As reported last week, the USA cut their prime rates while Canada did not. The latest rates are now reflected in the HISA and short-term bond table (Canada & US). No changes for at least 6 weeks at this rate. Most cash I hold in my retirement savings is invested in an ultra-short-term bond fund, namely ICSH (one of my ETF all-stars) so I can squeeze out a few more basis points on my cash holdings.

TD Cuts Trading fees on 100 ETFs

TD seems to be upping its game. Not only are they throwing free money around, but an observant reader (thanks, big brother 🙂 ) alerted me to a recent change. You can read all about it here, but the skinny is that they cut trading fees on a list of 100 ETFs. Paying trading fees of any kind seems to be a dying business model, so it’s nice to see TDDI join the free club, at least a little bit. Some of these ETFs are even worth holding; I’ll save you the trouble and show you which ones:

Name

Symbol

What it holds

Vanguard S&P 500 Index

VFV

Largest US Companies

SPDR S&P 500

SPY

Largest US Companies in USD

Vanguard 500 Index

VOO

Same as SPY

iShares Russell 2000

IWM

Small cap US Equity in USD

TD all-in-ones

TEQT, TGRO, TBAL, TCON

100% Equity, 90% Equity, 60% Equity, 30% Equity. Read more here and here.

Newly free-to-trade ETFs at TDDI that are moneyengineer.ca approved

All the above funds would be worthy of consideration since they adhere to my rules about being passively managed, low cost, and aligned with my asset-allocation strategy. The simplest purchases here would be one of the TD or Vanguard all-in-ones (new to all-in-ones? read about them here) best aligned with your risk profile. There’s a bunch of other ones that aren’t of interest to me — bitcoin, leveraged, actively managed, segment-based…nah, I’m good.

In a previous post, I took a look at the major fund companies’ all-in-one-funds with a focus on what passive indices each of them folllowed with regards to Canadian equity, US equity, International equity, and bonds. That assessment found that iShares and BMO were very similar, but TD and Vanguard looked very different.

But do different indices really make a difference in terms of what each of these companies hold when it comes to equities? That’s what we’re trying to find out. Let’s take a look at each of the categories in turn.

Canadian Equity

Let’s take a look at the top Canadian equity holdings of TEQT, XEQT, ZEQT and VEQT1:

Stock

TEQT %

XEQT %

ZEQT%

VEQT%

RBC

1.65

1.73

1.62

1.80

Shopify

1.55

1.69

1.62

1.49

TD

1.12

1.16

1.10

1.16

Enbridge

0.84

0.88

0.85

0.92

Brookfield

0.82

0.82

0.78

0.81

BMO

0.74

0.77

0.72

0.77

Agnico

0.66

0.69

0.68

0.63

Scotiabank

0.64

0.67

0.63

0.68

CIBC

0.60

0.63

0.60

0.63

CP KC

0.57

0.58

0.57

0.62

# held

292

215

215

156

Top 10 %

9.19

9.62

9.17

9.51

Top Canadian Equity Holdings for TEQT, XEQT, ZEQT, VEQT per ETF factsheets, October 2025

VEQT has fewer holdings than the others, and this indicates slightly more concentration/slightly less diversification than the other funds. TEQT is at the top of the heap when it comes to the number of companies held, with XEQT and ZEQT looking pretty similar. My take here is that the differences between TEQT/XEQT/ZEQT/VEQT are pretty slight when it comes to Canadian equity. The Canadian equity indices these funds track may be different, but the differences are pretty minor, and might simply be attributable to tracking errors; how often and when these funds rebalance their holdings may explain the differences shown here.

