Right after the final, final deadline of Wealthsimple’s last free money offer, it appears that Wealthsimple is now offering spousal RRIFs as an account type for the DIY investor (they’ve had them for quite a while in their robo-advisor accounts).

This had always struck me as silly, especially since they have offered spousal RRSPs for a while now.

With this development, Wealthsimple is nearly a viable option to host all of my retirement funds1. My needs are pretty simple:

support for all the account types I need (RRIF/Spousal RRIF, TFSA, joint non-registered, individual non-registered)

zero cost ETF buy/sell

support for Norbert’s Gambit (which implies support for USD accounts, naturally)

Norbert’s Gambit is planned in early 2026 for Wealthsimple, per the very limited info found here.

So, if you’ve been on the fence about Wealthsimple, here’s one more reason to consider them. Once Questrade’s free money gravy train ends for me in March 2027, they become a personal serious contender, especially if they are willing to throw free money my way, which, historically, has certainly been a recurring theme. On that note, if any reader wants to give them a whirl, I have referral codes, just shoot me a note at comments@moneyengineer.ca; if you act quickly2, there might be some free Apple gear in it for you too.

QTrade and Questrade both offer all three. There may be others. ↩︎

DIY investing also means DIY decumulation. In 2026, I’ll be paying myself from my various RRIFs as well as from non-registered funds. I’ll refer to the letters in the diagram below so you can follow along1:

A: Calculate Net Worth over all retirement accounts

“Retirement accounts” include 3 non registered accounts, 2 TFSAs and 5 RRIF accounts. All of these are at Questrade except for one RRIF account held at Wealthsimple. My net worth calculation ignores my day-to-day spending accounts, and any other assets (my house, for example). In 2026 I could look up this number using Passiv, but I’m not 100% clear on what the fate of my Passiv account will be once Questrade cuts ties with them (March 2026). I still have a spreadsheet with lots of details and pretty graphs based on my multi-asset tracker.

B: Use VPW Methodology to Calculate Monthly “Suggestion”

VPW stands for “Variable Percentage Withdrawal” and it’s the playbook I use to guide my monthly withdrawals from my retirement accounts. I talk a bit about it here. The suggestion is generated by a VPW spreadsheet, but the inputs are pretty simple:

future pension amounts, and age you’ll be when you take them3

asset allocation breakdown (%stocks versus %bonds)

This “suggestion” represents the maximum value of the assets I am advised to sell this month. You could take more or you could take less. It’s merely a suggestion. For me, I take the suggestion at face value and sell the assets needed to meet the value of the “suggestion”.

C: Calculate the Salary

The “Suggestion” in step B is NOT your salary. The VPW methodology enforces one more step to calculate that. The VPW methodology requires the use of a “cash cushion”, which has the effect of making sure you don’t need to make drastic month-to-month changes in your salary, either upward or downward. The cash cushion is roughly 5x the “suggestion”4 and your salary is 1/6th of “suggestion” plus “cash cushion”. The “salary” represents the amount that will eventually turn up in your chequing account.

To make things easier to track, my “cash cushion” is a totally separate non-registered joint account that holds one of four things: Canadian dollars, US dollars, ZMMK or ICSH. I keep a little cash floating around in this account to avoid having to do monthly trades. It just makes tax reporting and ACB tracking a bit simpler, at a small loss of interest income. Also, Questrade doesn’t support fractional shares of either ZMMK or ICSH, and since they routinely trade at roughly $50/share, mathematically, I’ll always have $25 CAD and $25 USD on average 🙂

