This is a monthly look at what’s in my retirement portfolio. The original post is here.

Portfolio Construction

The retirement portfolio is spread across a bunch of accounts:

6 RRIF accounts

3 for me (Questrade, QTrade, Wealthsimple)

3 for my spouse (Questrade, QTrade)

2 TFSA accounts (Questrade)

4 non-registered accounts, (1 for me, 1 for my spouse, 2 joint, all at Questrade)

The view post-payday

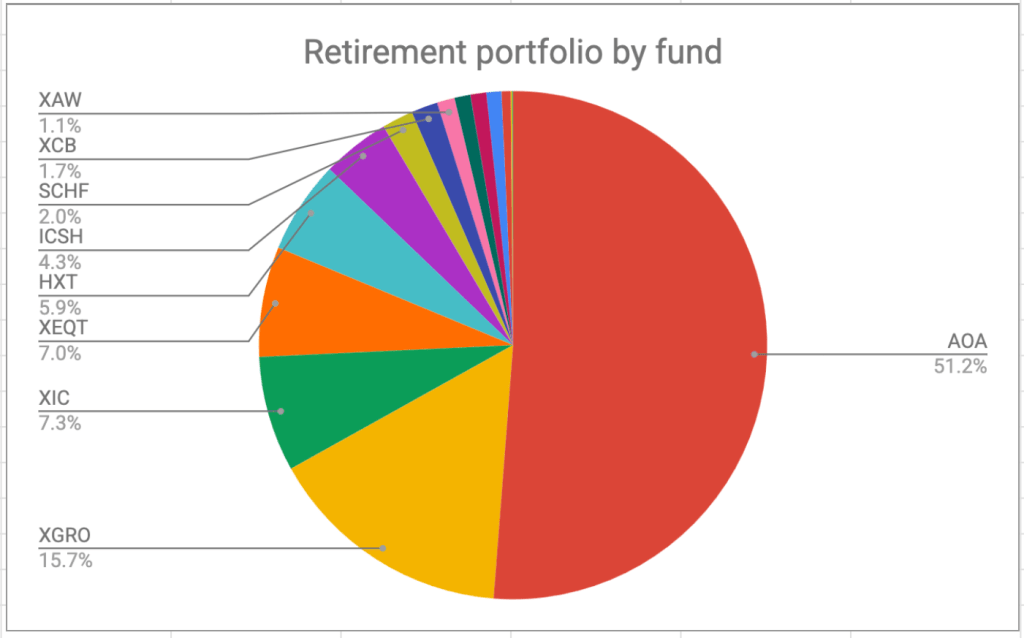

I pay myself monthly in retirement, so that’s a good trigger to update this post. On January 26, this is what it looks like:

The portfolio is dominated by my ETF all-stars, but if you’ve been following along, you’ll see a few changes.

As mentioned in a previous post, I did some shifting around and you now see XAW and XIC increasing their contribution to the portfolio at the expense of XGRO.

I also tidied up some extra funds that aren’t needed — VCN was replaced with XIC1, and I turfed some small holdings.

I sold more HXT than I needed to for my monthly paycheque, and when I discovered the mistake2, I just bought XIC instead.

And, I did my quarterly Norbert’s Gambit to shift some AOA to XGRO. And again, I came out ahead!

Plan for the next month

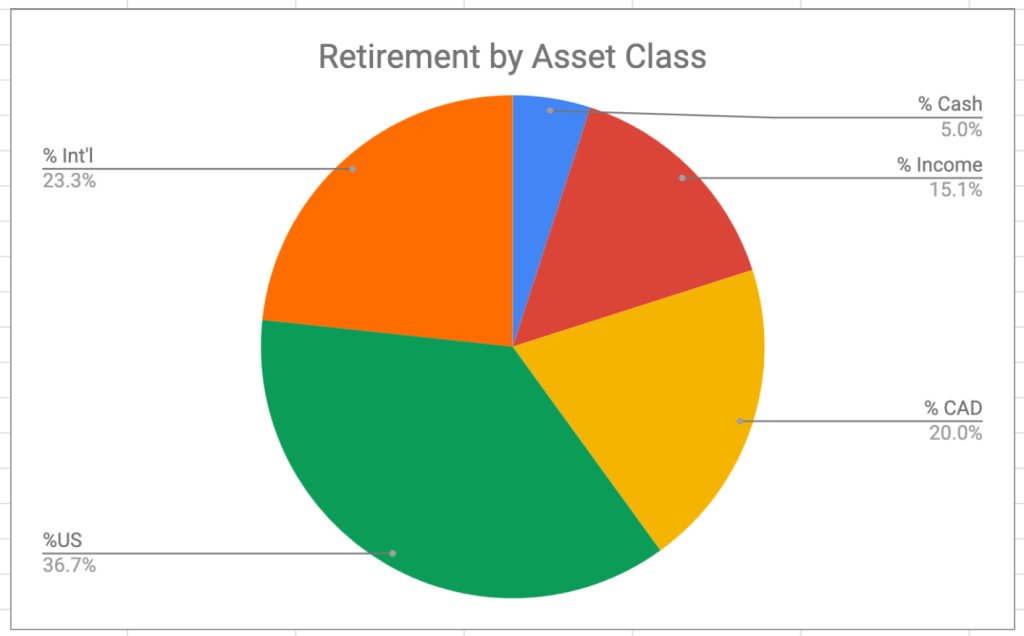

The asset-class split looks like this; you can read about my asset-allocation approach to investing over here.

