This is a monthly look at what’s in my retirement portfolio. The original post is here.

Portfolio Construction

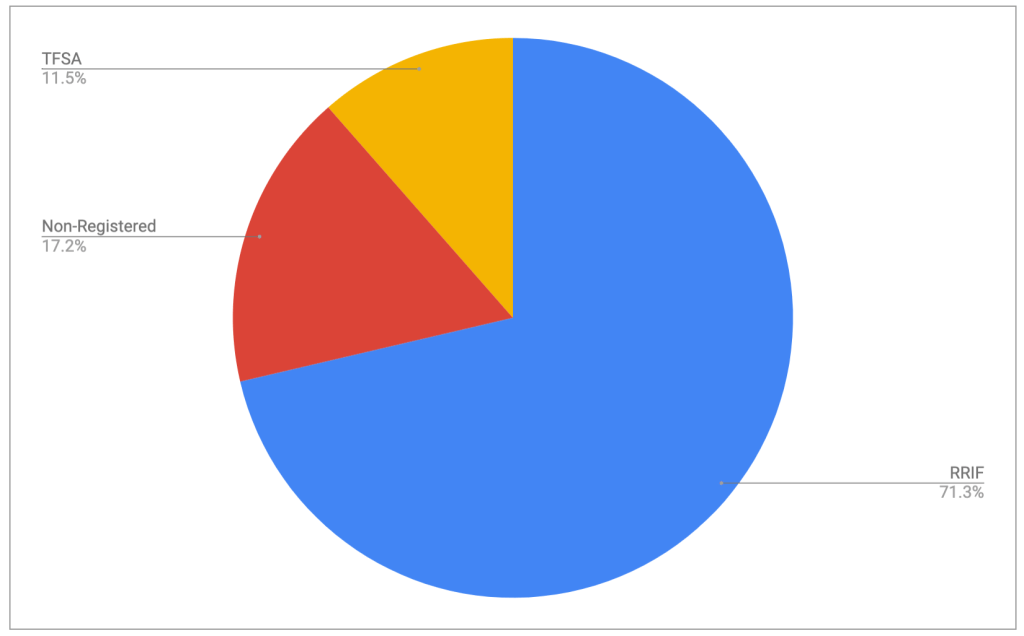

The retirement portfolio is spread across a bunch of accounts:

- 6 RRIF accounts (2 for me, 3 for my spouse, 1 for me at an alternative provider as a test)

- 2 TFSA accounts

- 4 non-registered accounts, (1 for me, 1 for my spouse, 2 joint)

The target for the overall portfolio is unchanged:

- 80% equity, spread across Canadian, US and global markets for maximum diversification

- 15% Bond funds, from a variety of Canadian, US and global markets

- 5% cash, held in savings-like ETFs.

You can read about my asset-allocation approach to investing over here.