D/D’: Compare the Suggestion to the Salary and act accordingly

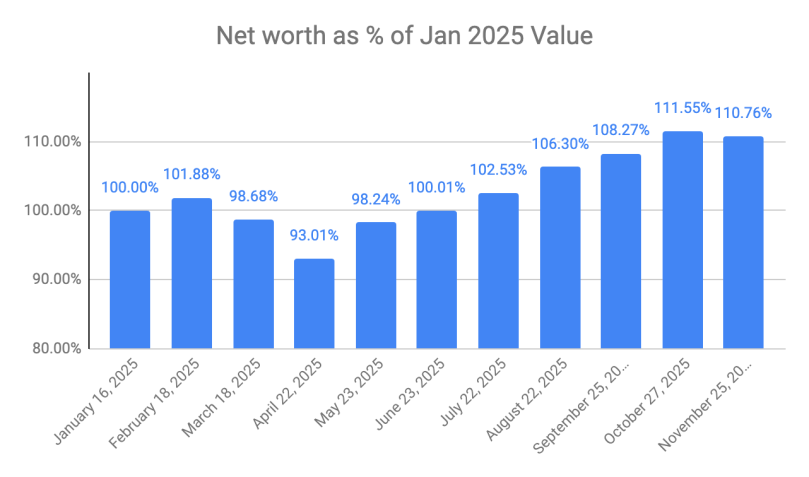

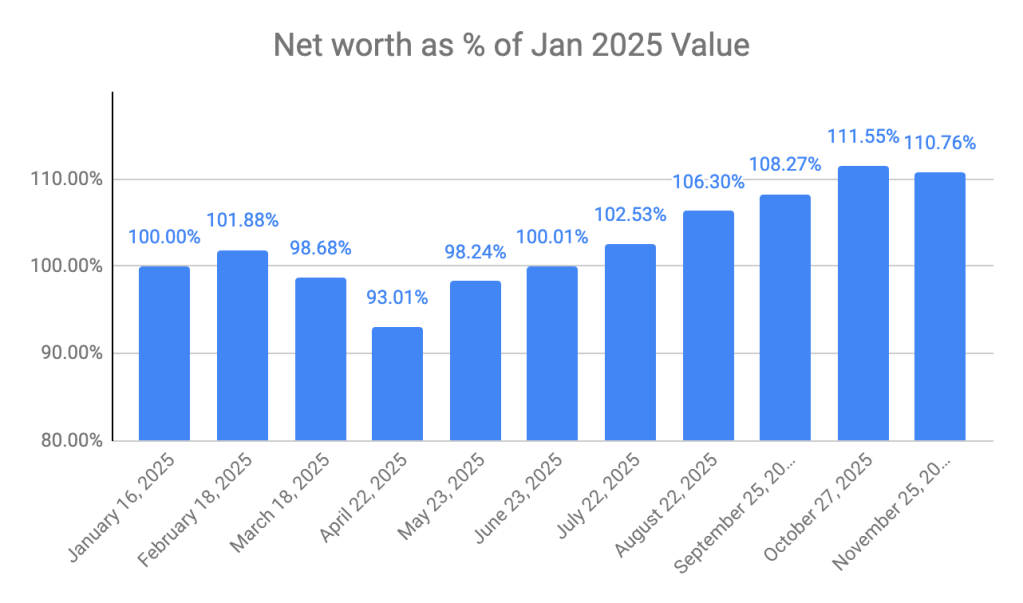

Since the cash cushion is effectively a 5-month moving average Salary, the Suggestion could be more than or less than the Salary. If my net worth is down (or up) month over month, then it follows that the Suggestion will also be down (or up) month over month. My Salary may or may not be down (or up), depending on how long the downturn has lasted. Just to give you a sense of how the cash cushion smooths out the market gyrations, you can see the comparision of net worth versus salary below. (Taken from my most recent monthly “What’s in my Retirement Portfolio” update.) The net worth moves quite a bit month-to-month (generally upward, which is nice), but my salary is much smoother (but also generally upward).

Anyway, what all this means is that I’m either going to move some of the Suggestion money into the cash cushion (because my Salary is less than the Suggestion), or I’m going to pay myself from the cash cushion because my Salary is higher then the Suggestion5. It’s one or the other; as yet, I haven’t had the Salary be equal to the Suggestion, but it is mathematically possible, of course.

E/E’: Make sure the 4 Questrade RRIFs have cash to cover the monthly payment

At the end of 2025, I’m expecting some sort of communication6 from Questrade as to what my minimum monthly7 RRIF withdrawal needs to be for 2026 for each of the four RRIF accounts in my household8. This is a standard “feature” of anyone holding a RRIF — your provider makes a calculation based on the value of your RRIF on the last day of the year and your age (or your spouse’s age) at the end of the year. That’s RRIF minimum — the minimum amount you’re obligated to take. This coming year, I’ll stick with RRIF minimum again to avoid having to deal with spousal attribution rules.

So for 2026, I will know exactly how much cash I will need every month in every Questrade RRIF account. And since I’ve done such a good job in simplifying my RRIFs9 (pats back) I can also calculate exactly how many shares of XGRO need to be sold in each RRIF account every month, in real time10.

So generally, this step involves placing 4 sell orders to put cash in the account.

The E’ step — moving cash from the RRIF to the chequing account — I’m expecting to be automatic, but since I haven’t had to do this with Questrade before, I’m not certain.