It’s looking pretty close to the targets I have, which are unchanged:

5% cash or cash-like holdings like ICSH and ZMMK

15% bonds (most are buried in XGRO and AOA, some are in XCB)

20% Canadian equity (mostly based on ETFs that mirror the S&P/TSX)

36% US equity (dominated by ETFs that mirror the S&P 500)

24% International equity (mostly, but not exclusively, developed markets)

Overall

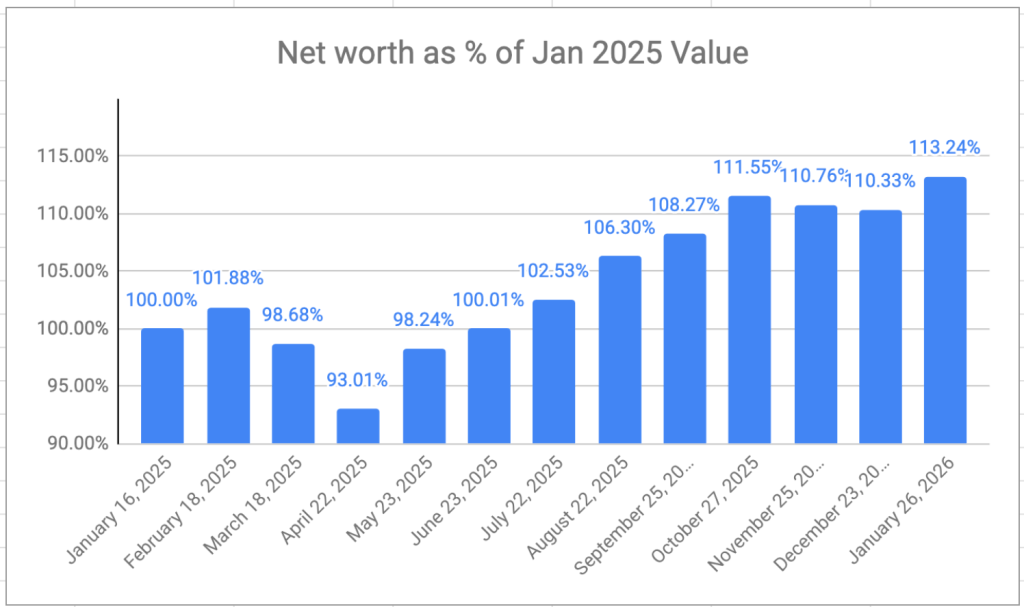

Net worth overall is up month over month, reversing a 2 month losing streak and hitting a new all-time-high:

I had to do some quick manual calculations because I had already updated my auto-calculating spreadsheet to reflect fewer RRIF accounts. My RRIF transfers are 2 months in progress and counting. I guess trying to move a RRIF near the end of the year was a bad idea. ↩︎

My retirement portfolio is spread across multiple brokers and multiple accounts. And although I treat the portfolio as a unified entity when it comes to asset allocation (the concept is discussed here), different accounts have different allocations. The reasons are varied, but I would rank inertia as one of the big contributors — sticking with what’s there seems like a lot less effort than the other options.

What I think in important to point out is that the portfolio is still dealing with inflows and outflows every single month:

I pay myself RRIF minimum from my RRIF accounts, and this usually means selling some shares of XGRO

If RRIF minimum isn’t sufficient for my expenses (and it hasn’t been), then I have to liquidate shares from my non-registered account.

I contribute to our TFSAs every month

Questrade gives me free money every month as a reward for shifting assets their way (see how I did it here). This money shows up in my non-registered accounts1.

Dividends show up every month2; every quarter there is an even bigger distribution

And quarterly I convert some of my AOA holdings to XGRO within my RRIF using Norbert’s Gambit3. When I do this, it reduces my US and international equity holdings and replaces it with Canadian equity4.

So given all these ins and outs, there are always opportunities to tweak the asset allocations so that they remain close to my targets.

But this study did make me realize that the small allocation I had of bonds in my TFSA was wrong-headed. Since in my planning the TFSA is the LAST place I’ll head to fund my retirement, it follows that it should have the longest-timeline investments. So, for me, that means 100% equity is the correct allocation for the TFSA accounts. So what did I do?

I sold the bonds in my TFSA (XSH was the ETF), and put them in my RRIF (choosing instead to use XCB, a longer-duration corporate bond fund)

Of course, since you can’t add money to a RRIF, something had to be sold there. XGRO was plentiful, so that’s how I funded the bond purchase. From an asset allocation perspective, selling XGRO meant that I reduced my Canadian, International and US Equity exposure at the same time.

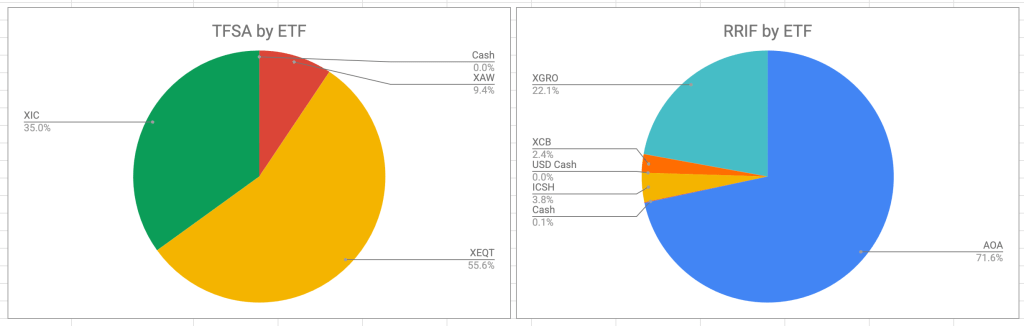

To compensate, the cash I generated in my TFSA by selling XSH was used to buy a combination of XIC (Canadian Equity) and XAW (US and International equity combined). XIC was already in the TFSA6. XAW is new but gives back the US Equity and International Equity I lost by selling XGRO7.

