have any income generated by the estate in 2025. This simplifies the tax filing considerably.

After doing a bunch of reading, I gave up on the idea of attempting to do the taxes myself. I knew there would have to be both a Final Return (for my Mom) and an Estate Return (aka a T3 return) but I wasn’t really sure about all the steps, and of course CRA’s website isn’t really designed for the layperson to figure this stuff out easily. There was also the matter of filing a CRA clearance certificate. I hired a pro to figure all this stuff out. As it turns out, my Mom’s estate qualified as a GRE Trust, which is, as I understand it, pretty typical. That would appear to offer some potential tax benefits, but I’ll have to wait and see and this point.

It didn’t hold a significant amount of money. Larger sums could conceivably attract the attention of CRA as a bare trust. ↩︎

Actually, mostly filling out PDFs and sending them back over secure messaging ↩︎

If the estate can’t pay the taxes, then the executor is legally obligated to pay ↩︎

Like all matters estate-related, this took a lot of effort. Having sufficient funds when my mother was alive was a very simple process: log on to the portal, sell some shares, wait a few days, get the money. In an estate scenario you have to write a letter of direction to indicate what, exactly, to sell. Then you wait a week or two. Then you get angry at the fact that they charged you $40/trade. Then you write another letter of direction to indicate who to write the cheque to. Then you wait a week for the cheque to arrive. ↩︎

I’m not really sure how the mechanics would work with a broker that doesn’t have bank services. EFT I guess? ↩︎

Probably more than I needed to hold back, but I wasn’t taking chances. ↩︎

As of this morning, this is what the overall portfolio looks like:

Overall retirement portfolio by holding, March 2025

The portfolio, as always, is dominated by AOA and XGRO which are 80/20 asset allocation funds in USD and CAD, respectively. The rest are primarily either cash-like holdings in two ETFs: ZMMK2 in CAD and ICSH3 in USD) or residual ETFs held in non-registered accounts for which I don’t want to create unnecessary capital gains just for the sake of holding AOA or XGRO.

The biggest month over month change is due to switching brokers. My old broker (QTrade) allowed the purchase of HISAs, but my new broker (Questrade) doesn’t seem to offer them4. So I replaced DYN6004 with ZMMK and DYN6005 with ICSH. I made these changes in my QTrade account to avoid any problems with doing an “in-kind” transfer to Questrade.

I’m still in need of USD to pay off some vacation bills, so there is a small hit to SCHF to help out.

Plan for the next month

The asset-class split looks like this

Overall retirement portfolio by market, March 2025

The international equity percentage is below my target of 24%, and so I’ll have to fix that5. VEU looks like it provides exposure to both developed and emerging markets at a rock-bottom price6. XEF would be a perfect fit in the Canadian market, although I should probably also consider XEC to get some emerging markets exposure.The cash position is artificially high because I already did the necessary transactions to get paid out of my RRIF and non-registered accounts (if I did this exercise at the beginning of the month, rather than mid-month, that would disappear). That extra cash will flow to my bank account in the coming days.

A quarterly activity that I’ll be performing this month7 is to shift some of my USD RRIF holdings into my CAD RRIF. I do this to make sure I’m not overexposed to changes in the CAD/USD exchange rate. My current provider reportedly allows me to make RRIF payments natively in USD, so that may be another option to consider. I’ll make an attempt at some point!

One final note: my retirement savings declined 3%8 over the month due to the wild (mostly downward) swings in the stock market, but this leaves me roughly even since my retirement started at the beginning of the year. Here’s the monthly returns for the 2 ETFs that make up the lion’s share of my portfolio9.

XGRO and AOA monthly returns so far

The list is sort-of accurate. I’m in the middle of changing online brokers and since Questrade combines USD and CAD assets in one account, the number of accounts is diminishing. ↩︎

The observant reader will note I also said this LAST month. That was before I decided to switch brokers. Once my holdings settle at Questrade, I’ll revisit. ↩︎

MER = 0.04%. VEU has some Canadian exposure too, which isn’t ideal, but I don’t think there’s a USD ETF that excludes both Canada and the USA. ↩︎

Summary: The spousal RRSP is a great way to reduce current taxes, but if you’re planning on using the money in that spousal RRSP soon, be aware of the rules concerning who declares the income!

Disclaimer: As this article will demonstrate, I’m not a tax expert, lawyer, CPA or anything else. Use with discretion, some assembly required.

I made substantial use of spousal RRSPs during my working life. Spousal RRSPs are a way for the higher earning spouse to take advantage of the lower earning spouse’s unused RRSP contribution room, thus leading to a lower overall tax bill1. All good so far.

Some vocabulary will help with the next bit.

The contributor is the person providing the cash for the spousal RRSP and is the one who gets the tax deduction. Usually this is the higher income spouse.