F/F’: Generate cash equal to RRIF minimum in the Wealthsimple account and move it to the chequing account

Like with Questrade, I’m expecting Wealthsimple to communicate my RRIF minimum. From what I can see from their website, it appears that they actually make it really obvious.

The same good work I did with my Questrade accounts is even better in my Wealthsimple RRIF account since I hold no USD at Wealthsimple. So here, and thanks to fractional shares, 100% of my RRIF is invested in XGRO, with no additional cash.

Their help article makes it sound like both F and F’ are under my control, which is fine. I’ll just do this step at the same time I do the Questrade step. Maybe I only have to do F’ once and pay out in “Installments”? Not sure.

G/G’: Use the non-registered account(s) to generate cash equal to Suggestion minus all the monthly RRIF payments

I already know my five RRIF minimum payments will fall well short of the VPW “Suggestion”, so every month I have to sell assets from the non-registered accounts to make up the shortfall. This cash will either go 100% to my chequing account or some of it may be diverted to the cash cushion.

Normally this comes from my, not my spouse’s, non-registered account. Since my spouse is still working, I leave hers alone to avoid generating capital gains. Unfortunately, my non-registered accounts are a bit of a dog’s breakfast, and although I’ve made efforts to use spreadsheet formulas to make automated suggestions11, it’s proving a bit more difficult.

In the end, this is again a sale of one or more assets. For step G’, I can then immediately use Questrade’s “Withdraw Money” to move the cash into my chequing account, or “Move Money” to move cash into the Cash Cushion account.

Conclusion

And that, my friends, are the steps I take monthly in retirement. I try to perform these steps in the dying days of every month while allowing enough time for trades to settle to ensure cash is well and truly in hand before I move it to my chequing account.

In my household, a very large portion of this process gets spit out as a step-by-step “do this, do that” set of instructions I’ve built into a macro-enabled spreadsheet. The trades required for Step G are still decided on the fly, manually. Of couse, given that Questrade has APIs, I could conceivably make automatic trades based on the work I’ve done, but I’m not sure I want to take that step. Retirement project?

I don’t really know if any of my readers find this particular articl useful, exasperating or confusing. But for me, it’s useful to write down how it works! ↩︎

For me, CPP, OAS and the OAS supplement. The current plan is to defer CPP/OAS until age 70 to maximize my inflation-indexed income. ↩︎

which, in my case, since I withdraw monthly, is about 5x my salary ↩︎

I’ve run this algorithm ten times so far this year: 3 times I had to pay myself out of the cash cushion and 7 times I added to the cash cushion. That’s the general upward trajectory of this year’s market in action ↩︎

My last provider, I actually called them to check. I had of course calculated it myself (and they were very close) but my numbers don’t matter to the CRA. I’m hoping Questrade makes it a bit more obvious, but I’m pessimistic. ↩︎

I had set it up as monthly. I could’ve chosen quarterly or annually. I like monthly. ↩︎

My RRIF accounts hold one of five assets: Canadian and US dollars (because I can’t buy fractional shares), ICSH, AOA, or XGRO. ICSH is held in RRIFs to keep me at 5% cash in my retirement overall, and I routinely convert (quarterly) AOA into XGRO using Norbert’s Gambit. ↩︎

And yes, I have a macro-based spreadsheet that tells you exactly how many shares to sell at that moment based on share price and current cash in the account. ↩︎

The most appropriate thing to sell in any given month is an asset for which I’ve become overweight per my multi-asset tracker. But when you hold all-in-ones in the portfolio, it’s a bit trickier to work that out. I just need to set aside some time to come up with a spreadsheet-based solution. I would much prefer this decision to be made algorithmically. ↩︎

You can read about my asset-allocation approach to investing over here.

The view post-payday

I pay myself monthly in retirement, so that’s a good trigger to update this post. On November 25th, this is what it looks like:

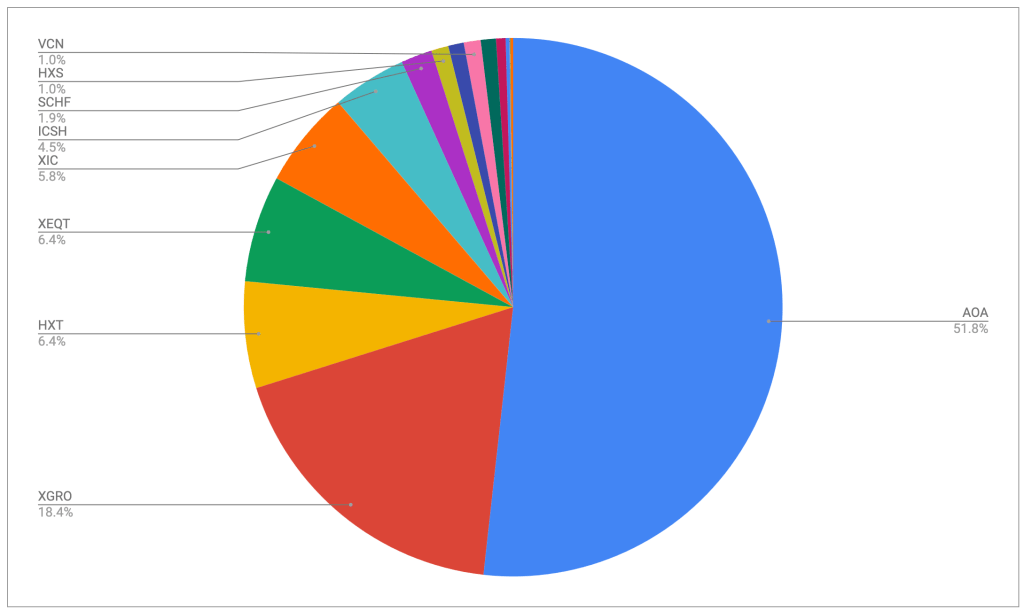

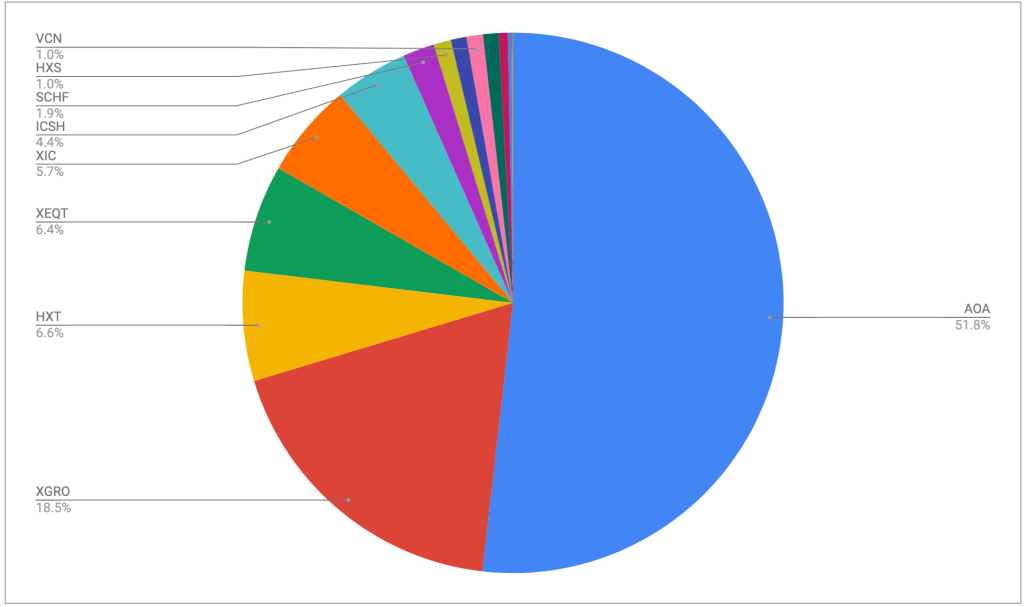

ETF Breakdown of retirement investments, November 2025

The portfolio is dominated by my ETF all-stars; anything not on that page is held in a non-registered account and won’t be fiddled with unless it’s part of my monthly decumulation. Otherwise I’ll rack up capital gains for no real benefit.

No notable changes this month; HXT is down slightly because that’s the fund I sold in my non-registered account this month to help pay the bills. I’ve sold quite a few shares of this fund this year and I’m seeing the capital gains mounting, but it’s around where I expected to be. I try to keep taxes owing reasonable; nonetheless I’m guessing I will certainly be moving to quarterly instalments in FY 2026; that’s the downside of having no withholding tax of any kind this year.