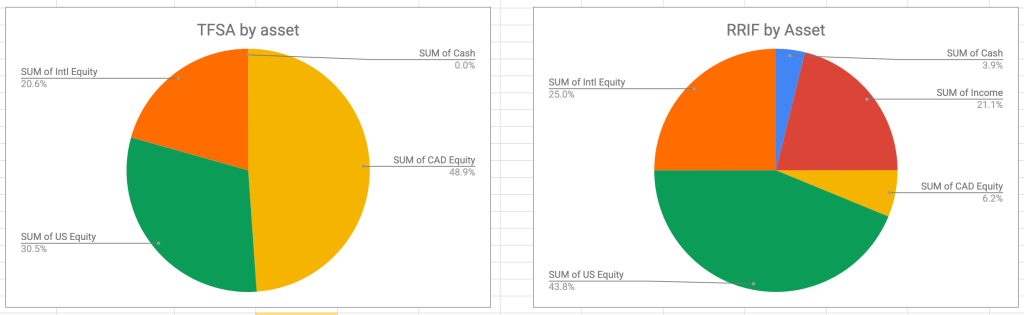

This is how the two accounts break down now, both from an ETF and an asset-allocation perspective. (In the asset allocation charts “Income” is the nomenclature I use for “bonds” and “Cash” means actual money as well as ultra-short-term bond funds like ICSH and ZMMK).

The result is my TFSA is now 100% equity, and the lower-growth cash-generating bonds are now all in my RRIF accounts. More efficient all around!

Leaving the free money as part of the retirement portfolio was a conscious decision. I could have just as easily decided to withdraw the money every month. ↩︎

Both ZMMK and ICSH pay monthly. They are both featured in my ETF all-stars. ↩︎

AOA is 50% US equity, 28% International equity. XGRO is 36% US Equity, 24% International Equity. ↩︎

It’s not a straightforward topic. In the end, the foreign withholding tax isn’t huge but as a cheapskate, it’s noticeable and can be higher than MERs of the ETFs you hold. ↩︎

XIC helps tilt the overall Canadian equity allocations in the right direction. AOA tilts it in the wrong direction. ↩︎

The current numbers don’t allow me to use an XEQT/XIC combination. Over time, this will change. ↩︎

One of the confusing questions I got from my international colleagues when I announced my retirement was “what’s the retirement age in Canada”? And, after thinking about it, said, “There isn’t one that I know of”, which is, strictly speaking, correct.

However, for many Canadians (and, I suppose, for many people around the world), “retirement age” equates to “the age where I can collect my pension”. For me, the equivalent statement was “the time when my retirement savings were sufficient1” (you can read about the steps I took here). I don’t have a private pension through my employer, so CPP, OAS and my own savings are all I have to sustain my needs throughout retirement.

CPP (Canadian Pension Plan) and (possibly2) OAS (Old Age Supplement) are two sources of income that will eventually make up part of my retirement income, but not for a while. For the time being, my retirement income comes from a mix of non-registered asset sales (about 2/3 of my 2025 household income) and RRIF payments (about 1/3 of my 2025 household income)3. My advisor suggested waiting as long as possible to collect on CPP/OAS, which is age 70 for both.

But maybe, if you haven’t retired yet, you haven’t really thought too much about these things4? Here’s a quick primer.

What’s CPP and what’s it worth to me?

CPP applies to anybody who has contributed to the plan; how much you contribute annually is captured on your T4 slips. You can see your lifetime contributions5 by logging into your My Service Canada Account. It is the history of these contributions6 that ultimately determine what your annual pension will be in the year you first start taking it.

The first year you are eligible to receive CPP is the year you turn 607; every month you wait after turning 60 increases your monthly payment. The absolute maximum CPP you could collect would be waiting until you turn 708. The Feds lay it all out here.

The absolute maximum monthly CPP you could possibly get as a 65 year old is $1507.65 in January 2026 per the Feds9. Since I retired early, and 18 year-old me worked a part-time minimum wage job, my CPP will be less than that. (The CPP calculation takes your best 32 years of earnings into account).

What’s OAS and what is it worth to me?

OAS (“Old Age Security”) applies to anybody who has lived in the country long enough10. OAS can start at age 65, and be delayed until as late as age 70. Like CPP, OAS rewards those who start payments later than age 6511. You get an OAS supplement of 10% when you hit 75.

The absolute maximum monthly OAS payment in the first quarter of 2026 is $742.31 if you’re under 75 and $816.5412 if you’re over per the Feds. (These amounts are adjusted every quarter in accordance with inflation rates.)

The wrinkle with OAS is that it’s income-tested. If you make too much money, you’re going to have to pay some of it back. If you really make too much money, you’ll have to give it all back. This is commonly known as “OAS Clawback”13.

The magic of CPP and OAS

CPP and OAS payments are both indexed to inflation, for as long as you collect it. This is key for me personally — none of my other income sources are inflation-proof, so the more I can get that is inflation-protected, the better. That’s part of the reason I’m planning on delaying collecting CPP and OAS until I’m 70 — that way, I can maximize the inflation-protected income. The other reason I’m delaying these payments is to try to avoid OAS clawback. The earlier I take RRIF money out, the lower my RRIF income will be later in retirement, when I have to start adding CPP to my income. I have no idea if I will avoid the clawback because it depends on the performance of specific elements of my portfolio. But try I will.