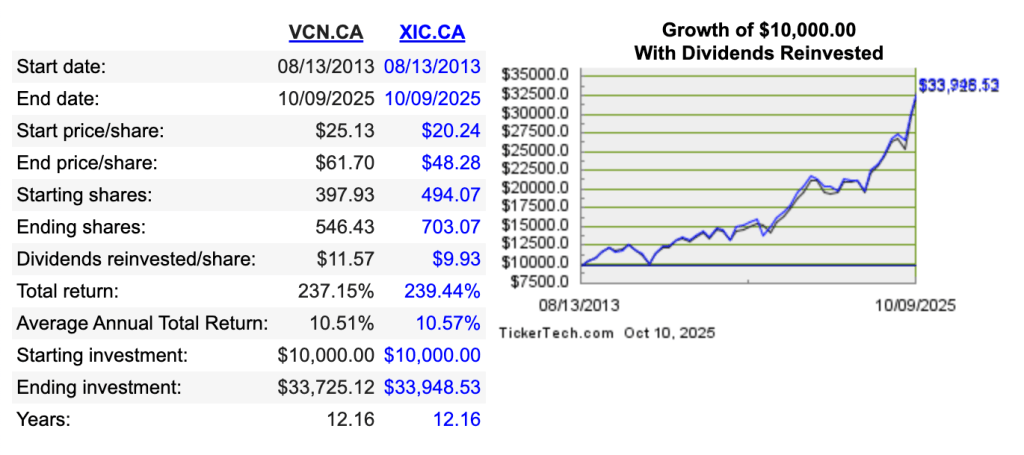

But just for fun, I looked at comparing VCN (which is underneath VEQT, and tracks the FTSE Canada all cap) to XIC (which is underneath XEQT, and tracks the S&P/TSX Capped Composite) and found this using https://www.dividendchannel.com/drip-returns-calculator/ (which is also listed in Tools I Use).

This indicates a tiny advantage to XIC aka the capped composite index, but there’s not a lot of daylight between these two returns!

On the Canadian Equity front, I declare the 4 funds EQUIVALENT!

US Equity

The US weighting is NOT the same for each of these funds, so making a one-to-one comparison is a bit tricky.

TEQT: 55% US

ZEQT: 50% US

XEQT, VEQT: 45% US

What I show in the table below is the percentage of the US portion held by the fund. So in other words if stock XYZ makes up 5% of the US holdings of TEQT and XEQT, it means that TEQT actually holds more of XYZ because 55 cents of every dollar of TEQT is invested in XYZ as compared to 45 cents for XEQT et al.

Stock

TEQT: TPU %

XEQT: XTOT %

ZEQT: ZSP/ZMID/ZSML%

VEQT: VUS%

NVIDIA

7.81

6.91

7.35

6.45

Microsoft

6.62

5.71

6.26

6.02

Apple

6.38

5.53

5.99

5.54

Amazon

3.73

3.24

3.45

3.49

Broadcom

2.75

2.38

2.51

2.23

Meta

2.74

2.33

2.51

2.56

Alphabet Cl A

2.43

2.07

2.26

1.97

Alphabet Cl C

2.13

1.67

1.82

1.59

Tesla

2.12

1.80

1.91

1.46

JP Morgan

1.46

1.24

1.36

1.29

Eli Lilly

1.25

1.00

1.09

1.00

Berkshire

1.15

1.33

1.47

1.43

# held

504

2494

1511

3524

Top 10 %

38.17

32.97

35.54

32.74

Top US Equity Holdings for TEQT, XEQT, ZEQT, VEQT per ETF factsheets, October 2025

What’s clear here is that TEQT is an outlier insofar as it only focuses on the largest US companies, with the other three funds including smaller companies. This also impacts how much money is found in the top 10 US holdings of TEQT, with 38% of holdings invested in names like NVIDIA, Microsoft, Apple et al.

This has proven beneficial of late since smaller US companies have not kept pace with the larger ones. Per spglobal.com, the 10 year performance as of Oct 13, 2025 of the three US market segments has been:

S&P SmallCap 600 = 7.65%

S&P MidCap 400 = 8.49%

S&P 500 = 12.75%

Meaning that any fund that holds smallcap and midcap US stocks has had their returns dragged down in the past 10 years.