The view post-payday

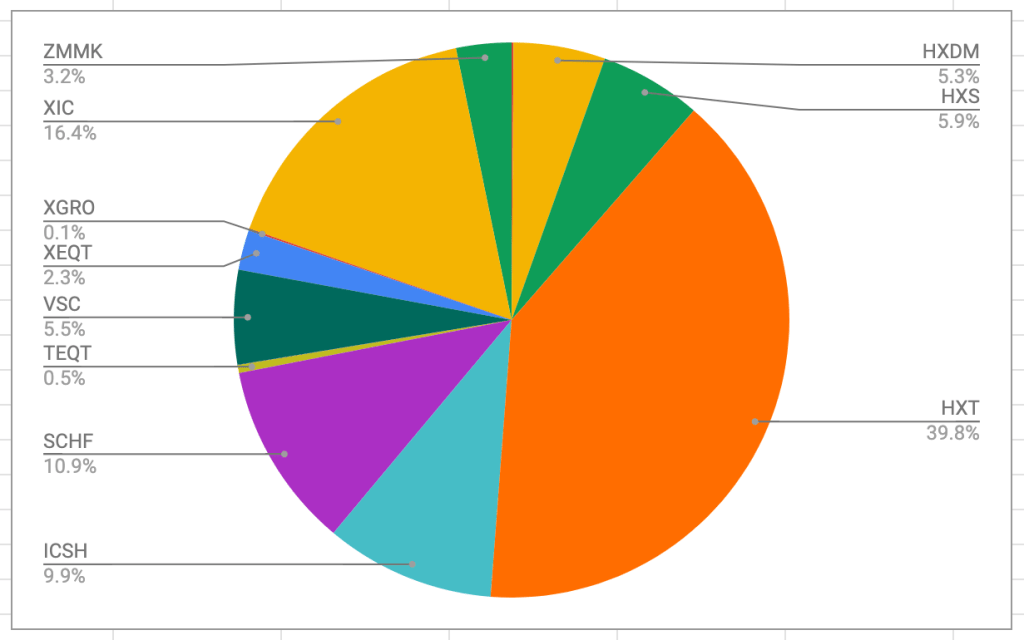

I pay myself monthly in retirement, so that’s a good trigger to update this post. On December 23, this is what it looks like:

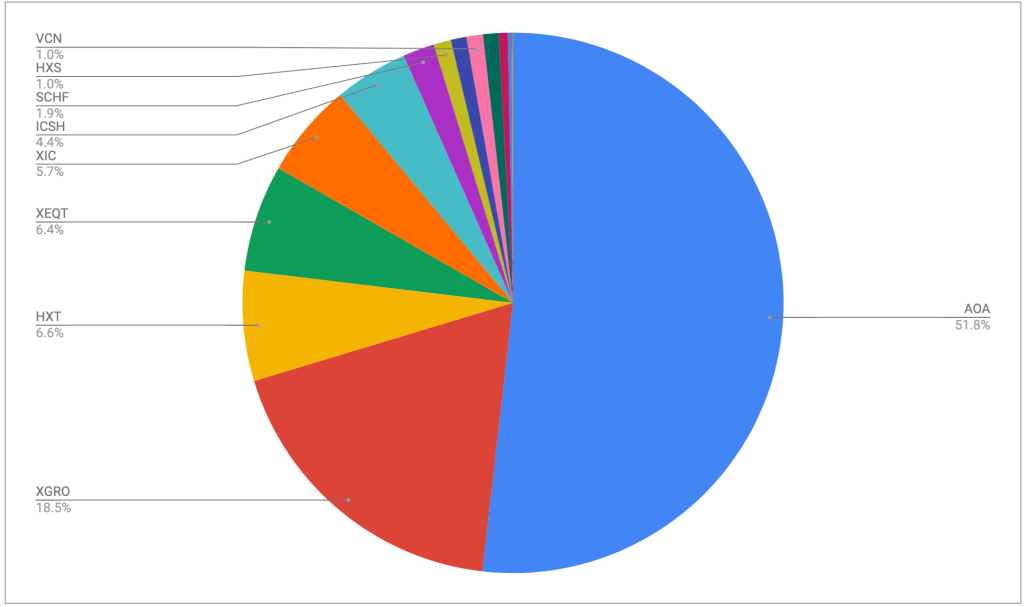

The portfolio is dominated by my ETF all-stars; anything not on that page is held in a non-registered account and won’t be fiddled with unless it’s part of my monthly decumulation. Otherwise I’ll rack up capital gains for no real benefit.

There aren’t really any notable changes this month — AOA’s contribution was down a bit this month, largely due to an unfavourable change in the USD/CAD exchange rate (down about 3% month over month, back down to a level not seen since around May this year). I recalculate the FX rate every month1 since I track my net worth in CAD so I always have an apples-to-apples comparison. I don’t stress too much about the FX rate as it tends to cut both ways. Sometimes it’s a lift to my numbers, sometimes not. In the end, I suppose it all evens out. I tracked my snapshot FX rates starting in February2, just for illustration:

Monthly USD/CAD rates on payday day

Plan for the next month

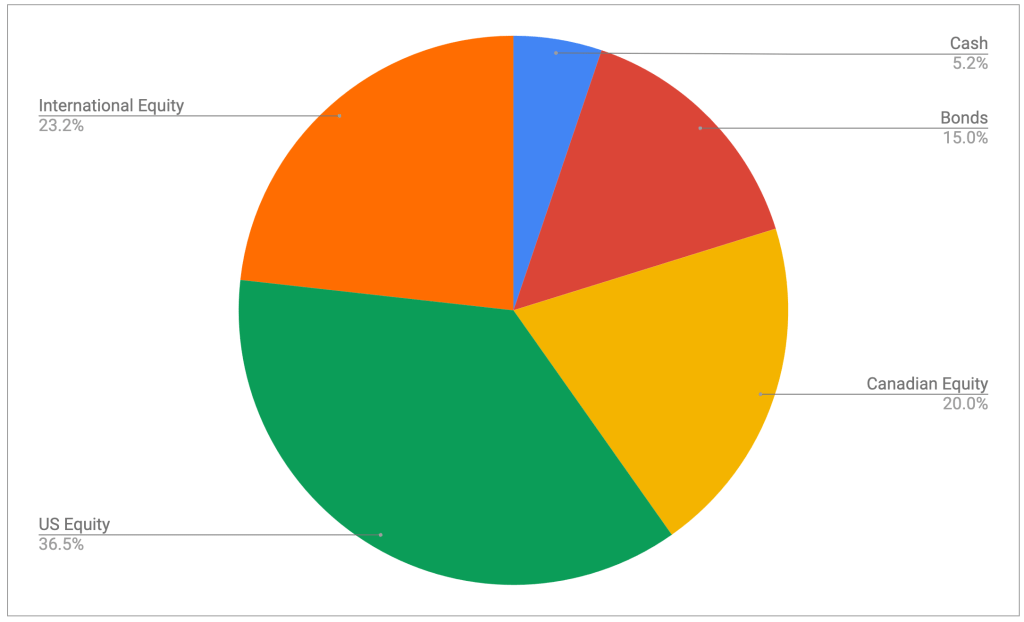

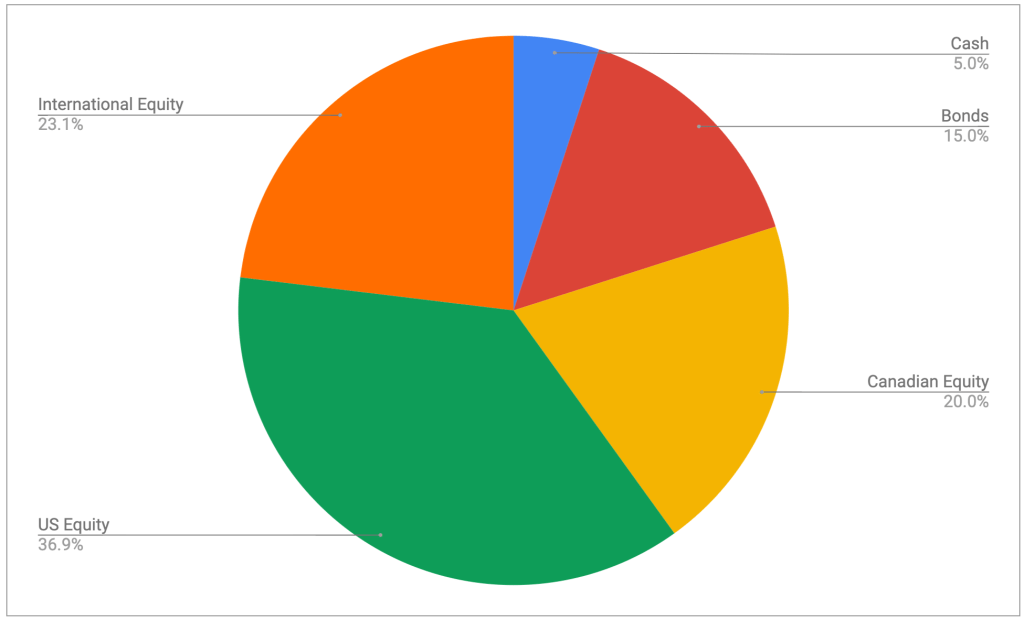

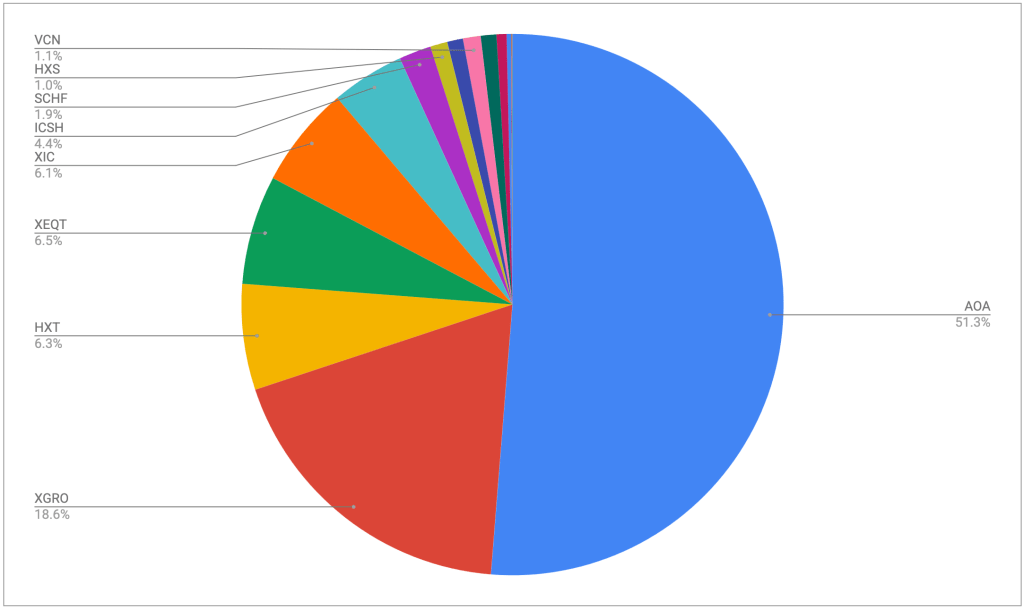