Estimating CPP and OAS for VPW

My decumulation strategy is based on VPW (Variable Percentage Withdrawal). I’ve talked about it previously over here and here. VPW requires, as an input, the value of a future pension. So how do I go about estimating that? Any reasonable estimate might want to ignore what the feds put on the periodic CPP summaries they send out because those estimates are assuming you’re retiring at 65, and working at a similar salary level (of course, if that’s your plan, then it’s perfectly fine — but it wasn’t mine :-))

All good estimates start from the lifetime contributions table you can find at My Service Canada. From there I’ve given a few tools a spin:

This tool has a lot of neat features, but be careful. The model bakes in both inflation estimates and wage inflation estimates that are changeable, but not immediately obvious.

This is one I recommended previously in Tools I Use, but the upload feature has been broken for a while now. It still works by entering it manually, but I now prefer the tool below….

The Finiki tool is now my favourite because it’s available as a worksheet (Google Sheets, Excel and Libre Office all supported), and all you need to do is enter in your pension contributions. The current version (2.3) hasn’t been updated with the latest YMPE values, but it’s a trivial exercise to update them.

“sufficient” means different things for different people. You have to have a budget, and you have to have an idea what sort of estate, if any, you’re intending to leave behind. ↩︎

I figure my odds are 50/50 that my combined CPP+RRIF income when I hit 70 will render me ineligible for OAS. ↩︎

I am not planning on actually working for a living anymore; there are all kinds of rules concerning the interplay of CPP and employment income, but I’m not talking about them here because that scenario doesn’t apply to me. ↩︎

Or, if you were a cynic like me, figured that it wouldn’t exist by the time I got to an age where I’d be collecting it. Seems like the pension plan is currently in pretty good shape. ↩︎

You would have to be at maximum pensionable earnings for 39 years between the ages of 18 and 65 to get this amount. (47 years less the 8 worst years of earnings). ↩︎

Which, if you’ve been paying attention, is 10% more than the benefit for someone under age 75. ↩︎

OAS is progressively reduced if you make more than $95k in 2026. You get no OAS at all if you make more than ~$155k at ages 65-74, $160.5k for ages 75+. These numbers are modified 4 times a year based on inflation. ↩︎

My retirement fund is divided amongst a bunch of different accounts: RRIFs, TFSAs, non-registered. And although I present them as a monolith in my monthly updates (latest one here), I don’t treat them the same way and they have rather different things inside them.

I don’t claim to have a fully optimized portfolio; a thoughtful reader was asking me questions about tax implications of my current holdings, and I admittedly haven’t given a ton of thought to that. But I will in a future post 🙂 .

So, in other words, you’re getting my current thinking for what I hold where. It may not be ideal. But at least you see why things are the way they are.

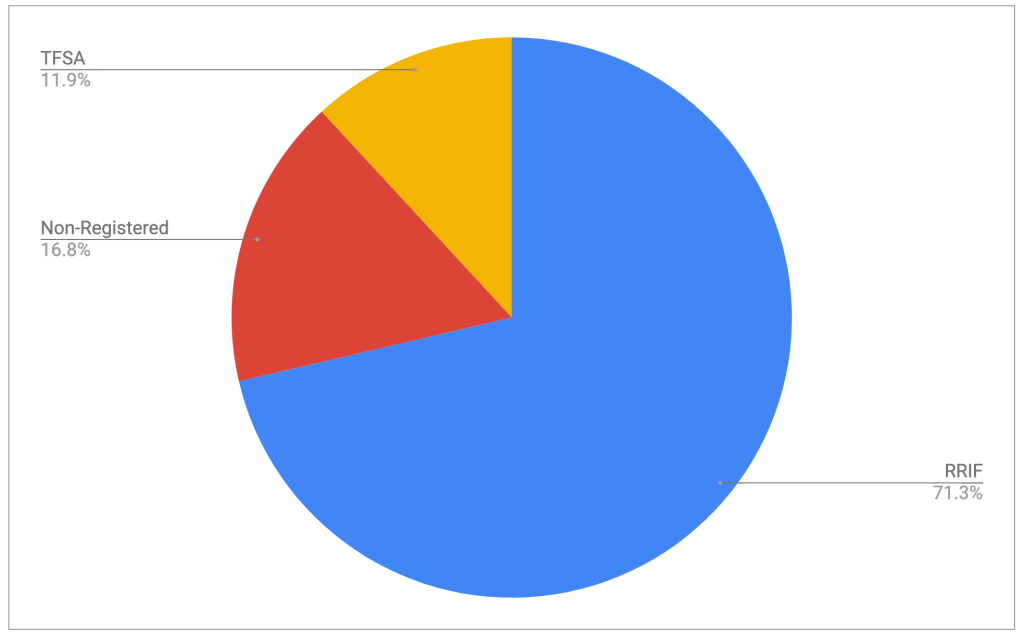

Below you can see how my retirement funds are divided amongst my various investment vehicles. This one is accurate as of January 8, 2026, and is greatly facilitated by tracking my stuff in Google Sheets. There’s a basic template of what I use over here1.

Retirement portfolio, divided by account type, January 2026

So that’s where it’s at. How do I treat the three main segments of the pie?