So my conclusion for US Equities is that TEQT is the performance champion, but this comes with a less diversification than the alternatives: not only does TEQT focus on the highest-performing portion of the US equity market, it also puts more money overall into the US equity market. This has worked well for the last ten years, but it’s anybody’s guess as to whether this is a good idea for the future.

International Equity

The International2 weighting is NOT the same for each of these funds, so making a one-to-one comparison is a bit tricky.

TEQT: 20% International

VEQT: 25% International

ZEQT: 25% International

XEQT: 30% International

BMO gets the “lack of transparency” award from me for their complex structure. ZEQT holds ZEA which holds European stocks as well as IEFA, which is their USD fund holding the same things. It also holds ZEM which holds emerging markets stocks as well as EEM, which holds similar things in USD. Nowhere can you find a BMO/ZEQT consolidated view like what I’m showing below.

Like in the previous examples, what I show in the table below is the percentage of the International portion held by the fund.

Stock

TEQT: TPE %

XEQT: XEF/XEC %

ZEQT: ZEA/IEFA/ZEM/EEM%

VEQT: VIU/VEE%

Taiwan Semi

0

1.73

5.88

4.19

ASML

1.98

1.43

2.11

1.59

SAP

1.43

1.03

1.37

1.14

Nestle

1.30

0.93

1.24

0.96

Roche

1.24

0.87

1.12

0.95

Novartis

1.24

0.90

1.17

0.98

AstraZeneca

1.24

0.93

1.26

0.94

HSBC

1.15

0.83

1.22

1.02

Shell

1.11

0.80

1.09

0.87

Toyota

1.06

0.70

0.97

0.85

Siemens

1.02

0.77

1.08

0.82

Tencent

0

0.80

2.75

2.10

Samsung

0

0.37

2.03

1.16

Alibaba

0

0.40

1.87

1.59

# held

893

5626

3864

3524

Top 10 %

12.77

10.25

20.89

15.68

Top International Equity Holdings for TEQT, XEQT, ZEQT3, VEQT per ETF factsheets, October 2025

Here you see some pretty significant differences. BMO and Vanguard (especially BMO’s ZEQT) have a much heavier emphasis on “emerging” markets than XEQT does; TD’s TEQT has NO exposure to emerging markets at all.

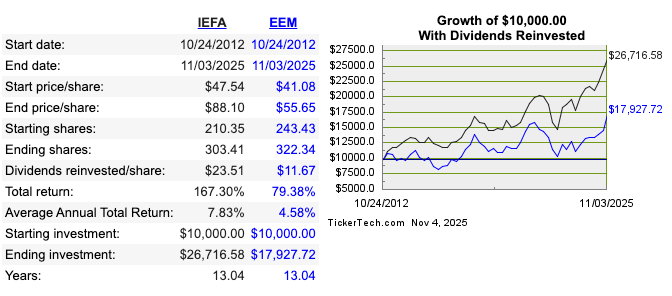

That’s an interesting strategic choice being made here. Let’s compare emerging market performance to mature international markets. We cand do that by looking at IEFA (mature markets) versus EEM (emerging markets)4:

Emerging markets have been a serious lag to global performance, so perhaps TD is on to something here. I played with this chart quite a bit and it’s only very lately (last 2 years or so) that emerging markets have outperformed the established ones. Long term trend? ZEQT certainly hopes so.

So on the international front, you have choices

TEQT only focuses on mature markets

XEQT allows some (not much) exposure to emerging markets

ZEQT and VEQT make much bigger bets on emerging markets

Which is the correct call? TEQT historically has made the right choice, but as the old adage goes “past performance does not guarantee future results” (or something like that).