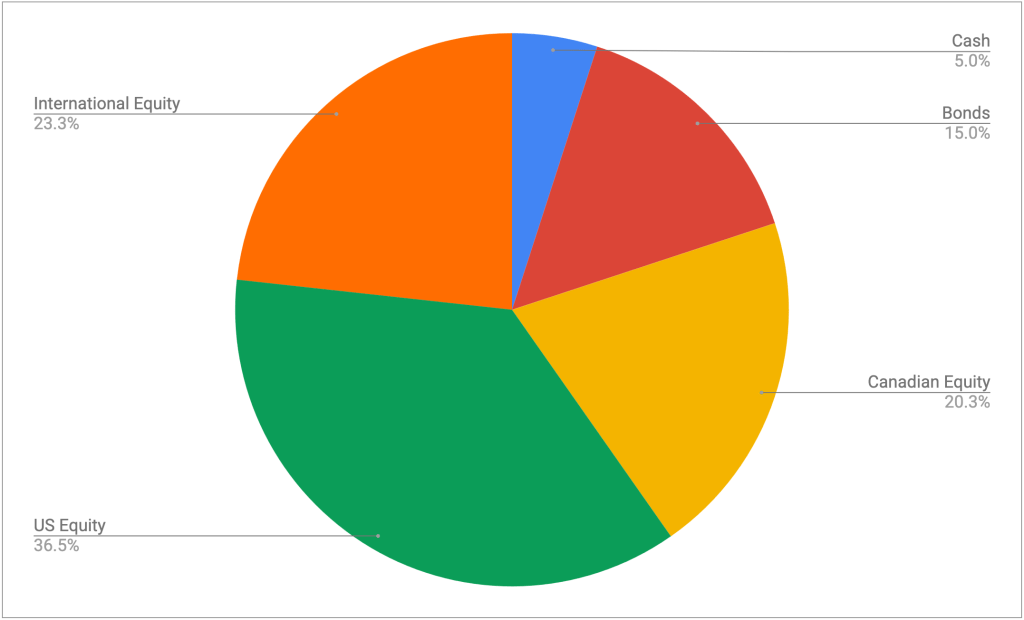

The asset-class split looks like this

It’s looking pretty close to the targets I have, which are unchanged:

- 5% cash or cash-like holdings like ICSH and ZMMK

- 15% bonds (almost all are buried in XGRO and AOA)

- 20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX)

- 36% US equity (dominated by ETFs that mirror the S&P 500)

- 24% International equity (mostly, but not exclusively, developed markets)

The end of the year will mean more distributions from my holdings; in my RRIF accounts they are set to DRIP since I only hold AOA/XGRO/ICSH in these accounts. The rest I redeploy to the asset classes that are short funds; typically this means investing in one of the *EQT funds since the bond complement of the portfolio frequently moves above the 15% target.

Overall

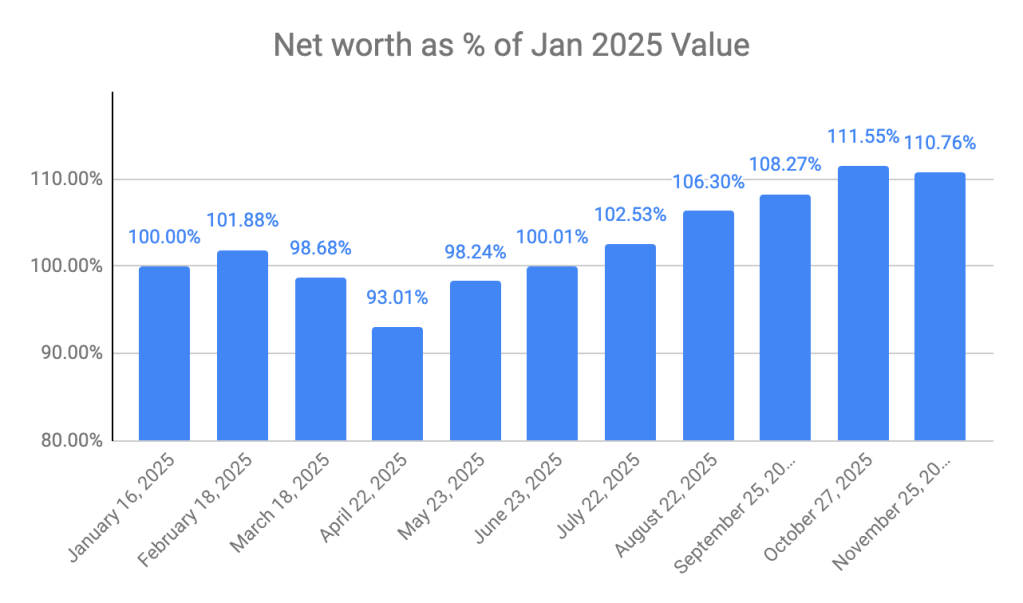

Net worth overall is down slightly month over month, but up a little over 10% from the start of the year. Hard to be unhappy about that.