The annuitant is the person whose name is on the spousal RRSP statements. This is usually the lower income spouse.

What most primers on spousal RRSPs don’t mention is that there is a restriction when it comes to withdrawing from the RRSP2. Paraphrasing the source material:

If the annuitant withdraws from a spousal RRSP within three years of the last contribution, the income from that withdrawal is considered to belong to the contributor, not the annuitant.

What? Why?

As with all things, there’s no free lunch. CRA doesn’t want to make tax avoidance so easy3, so this little detail will prevent the purely hypothetical scenario of a higher earning spouse making a large spousal RRSP contribution in the last year of their employment, and then getting the lower earning spouse to take out that same money at a much lower tax rate when the calendar moves from December to January.

There is one, small, bone that CRA throws our way in this case. Paraphrasing again:

If the annuitant withdrawal is instead made via a spousal RRIF, and the payment is RRIF minimum, then fine, the annuitant can declare that income.

So, as long as our lower income annuitant spouse opens a spousal RRIF, and as long as for the three years4 following the last spousal contribution, that spousal RRIF only pays out RRIF minimums, then all is well. The annuitant spouse declares the income, as expected.

Now of course, this rule may not matter to you. If you’re newly retired and don’t have much in the way of income, then it may not trouble you that you have to declare the income from your spouse’s spousal RRIF/RRSP. It’s just a bit more paperwork (a T2205, looks like).

In my case, I’m only taking RRIF minimums for the time being. So no extra paperwork for me.

I’ve never myself made a withdrawal from an RRSP. That would break my rule of keeping retirement savings firewalled. And it looks to me to be an expensive proposition — your provider will surely charge a deregistration fee, your provider will have to withhold tax, and you have declare the full amount as income in the year you grab it. ↩︎

I have learned to be guided by the humbling tenet of: “If I think I’ve figured out a way to outsmart the taxman, it’s probable that I’m simply demonstrating an incomplete understanding of how it actually works….” ↩︎

To illustrate/clarify: the rule applies in the year the contribution is made, and the previous two years. So the contribution I made in 2024 will be free from all constraints in the 2027 tax year. ↩︎

Summary: The mechanical details of getting paid in retirement require careful review of how your provider allows cash movements between accounts, a handle on how much money is coming in via a RRIF, and, for bonus points, an annual decumulation plan to minimize household taxes.

I covered how I get paid in retirement previously, but this was nothing more than a restatement of how VPW (Variable Percentage Withdrawal) works. My reality is not quite as simple as the Idealized Monthly Routine I laid out in that post.

The actual work required looks more like this:

Actual monthly work needed to get paid in retirement

The first 3 steps are the ones I covered in the last post, and there’s nothing new to talk about there. In brief, you calculate your retirement savings, enter that number into the VPW spreadsheet, and out pops the monthly VPW suggestion (“v”), which is then added to the current value of your cash cushion (“c”) to calculate your salary (“s”).

It’s probably worth noting what specific accounts I hold at my provider to make things a bit clearer1

There are 4 total RRIF accounts (two for me, two for my spouse)

There are 2 non-registered accounts that hold retirement investments (one for me, one for my spouse)

There is 1 non-registered joint account that serves the role of VPW’s cash cushion, which is invested in DYN6004 so I can earn a bit of risk-free interest.

So ideally, my RRIF payments would flow into the cash cushion account, and I would pay myself out of the cash cushion account to my everyday joint chequing account. That is unfortunately NOT how it works.

Let’s pick up the process starting at step 4.

Do the RRIF minimum payments cover the calculated salary?

When I opened my RRIF accounts (and yes, there’s more than one2), one of the questions asked was “what bank account should the payments go to?” Asking for RRIF payments to go to a non-registered account was not presented as an option, and it’s not possible. So already the simple RRIF to cash cushion transaction outlined in the ideal scenario wasn’t possible.

The other questions asked by my provider was: how much do you want to be paid? (RRIF minimum, some percentage/amount higher than that, gross/net?)

(If you’re new to the RRIF world, or if you think that RRIFs are just for 71-year-olds, you may want to check out my previous post on debunking this and other myths.)

The amount each of my RRIFs3 pays me monthly is a well-known fact since I opted to collect RRIF minimum from each RRIF — and RRIF minimum is based on my RRIF value and age as of January 1, 2025. It will stay constant throughout 2025. So while simple, the amounts involved aren’t enough to pay my suggested salary. I’m free to ignore the suggested salary and simply (try to) live off my RRIF minimums, but that would be counter to my “you can’t take it with you” ethos. And so, I have to augment my RRIF minimum salary with money from elsewhere.

If your RRIF minimum payments are higher than the salary, then I suppose it makes sense to re-invest those payments somewhere. Or give the money away. Up to you 🙂

Sell required assets in non-registered account and move $ manually

The title is clear enough — sell something in the non-registered portfolio and use it to make up the salary shortfall. But whose holdings4? Which ones?