I’m using the all-equity versions of these to make the comparison more apples-to-apples. VEQT has a larger Canadian percentage (30%) than the other 3 (25%), so I muliplied VEQT’s holdings by 25/30 to make the comparison meaningful. ↩︎

In this analysis, I’m not making a distinction between “mature” and “emerging” markets. Some of the funds do. In all cases, “International” means “no US, no Canada”. ↩︎

I’ve used QTrade for over a decade as the (until recently) exclusive provider of all my retirement savings. They do some things really well, but in other areas it’s clear they are falling behind.

I hang out a bit on Reddit1 to see what people are talking about. Often times, the post reads something like

“I am new to investing, I have $x to invest, who should I use ?”.

The crux of every 5th question posted to r/PersonalFinanceCanada

Personally, I find this kind of question a bit odd. “Investing” is a noble pursuit but it’s a term that means a lot of things to a lot of people. For me, “investing” is reserved for retirement savings since the timelines are long and I don’t need immediate access to the funds therein. A lot of people who ask this question want very near term access to the money, and to me that’s not investing. It’s saving. Timeline matters. The answer I’d give to a saver2 is a lot different than the answer I’d give to an investor.

I suppose the amount of money involved may influence the decision of platform provider (especially if there are freebies associated with having a balance above a certain amount, a common-enough practice), but it’s not the first thing I’d have in mind. Here are the main things I think about when it comes to choosing a financial provider, either for the first time, or if you’re thinking about making a change.

Does the provider have the account types you want?

Any provider I use has to offer Investment accounts, RESP, TFSA, RRIFs and spousal RRIFs. USD options for Investment accounts and RRIFs would be useful to me as well. Your own circumstances will offer up a different list. But don’t dismiss the RRIF if you’re nearing retirement. You may want one sooner than you think!

Does the provider have the products you want?

My needs here are really simple. I need access to trade a handful of ETFs on the US and Canadian markets, and I need a way to get a good interest rate on cash holdings. My assumption is that every major provider has a way to accomplish this. I don’t need access to bond markets3, options trading, fractional trading, margin trading or crypto. You might.

What fees that matter to you are charged by the provider?

The list of fees for any provider can get pretty long, but I only consider the things that impact me in my normal usage of the platform. The things I look for and expect are:

They don’t charge anything for “account maintenance”

The don’t charge fees for trading the ETFs I care about4

They need to offer a way to access daily interest rates in the neighborhood of the Bank of Canada overnight rates (some do this by paying good rates on any cash lying around your accounts, some do this by offering access to purchase HISAs, and as a last resort, there are ETFs that buy HISAs, too5)

They need a “much more generous than the bank”6 way of doing forex7

I’ve used QTrade8 as my main provider for the last 15 years or so. They offer the things I need. But for the first time, I’m seriously considering making a switch to Wealthsimple9. I’m test driving them now with part of my retirement portfolio, but I’ve found at least one show-stopper that make them unsuitable for me — they don’t offer spousal RRIFs10 in their self-directed product offering!

Switching providers can be quite onerous, so it’s not something I take lightly, especially since my holdings are paying my monthly salary! The DIY market is getting more competitive, so it can pay to take a look around. What do you like/dislike about your current provider? Drop me a line at comments@moneyengineer.ca.

Put your money in the highest interest rate savings account you can find, or buy a GIC. ↩︎

Beyond bond ETFs. I don’t need to own individual bonds. ↩︎

Had I written this phrase 5 years ago, I would have said “low fees”. However, in today’s competitive landscape, many brokers charge nothing to buy and/or sell ETFs. If yours does, maybe it’s time to take a look around. ↩︎

Norbert’s gambit would apply here, although it’s somewhat cumbersome. I’ll cover forex in some future post. ↩︎

But I’m also somewhat familiar with BMO Investorline, Interactive Brokers and Wealthsimple. ↩︎

Free ETF trading, good interest rates for cash holdings, just-launched zero fee FX transactions for amounts over $100k, and their currently running promo are all rather attractive features. ↩︎

And, as I write this, I get a friendly email from Wealthsimple support confirming this, with a promise to let the development team know about it. ↩︎