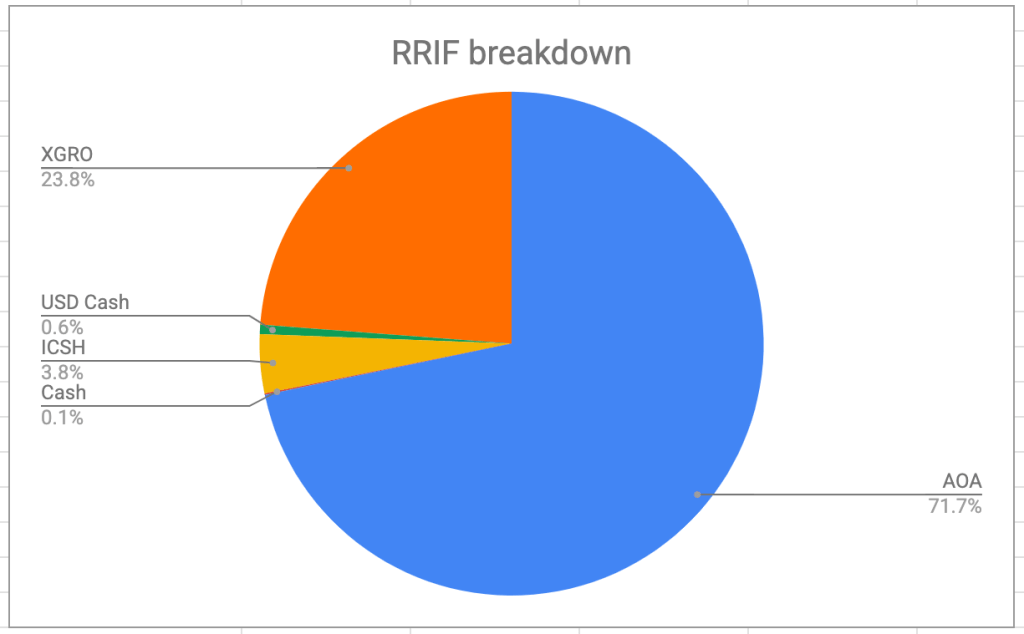

RRIF

So the RRIF is clearly the largest piece of the retirement pie and will be around for some time, possibly for the rest of my life. At this point in time, I’m only taking RRIF minimum payments which are recalculated every year and are based on my age and the value of my RRIF on December 31 of the previous year.

I am taking RRIF minimum primarily because I want to avoid the hassle of spousal RRSP/RRIF attribution that I talk about here. RRIF minimum is quite a bit less than the expected return of this account given the holdings therein, mostly AOA and XGRO:

I periodically (once a quarter) shift funds from AOA to XGRO using Norbert’s Gambit2. How much? Well, at the beginning of the year, I see how much of my RRIF is in USD. I then multiply that by my RRIF age factor3, divide by four, and presto, I have a quarterly amount I should move.

All of my many RRIF accounts4 have XGRO, and on the day I make my payday calculations, I have a spreadsheet that calculates how many shares of XGRO I need to sell in each account given the current price of XGRO and the amount of CAD happens to be kicking around in a given account. In very rare circumstances, I might (as well/instead) sell AOA if I had a need for US cash5.

The small contribution of ICSH here is because I have a 5% “cash” asset allocation in my portfolio, and I needed someplace to keep this monthly income. RRIF seems as good a place as any, especially since all those monthly dividends are completely tax-free as a result.

In the coming years, the RRIF will take on more and more of my monthly spending needs. Once the attribution time period has lapsed, I’ll probably take more than RRIF minimum from here in an effort to reduce taxes for older me — once I start collecting CPP/OAS as well as RRIF payments, I could find myself in a taxation world of hurt. Making my RRIF smaller will help, but there is no free lunch. You either pay taxes while you’re alive, or your estate will pay them when you’re not.

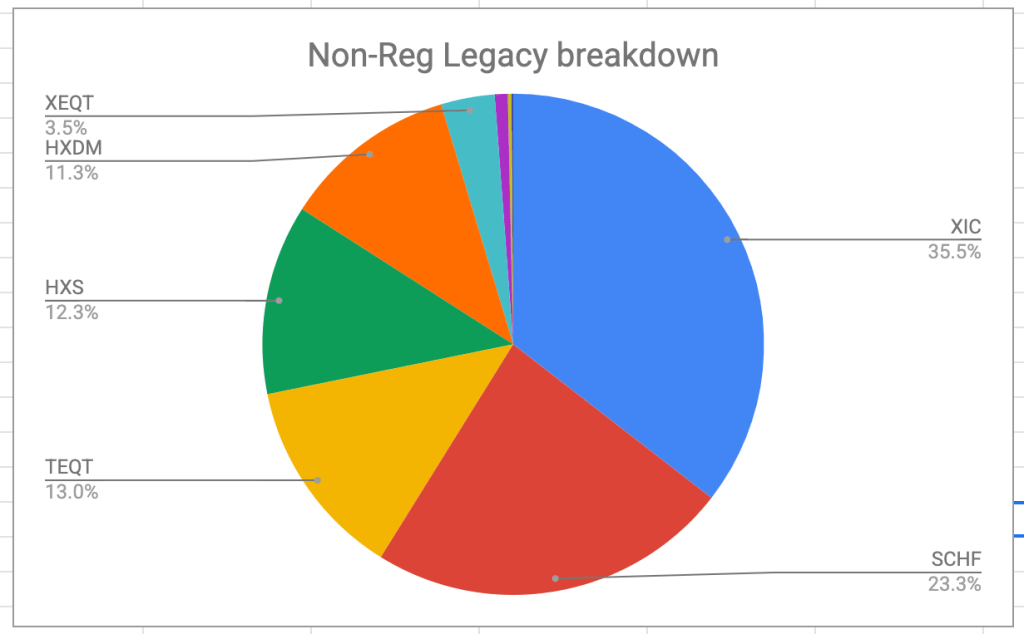

Non-Registered Accounts

I really have two kinds of non-registered accounts in my retirement calculations, and they have very distinct usages. Let’s see the difference:

The “legacy” non-registered accounts are long-standing accounts that have grown over the years of accumulation. They are held in my name and my spouse’s name and taxed accordingly. These accounts, specifically the one in my name, account for probably 2/3 of my current income. Every time I withdraw from these accounts, I have to account for capital gains, which is fine, since the taxation treatment of capital gains is generous. You’ll also notice that this account is 100% equity. And as previously noted, the dividends thrown off these investments is not particularly noteworthy (not zero, but nothing a dividend-focused investor would get excited about). That’s why you see funds like HXDM and HXS here, to explicitly avoid dividends. This portion of my non-registered funds is targeted to eventually go to zero in the next few years, probably before I start collecting CPP. That’s a tax avoidance strategy, no idea if it will work out in my favour.