Plan for the next month

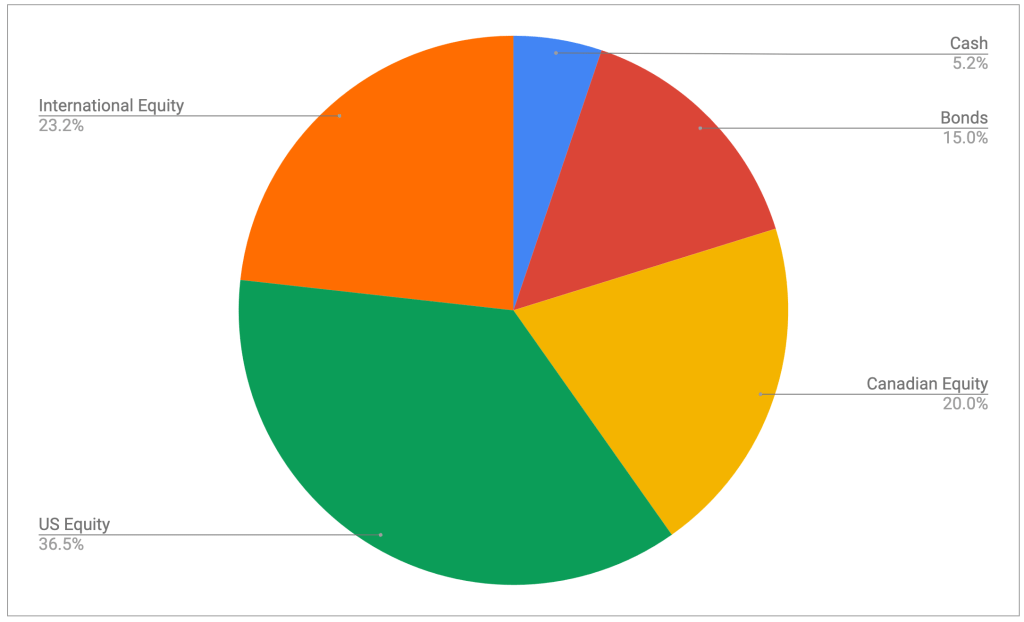

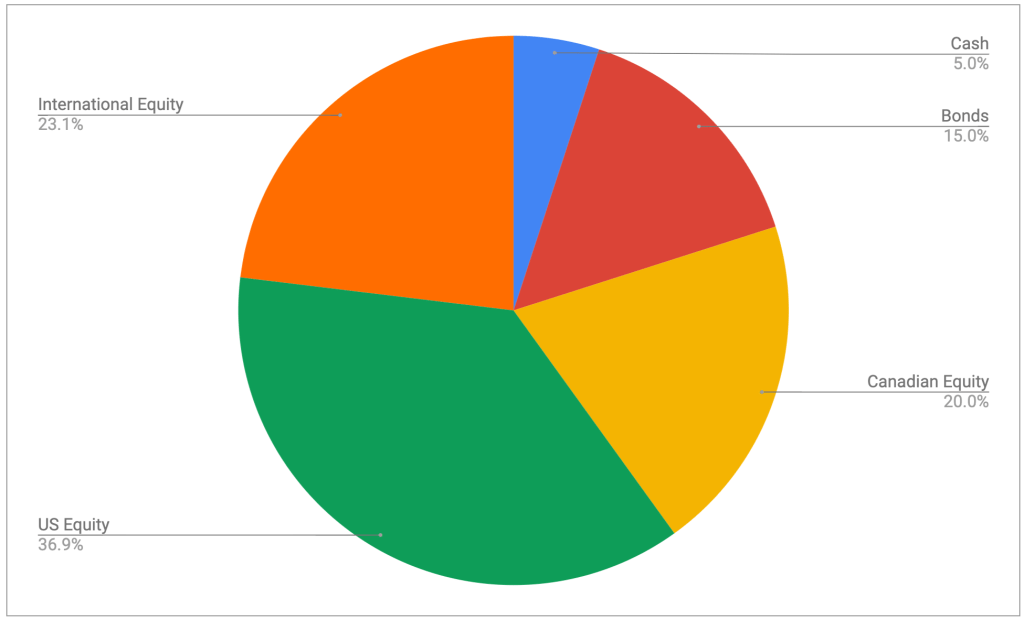

The asset-class split looks like this

It’s looking pretty close to the targets I have, which are unchanged:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds (almost all are buried in XGRO and AOA)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX)

36% US equity (dominated by ETFs that mirror the S&P 500)

24% International equity (mostly, but not exclusively, developed markets)

All looks to be in order from an asset allocation perspective, no need to do anything here. Cash is slightly elevated as a result of the pending closure of the three remaining QTrade accounts and will drift back to the normal 5% over the coming few weeks, I expect.