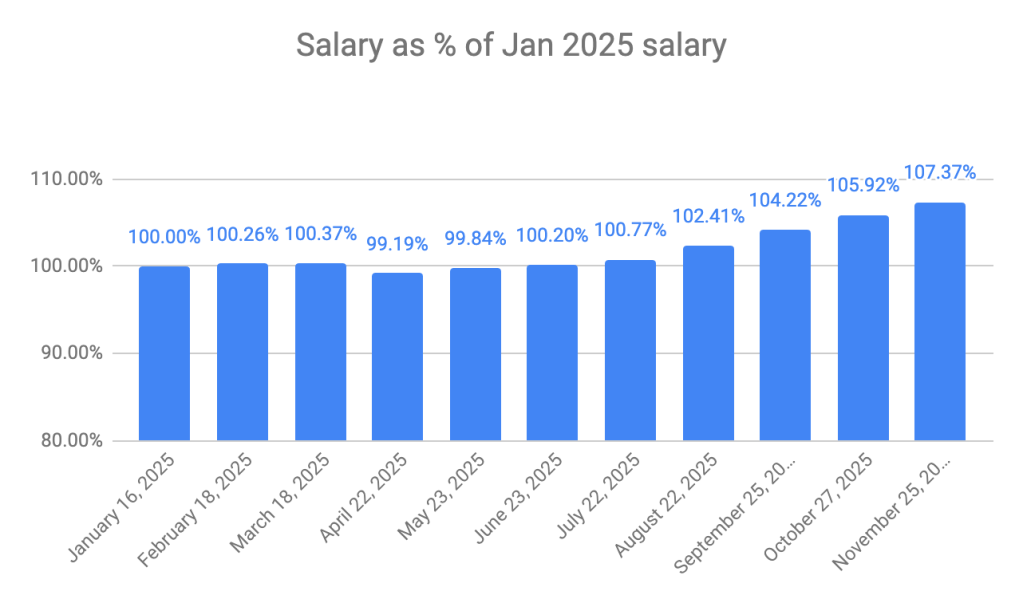

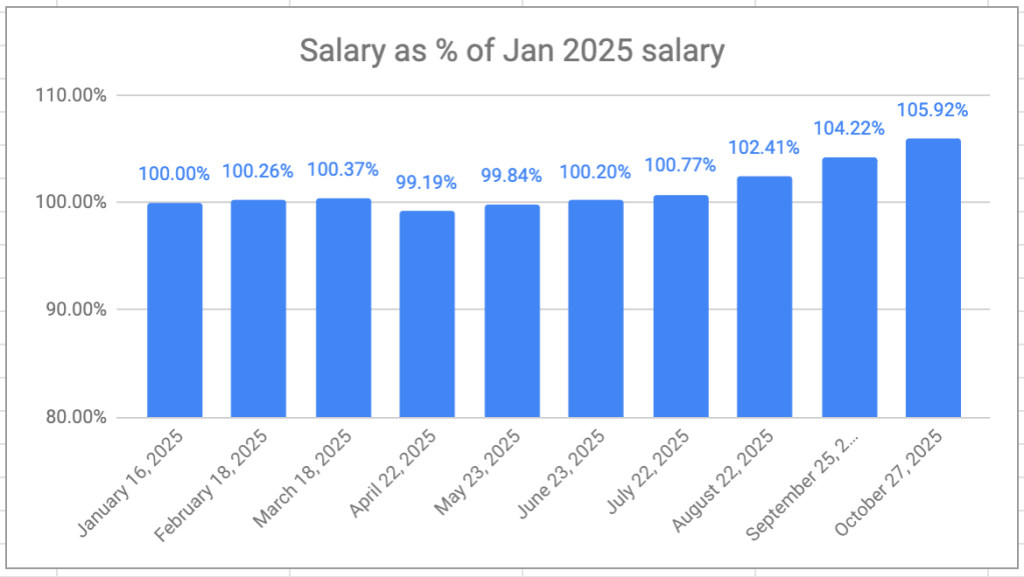

My VPW-calculated salary took a slight decline, breaking the 7 month growth streak. It ends the year a shade under 6% larger than my first paycheque. Not bad. I don’t recall many years where I got a 6% raise 😉

Next month will end my relationship with QTrade as I move the final 3 RRIF accounts to Questrade; I had thought December would be the final month, but as you’ll see in my next post, a (hopefully) small wrinkle has delayed this.

- Using =googlefinance(“USDCAD”) of course ↩︎

- February because I only thought to start tracking that a month in. January’s rate will be lost to the sands of time. Or I could add it back using the official FX rates, I suppose. ↩︎