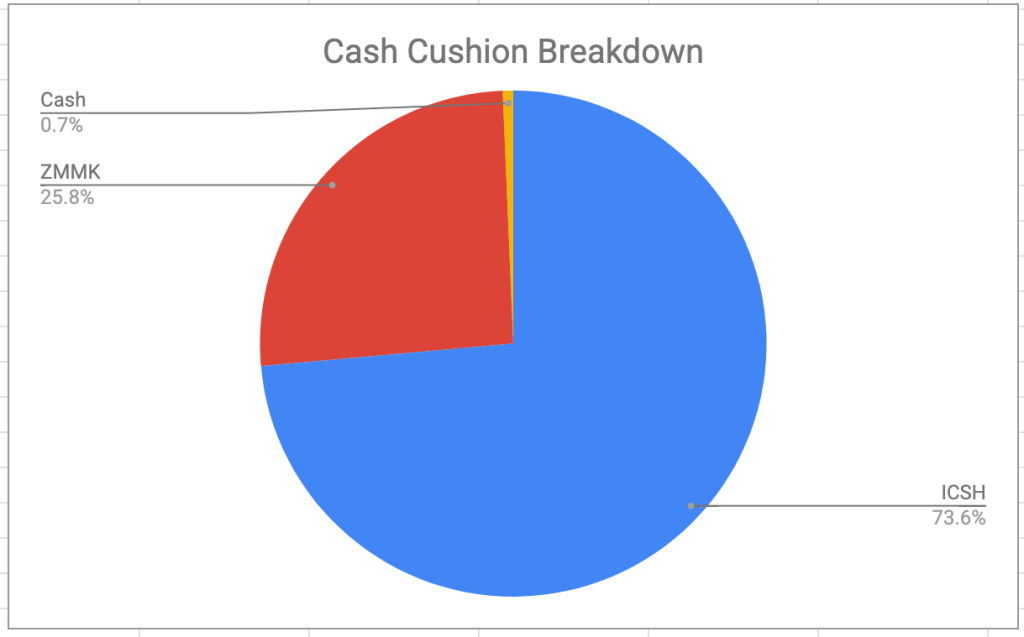

The “cash cushion” non-registered holdings are 100% in ultra-short term bond funds, which to my way of thinking, is equivalent to cash. This account exists because I use VPW as a decumulation strategy, and the cash cushion helps smooth out my monthly salary. Sometimes I add to the cash cushion (directly from my other non-registered account) and sometimes I pay myself from the cash cushion. You can read all about how it works at The Mechanics of Getting Paid in Retirement. Here I keep a bit of uninvested cash floating around in an effort to reduce the number of buys/sells I have to do here. The capital gains are quite minimal in these funds since both ICSH and ZMMK stay close to $50/share6 but it’s possible to make minor gains/losses7 depending on the exchange rate and day of month I make the purchase/sale.

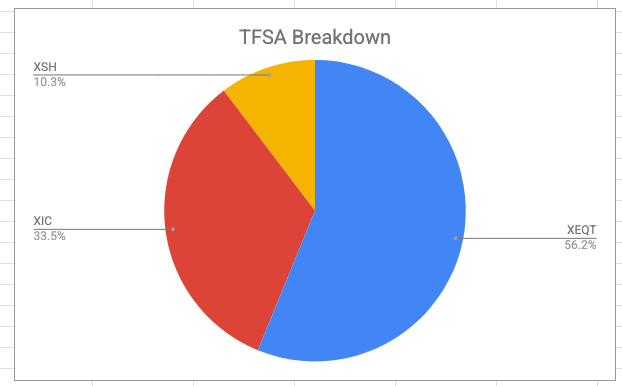

TFSA

The TFSA, per the plan prepared for me by my fee-based advisor, (part of the steps I took to figure out that I had enough to retire) is the last account to decumulate. I continue to contribute to my TFSA monthly, like I have ever since TFSAs were a thing. That would be an “expense” I could cut if needed, I suppose. It tilts heavily towards equities8:

Besides XEQT, you currently see XSH, a bond fund9. This exists in order to keep my target asset allocations in line, and because I don’t really want the monthly distributions landing in a taxable account. Perhaps that holding would be better in my RRIF? There’s also XIC here, which is a Canadian equity fund, necessary to offset the heavy US equity contribution made by AOA.