Overall

Net worth overall stopped its 6 month winning streak and I’m down slightly month over month. But I will reiterate: my net worth is still growing even though I’m taking a living wage every month. You might think that “decumulation” means “a steady reduction in net worth” but it needn’t be the case. And, in my particular case, my retirement income will include no pensions, so it’s probably a good thing that it keeps increasing overall.

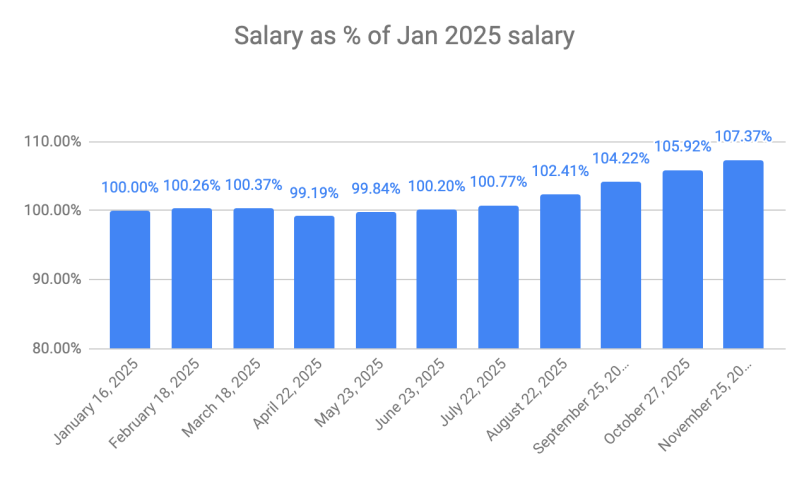

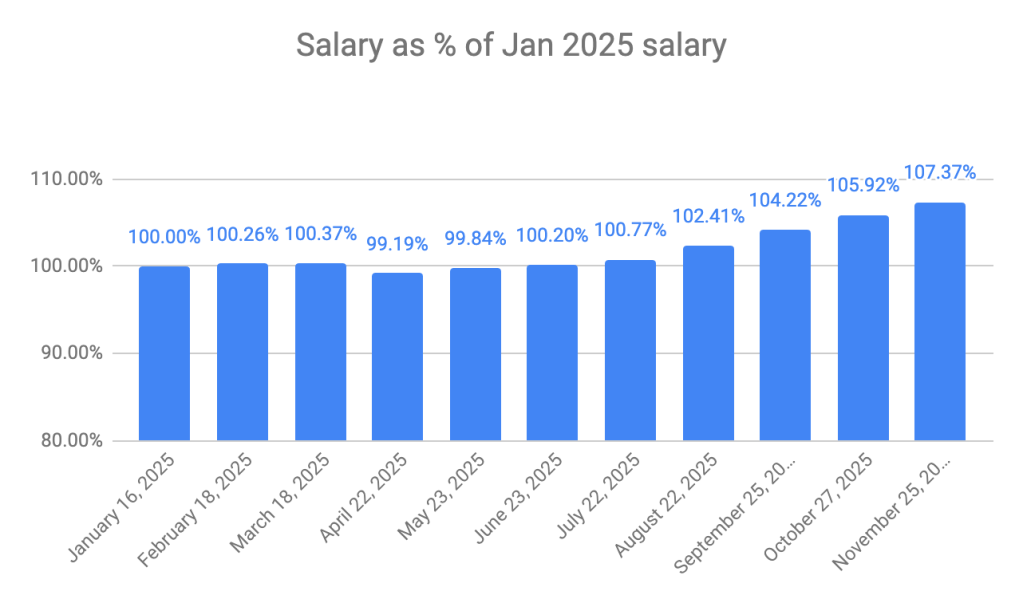

My VPW-calculated salary continues to grow for the 7th straight month in spite of the step back this month in my net worth. That’s a feature of the “cash cushion” that is integral to the VPW withdrawal. It serves as a shock absorber to the monthly ups and downs of the stock market.

Next month will end my relationship with QTrade as I move the final 3 RRIF accounts to Questrade2.

My QTrade one is no more, transferred to Wealthsimple to take advantage of their Summer promotion. ↩︎

I had hoped to move these to Wealthsimple and generate more free money, but alas, they still don’t support self-directed spousal RRIFs, which is very odd indeed. ↩︎

You can read about my asset-allocation approach to investing over here.

The view post-payday

I pay myself monthly in retirement, so that’s a good trigger to update this post. On October 27th, this is what it looks like:

The portfolio is dominated by my ETF all-stars; anything not on that page is held in a non-registered account and won’t be fiddled with unless it’s part of my monthly decumulation. Otherwise I’ll rack up capital gains for no real benefit.