To help me decide, at the beginning of the year, I played around with tax scenarios using the calculators referenced in Tools I Use to concoct a high level plan on how to best minimize my household’s collective tax bill. (This was a tip my financial advisor gave me; her advice was to try to pay no more than an average tax rate of 15%5).

Capital gains caused by the sale of non-registered assets7

Since the first three items above were already known, there was no decision to make; the tax owing on those was already clear8. The capital gains were the only variable — how much should I take versus my spouse? There was a bit of estimation involved in the actual amounts here (the actual gains would depend on the actual sale price), but it gave me a high level plan for 20259. Any additional income needed would be paid by capital gains realized from MY holdings since my income was forecast to be lower than that of my spouse10.

With the pre-work done, it boils down to making the required sell trade, waiting two days for the cash to settle, and then clicking the right buttons to get the cash out of my investment account and into my chequing account. Should be simple, but if you’ve never done it before, you need to make sure it’s all working as you expect.

Sell required assets in RRIF

Yes, you have to make sure that there’s cash available in your RRIF accounts (and remember, I have 4) BEFORE the monthly payment goes out. My provider would only be too happy to do this on my behalf, charging me their “telephone trading rates” for the trade — something like $30 plus $0.06 a share for XGRO. Compared with “free” if I do the work myself, that’s a pretty decent hourly rate…Do not forget that it takes two days for a trade to settle into cash. Since my provider does not pay interest on cash holdings, I’m highly motivated to keep any cash balance to a strict minimum. I hate not earning money on my money.

Adjust cash cushion up or down by comparing VPW suggestion to calculated salary

In my previous post I talked about moving “v” to the cash cushion and then simply taking 1/6th of it as salary. And that is exactly what I do. But practically, it’s impossible to do this maneuver in exactly the way I describe with my current provider (QTrade). Here are the specific reasons I can’t do what VPW asks me to do:

QTrade RRIF payments must be made to an external bank account. So right away, part of my salary cannot flow through an intermediary cash cushion account.

QTrade does not allow cash transfers between non-registered accounts on their online platform. This means that the asset sales in my non-registered account cannot be moved directly to the cash cushion accounts either11.

I have worked around the limitations imposed by my provider by either

moving money from my chequing account to my cash cushion if the VPW suggestion is higher than my salary (market is moving up)

moving money from the cash cushion to my chequing account if my salary is higher than the VPW suggestion (market is moving down)

I have set up smart-ish spreadsheets to break down all the various movements of money which I will share at some point once I figure out how to make them a bit more generic. I’ve also documented a step-by-step guide for my spouse which she uses as we sit together walking through the monthly tasks12 so that I have confidence she could execute on them if I became incapacitated. There is no substitute for handing over the controls to see where the gaps in knowledge — and documentation — are.

The future

Having witnessed what happens to savvy adults as they get older, I know deep down that this DIY strategy isn’t sustainable forever. There are too many moving parts, and too many opportunities to make mistakes.

At present, I don’t have a future plan mapped out. I have updated my “death binder“, but beyond this, nothing more. I will dedicate more research (and future posts) on that topic.

For your benefit I have not mentioned the USD variants I have of a few of these. This post is long enough as it is, and I presume that most readers don’t hold assets that are traded on US stock exchanges. ↩︎

My own RRIF and my spousal RRIF account for two, and my spouse has two as well. Total four. They are with the same provider. Spousal RRIFs are generated from spousal RRSPs, in case you were wondering. If you deal with more than one RRIF provider (I would NOT recommend that), you’ll also have to consider that. All this to say that I saw 4 distinct payments made to my joint chequing account on Friday last week, one for each of the 4 RRIFs. ↩︎

I keep saying “my RRIFs” for simplicity, but all 4 RRIFs (2 in my name, 2 in my spouse’s) are treated the same way. All four payments end up in our joint chequing account. ↩︎

Both my spouse and I have non-registered accounts. My spouse’s was funded via a spousal loan I set up years ago to achieve some degree of income splitting. ↩︎

After years of thinking of taxation in terms of what I paid on the LAST dollar I earned, this was admittedly a very different way of considering the problem. ↩︎

Most of my dividend income (via XGRO and AOA) is buried in my RRIF and TFSA to avoid any taxation of it ↩︎

Because I make a lot of use of HXS and HXT in my non-registered portfolio, I earn no dividend income; it’s all capital gains… ↩︎

If you’re not aware, RRIF payments are treated as no-special-treatment taxable income, reported on a T4-RIF form by CRA. ↩︎

Since I get paid monthly, I could always adapt if my assumptions were radically off. ↩︎

I could have also paid the extra from my TFSA holdings, but my advisor suggested that this is the LAST bucket to use in retirement. ↩︎