Over the holidays I’ve started on a new template that makes heavy use of pivot tables, which I do like quite a bit. ↩︎

Hopefully in a week or two it will be down to five. ↩︎

I do have a USD bank account (via CIBC) and a US credit card (ditto) to avoid FX charges, but my shiny new Rogers Red card also provides sufficient cashback on USD transactions to wipe out the extortionate FX rates charged by credit card companies. ↩︎

Reverts to around $50 on its ex-dividend date, late in the calendar month. Except January, where ICSH doesn’t distribute at all, instead distributing twice in December. ↩︎

Longer timeframe = higher risk acceptable = more equities ↩︎

Here is a bit of problem. XSH is a short term bond fund; by rights, this should be a long term bond fund since the timeline of the investment is longer. Sigh. I picked this one because (a) it had corporate bonds and (b) it had a very low MER. ↩︎

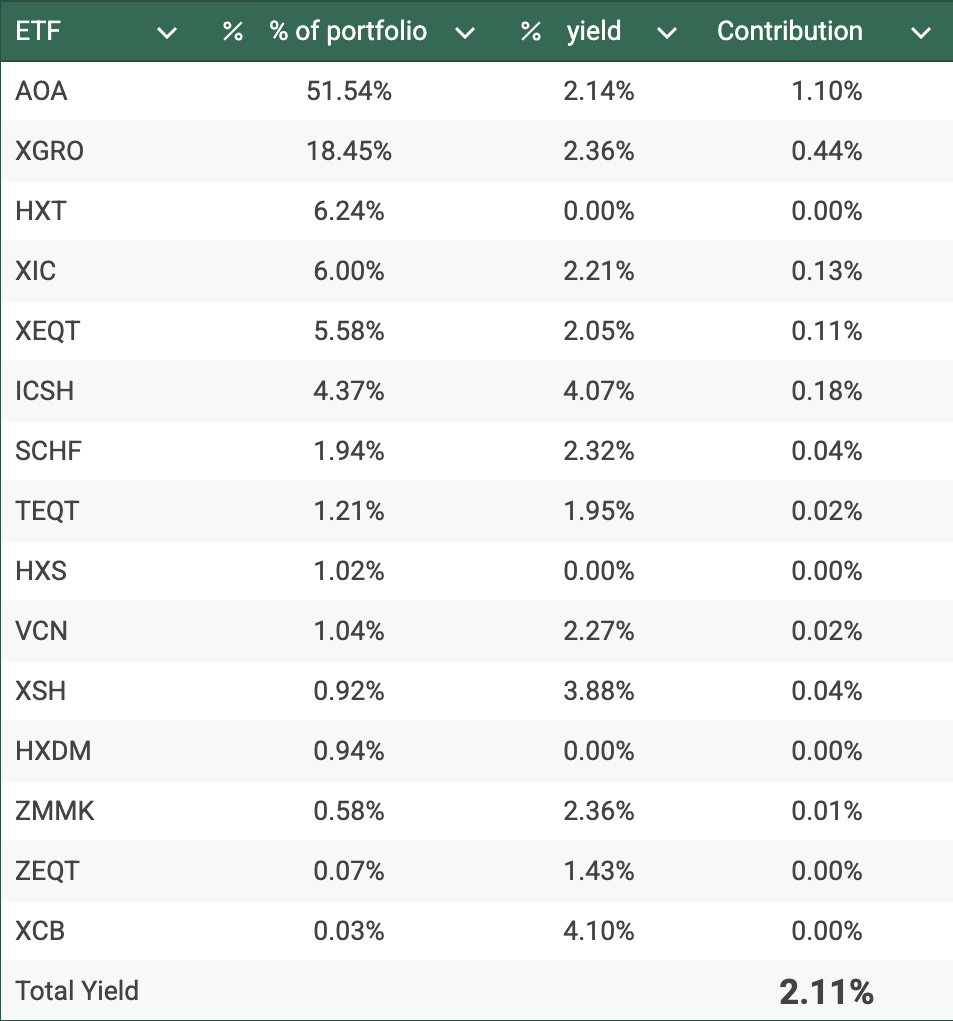

I had an email from a reader this week (via comments@moneyengineer.ca, I read all the email I get) who was curious about the yield of my retirement portfolio. It occurred to me I haven’t really talked much about this topic, so thanks for the inspiration 🙂

A very common approach for retirement investing is to build a portfolio based on high-quality dividend-paying companies. The best example I can think of is the long-standing “Yield Hog” portfolio written about by the Globe and Mail’s John Heinzl. He updated readers at the end of 2025.

So, using the ETF fact sheets1 and my current holdings, I give you the overall yield2 of my retirement portfolio:

So the overall yield is just a little north of 2%. For a divided investor, this would seem alarmingly tiny.

If building an income stream from this portfolio was your objective, you’d either have to have a lot of capital, or very modest income needs, as this portfolio is only generating about $20k in dividends for every $1M invested.

For me, I’m perfectly happy to dip into capital (i.e. sell ETF units) to fund my retirement. The overall growth of the portfolio is my only consideration, and whether that is in the form of dividends (which, in my portfolio, are always reinvested3) or capital appreciation (i.e. the price of the ETF increases) is irrelevant to me.

Is it possible to build a dividend-focused portfolio just based on ETFs? Sure. But here I do offer a word of caution. The ETF providers out there have learned how to structure products with spectacular-looking yields that either use leverage (and are hence inherently more risky) or boost their yields by using RoC and giving you back some of your own money. So looking at yield numbers alone without understanding what’s inside the ETF is not a good idea. I took a look at one reasonable product (ZGRO.T) in a previous article.

The Globe has been my go-to trusted source for such things for a long time; they have annually updated ETF lists in various categories, including dividend ETFs. One that jumps out for me on this list due to its very low cost to own4 (which is something I’m a bit fanatical about, admittedly) is XDIV.

XDIV’s current yield is 3.93%, and holds large Canadian companies like TD, Royal Bank, Manulife, Sun Life, Suncor Energy, Power Corp…In total it holds only 21 companies, with never more than 10% invested in any one company5.