No massive changes this month; the one you might notice is a slight shift from AOA to XGRO. I move some of my USD holdings into CAD every quarter, and last month was when I did it. The majority of my spending is in CAD, so I use Norbert’s Gambit to move funds around.

Plan for the next month

The asset-class split looks like this

It’s looking pretty close to the targets I have, which are unchanged:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds (almost all are buried in XGRO and AOA)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX 60)

36% US equity (dominated by ETFs that mirror the S&P 500, with a small sprinkling of Russell 2000)

24% International equity (mostly, but not exclusively, developed markets)

All looks to be in order from an asset allocation perspective, no need to do anything here.

Overall

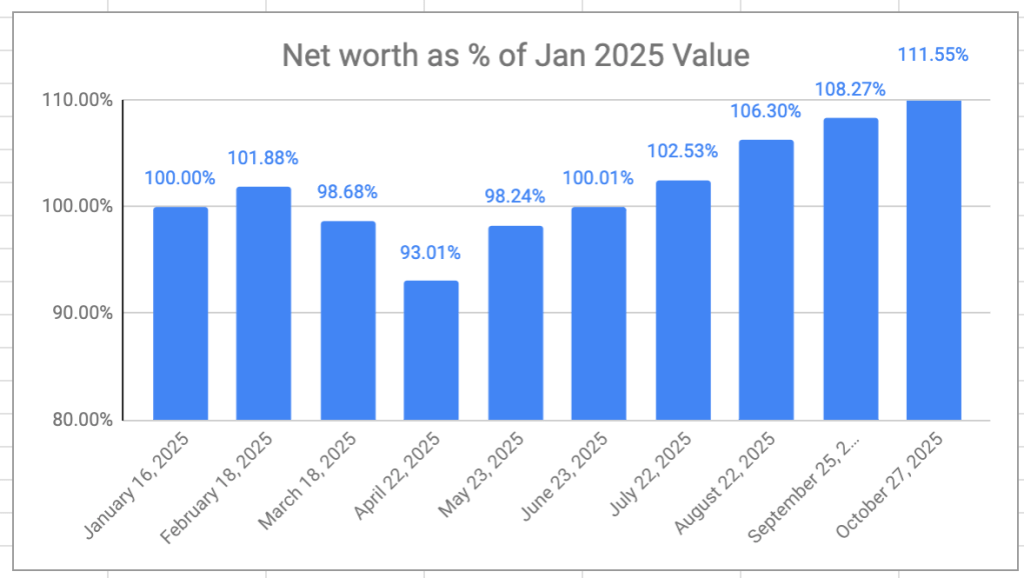

The retirement savings had a great month, again — a 6-month growth streak at this point. Overall, I’m now 11.5% ahead of where I started even though I’ve been drawing a monthly salary since the beginning of the year. I don’t really expect the winning streak to continue, but VPW allows me to take some benefit from the frothy stock markets at moment.

Net Worth as a percentage of starting point

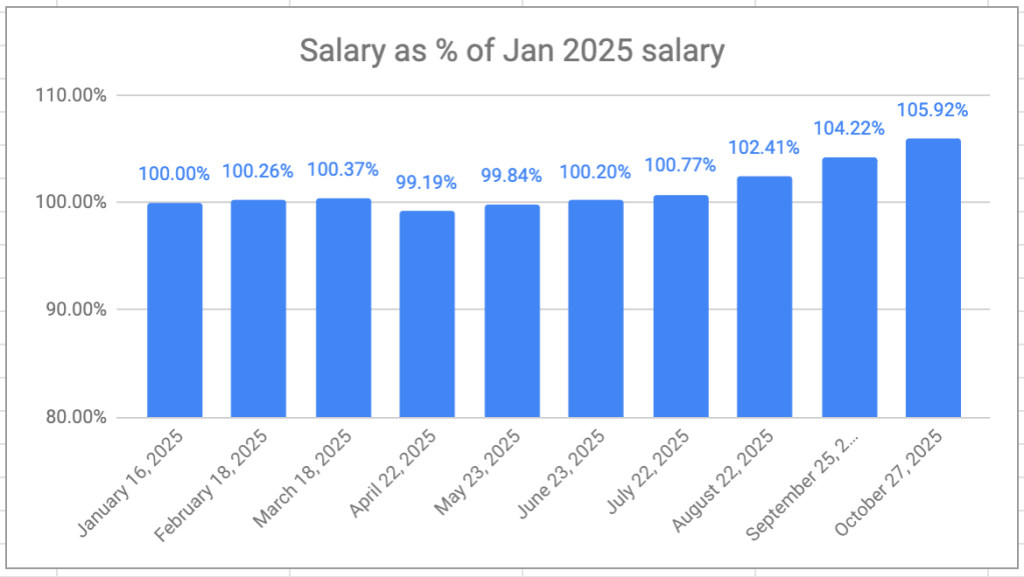

My VPW-calculated salary has hit a new high this year, 5.92% higher than my first draw in January. The monthly salary is also on a 6-month growth streak.

