As I’ve been alluding, my relationship with QTrade is coming to an end. It would have ended back in March 2025 when I moved the majority of my holdings to Questrade, but having an active RRIF can make things a bit more complicated when it comes to changing your online broker.

Anyway, the plan all along was to move the last of my QTrade holdings — 4 RRIF accounts: 2 for me, 2 for my spouse — to Questrade around now, after most of the RRIF payments for 2025 have been taken care of1.

But then Wealthsimple came around and decided to throw free money on the table2. And they even helpfully extended the registration deadline — multiple times — to make it even easier. Now, I know I preach about simplifying your arrangements in retirement to make it easier on your heirs, but hear me out….

Because of a problem with my DPSP, (another cautionary tale for those who are considering retirement), I already had a RRIF with Wealthsimple (and a nice shiny MacBook Air) as a reward for my troubles. If I wanted to keep my MacBook, I had to keep my money with Wealthsimple3 until January 2026, so that RRIF wasn’t going anywhere…I reasoned I wasn’t really making things more complicated. I’m going from using three brokers to using two, so that’s clearly an improvement.

Moving accounts from another provider to Wealthsimple, like many things Wealthsimple does, is totally digital, and very, very easy to accomplish. All that was needed was the account number and a recent statement from my sending broker, and that was it. I think it took all of 10 minutes to get the ball rolling. No printers. No pictures. No pens. Just clicks and swipes.

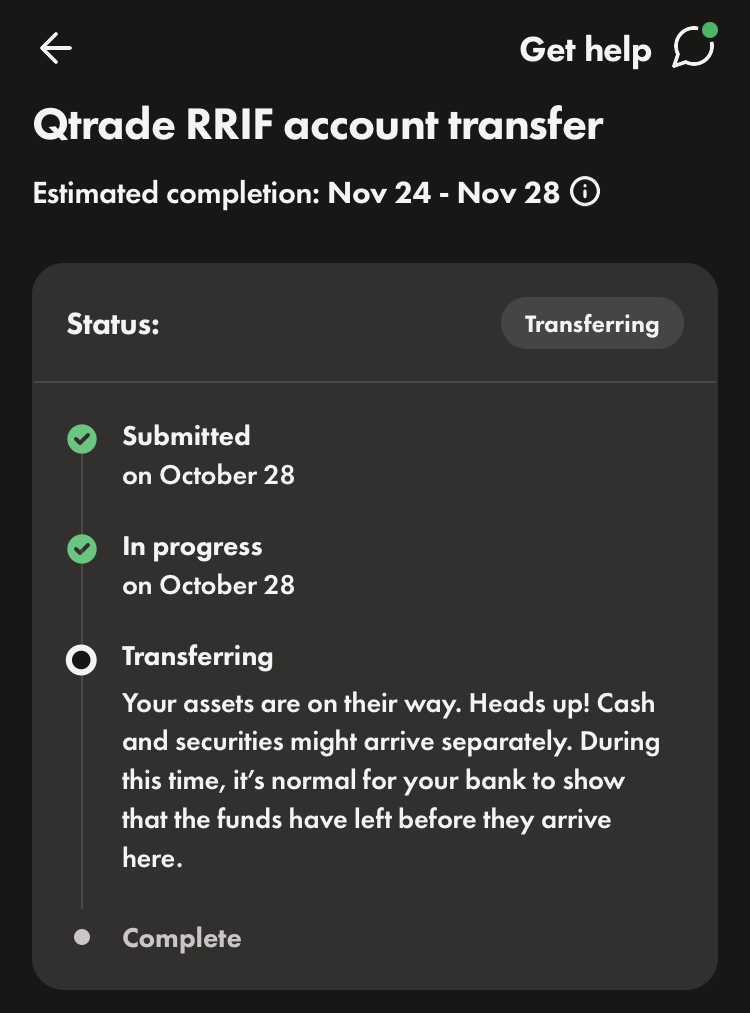

And even better is Wealthsimple’s super-clear status indicator, visible in the app or when using the web:

How clear is that? Of course, one could complain about how it could possibly take a month for things to move along (I know I did), but it’s stuff like this that makes me realize how far ahead of the competition Wealthsimple is when it comes to serving their clients.

What’s more, the transfer finished *way* ahead of schedule, being fully complete on November 8th, around 2 weeks after initiating the request. And, to make things even more pleasant, Wealthsimple has already reimbursed me the $150 plus GST that QTrade charged me for moving the account — no need for me to provide “proof” — the industry standard is well known to all, including, lately, the federal government.

I’ll provide an update once the free money starts rolling in. I have to update my workflows on how I get paid, since it’ll be a new world starting in January!

- I take RRIF payments monthly to make it more like a salary. And to avoid large stock sales all at once, since getting paid means selling assets. ↩︎

- I wonder if the gravy train in this space will end — read more about my thoughts on that here ↩︎

- The catch with free money (or free gifts) from brokers always involves keeping your money intact with them for some non-trivial amount of time. 12 months and 24 months are both pretty common. No big deal to me, I intend to stay retired a lot longer than that. ↩︎

Discover more from The Money Engineer

Subscribe to get the latest posts sent to your email.

[…] after the final, final deadline of Wealthsimple’s last free money offer, it appears that Wealthsimple is now offering spousal RRIFs as an account type for the DIY investor […]

LikeLike

[…] I moved my own RRIF account to Wealthsimple in late October to take advantage of (you guessed it) free money, which left 3 other accounts to move to Questrade before the end of the […]

LikeLike

[…] RRIF was moved to Wealthsimple in early November 2025 and this was an altogether painless experience, and I’ve been enjoying free money every month from Wealthsimple for my troubles. A good […]

LikeLike