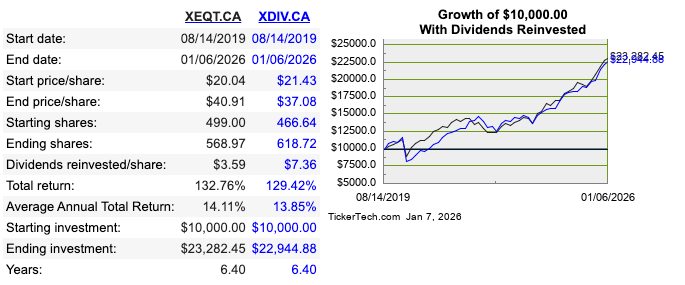

Just for fun, I did a head-to-head comparison of XDIV versus XEQT using this calculator that is featured in Tools I Use. I chose XEQT even though it’s a smaller portion of my portfolio than XGRO, but is a better stand-in since XGRO holds bonds.

So here it’s practically a tie. If you reinvested all the dividends for both ETFs, XEQT would have generated about $300 more on an initial investment of $10000 in August 2019.

But is that really a good comparison? XEQT and XDIV are pretty different:

XEQT adds extra fees because it rebalances automatically between its different geographical holdings

XEQT invests globally; XDIV is limited to Canada only.

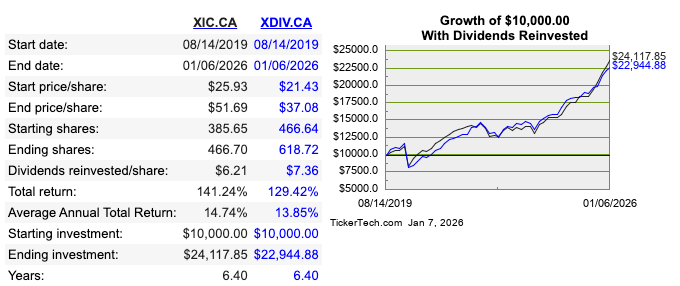

What if I instead chose to compare the Canadian portion of XEQT to XDIV? (I broke down what’s inside these all-in-ones in a previous article: Under the hood of XEQT et al). XEQT’s Canadian portion is XIC, an ETF that tracks the entire TSX (219 stocks), so let’s run the numbers again over the same time period:

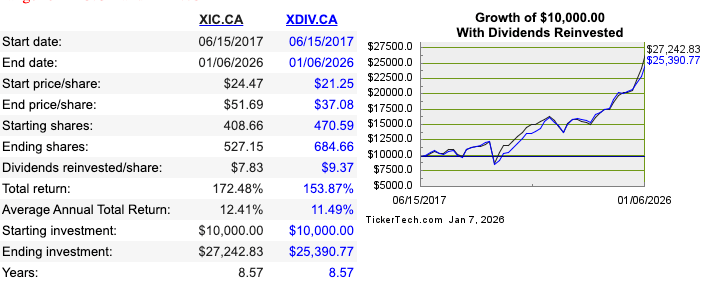

Here the gap is more noticeable: XIC outperforms by about $1200 in the same time period, assuming all dividends are reinvested. Now, of course, you can see that sometimes XDIV was ahead during this period. I cranked up the timeframe to as far back as I could to see what the results were:

Adding two more years of retrospective increased the gap by another $800, which is about a 1% per year return advantage to XIC.

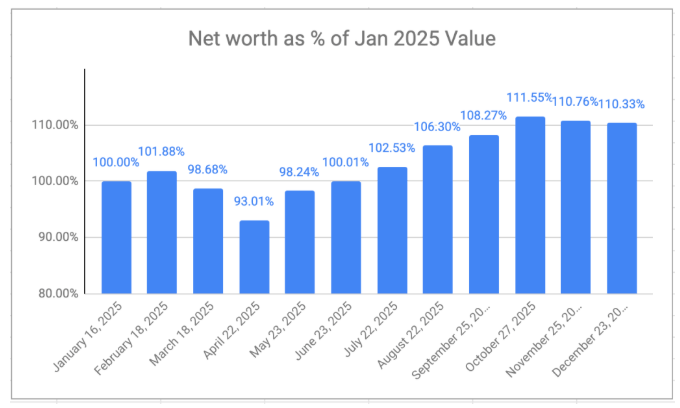

Now of course, you could find counter examples I suppose. But if capital preservation isn’t a concern6, then these results tell me that dividends needn’t be a concern in retirement. Even with my anemic yield stats, my net worth increased in 2025 even accounting for getting paid every month (chart from my latest What’s in My Retirement Portfolio):

Every month, I sell XGRO shares to fund my RRIF payments. Every month, I sell some non-registered assets to cover the rest of my salary. The TFSA gets a monthly contribution. Selling shares isn’t bad — as long as those that remain keep growing, I can keep spending7!

TEQT isn’t publishing a yield, so I made an attempt to calculate it based on the Dec 31 distribution. This seems a bit lazy on TD’s part: I get that it’s a new ETF, and 12 months of data isn’t available yet, so you can’t show a trailing yield, but you CAN show the forward looking yield based on the most recent distribution. Banks. Sigh. ↩︎

A weighted average. You may wonder about HXS/HXDM — these are “corporate class” ETFs that by design do not make distributions and instead use accounting tricks to bury that growth inside the ETF price. It’s something I use in my non-registered accounts. ↩︎

Either automatically via DRIP or through my own purchases; it’s a bit of a mix at the moment. ↩︎

A MER of 0.11%, a bargain for this sort of ETF. ↩︎

Otherwise, its tracking index (MSCI Canada High Dividend Yield 10% Security Capped Index) has a TERRIBLE name. ↩︎

For me, it isn’t. I’m not looking to leave a large estate. Die with zero! ↩︎

And if they shrink, so does my spending. That’s the VPW way. ↩︎