Monthly Salary as a Percentage of Jan 2025 salary

The months ahead will see the final “goodbye” to QTrade1 as the last of my RRIF investments will move to (mostly) Questrade2.

I didn’t have a great deal of issue with QTrade as a provider, but their support (lack thereof) was beginning to become irritating. ↩︎

My own QTrade RRIF will join the RRIF holdings I already have with Wealthsimple. They remain a potential backup provider of my retirement savings. I would have moved more to take advantage of their cashback promotion, but they still, inexplicably, do not support self-directed spousal RRIF accounts. ↩︎

Wealthsimple is a broker who holds some of my retirement assets1. They had a “For Nerds Only” (recording here) event on October 22 where they announced a bunch of new features. The most exciting development for me was the pending availability of Norbert’s Gambit. Here’s my take.

Of no personal interest to me as I don’t trade them. There are an increasing number of ETF products that use “Covered Call” strategies in an effort to eke some (or more) yield out of held equities, but I don’t bother with products like that2. I like my investments simple.

I lump these two together since I have the same amount of interest in both of these developments: none. Although people have made huge profits on gold and crypto, I’d rather make money off of companies that make things or provide services.

An interesting product that allows you to buy into the entire index3 (TSX all-cap4 or S&P 5005) and hold individual stocks. The main benefit of this is automated tax-loss harvesting which should reduce your tax bill in a non-registered account. The idea is logical, but it will come down to how well it is executed — how closely will Direct Indexing actually track the underlying index, and how much tax savings can be realized? The benefit will have to be more than the 0.5% MER being charged for investing in the index this way. Of possible interest in a non-registered account, but not otherwise. I’m not actively adding to my non-registered investments, so I don’t think this is for me either, although I’ve often wondered about how many stocks you actually have to hold in order to get “close enough” to the performance of the TSX 60 / S&P 500.

Sounds like an offer ripped from the pages of CIBC, BMO, or RBC. Dedicated advisors, tailored advice. Wealthsimple’s differentiator appears to be in the fee structure. From https://www.wealthsimple.com/en-ca/advice:

Our fees start at 0.75% and drop to 0.4% for clients who have $10M or more with us.

I am not a fan of percentage-of-net-worth-based wealth management. It implies that larger portfolios are more complex. Anyway, this might be the kind of offer future, less-capable-me might be interested in, but at the moment, no thanks.

“Coming Soon”

The other features announced on the event are not available yet. But here’s a view all the same:

Summit Portfolio: sounds like a robo-advisor that also includes private equity. Since I like my investments to be liquid, this is another development that doesn’t really interest me.

Retirement Accelerator: cheap loans to help you with RRSP contributions. Leveraged investing doesn’t fit my risk profile, and, oh, by the way, I’m already retired 🙂

Norbert’s Gambit: This is something I use all the time given that i have a large amount of USD holdings in my retirement portfolio. The best thing about the Wealthsimple webinar is that they actually trotted out Norbert6 himself to talk about it! This is one feature missing from the Wealthsimple portfolio that was a “must have” for me given my current holdings.

AI Trading Features, Advanced Options Strategies: Yawn.

Wealthsimple continues to be a broker I like to watch as they keep the new features rolling out. They are still not a serious contender to be my #1 broker until they support self-directed spousal RRIFs, something they inexplicably still lack.

Mostly because of the DPSP debacle and the fact I needed a new Macbook. ↩︎

On the webcast, it sounded more like they held “a representative sample” of these indices, which makes sense to me; you couldn’t hold ALL the members of the index AND do tax-loss harvesting at the same time. Their FAQ at https://www.wealthsimple.com/en-ca/portfolios/direct-indexing confirms this. ↩︎

VCN is an ETF that holds the same index, as far as I can tell. ↩︎

VFV is an ETF that holds the same index priced in CAD. IVV is the same index priced in USD. I presume the Wealthsimple product is traded in USD, but they don’t explicitly say. ↩︎